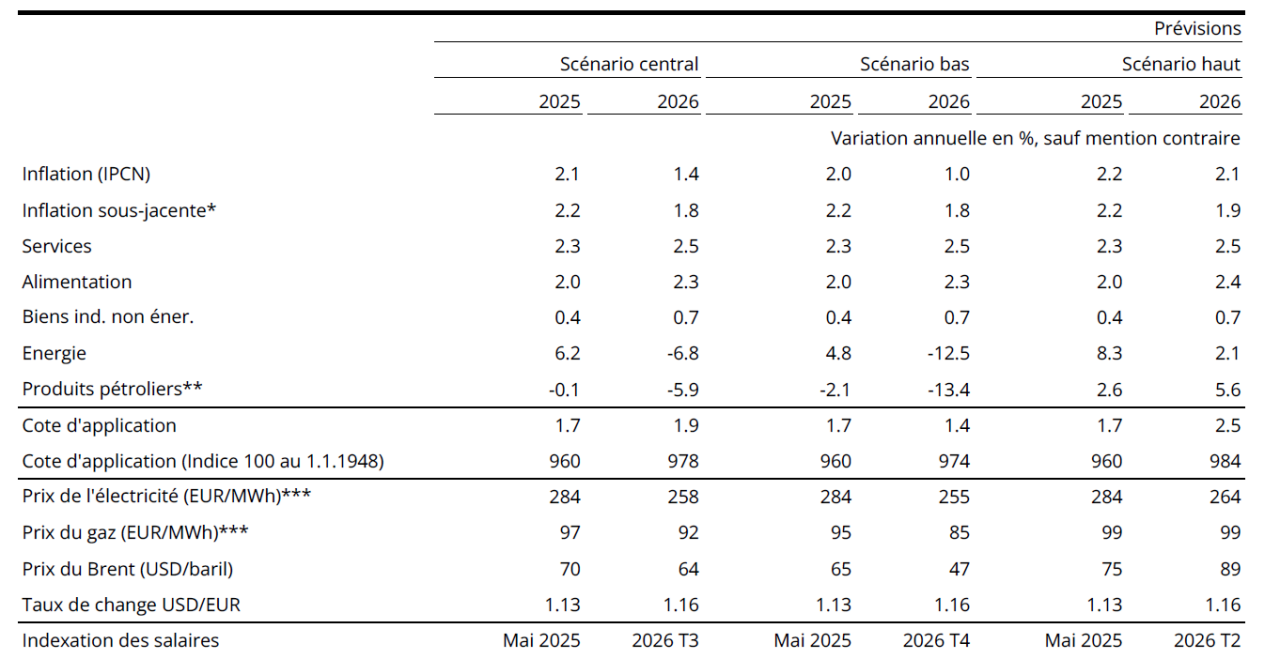

Inflation forecast : 2.1% for 2025 and 1.4% for 2026

Consumer price growth in Luxembourg was relatively strong in the second quarter of 2025, automatically raising the inflation forecast for the current year. However, measures to stabilise electricity prices are expected to lower the forecast for 2026. STATEC forecasts inflation of 2.1% for this year and 1.4% for 2026, provided that energy prices do indeed fall and the euro remains strong. The next index adjustment is scheduled for the third quarter of 2026.

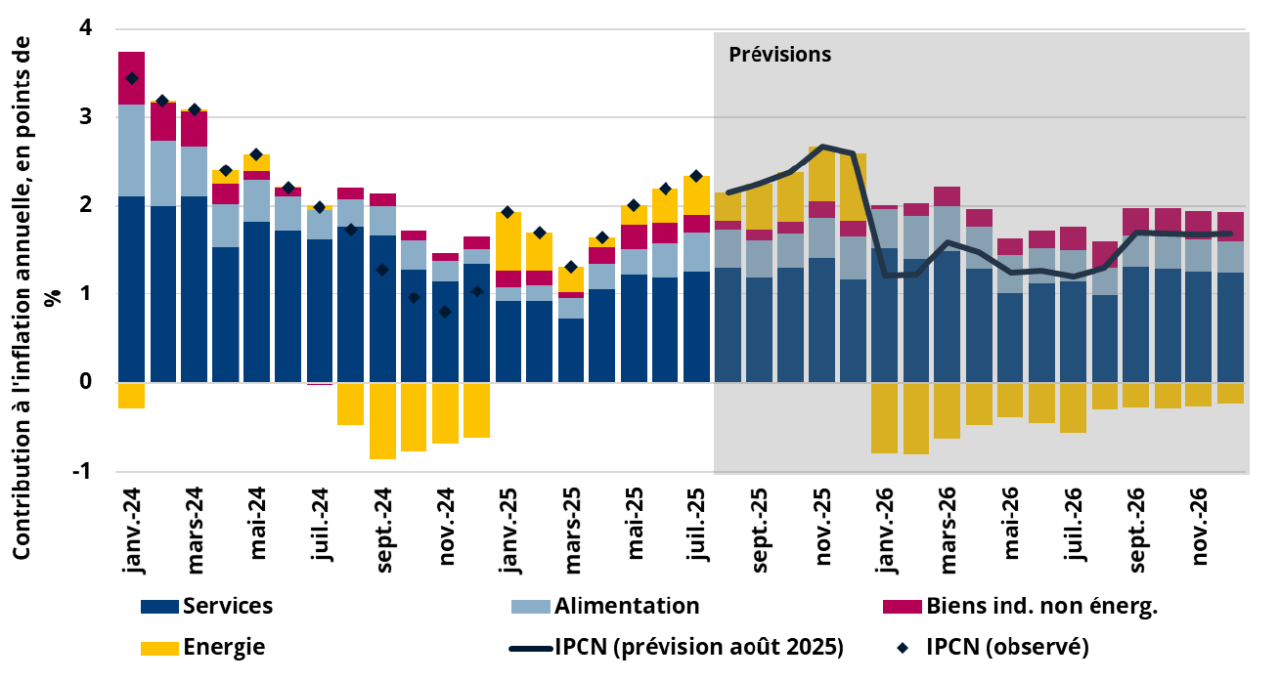

Annual inflation rate and contributions

Source : STATEC (forecast from 06/08/2025)

Annual inflation rose to 2.3% in July, its highest level in over a year. Services inflation remained at its June level (+2.4% year-on-year in July) after being sustained by wage indexation in May (+2.6%), while food inflation strengthened (+2.5% in July compared with +2.2% in June 2025) amid growing pressure on producer prices[1]. Annual core inflation[2] stood at +2.4% in July (compared with +2% a year earlier).

Under the influence of geopolitical tensions in the Middle East, Brent crude oil prices reversed their downward trend in the spring. Oil prices rose in June (+9% over one month[3]), with the increase being passed on to the prices of most petroleum products in Luxembourg in July (+2.1% over one month, after +1.4% in June). This increased pressure on energy prices (+5.9% year-on-year in July, compared with +0.8% a year earlier).

Across the euro area, inflation remained stable at 2.0% according to a preliminary estimate for July (compared with 2.6% a year earlier), confirming a slowdown around the ECB's target. This apparent stability is mainly due to energy prices, which have been falling since March (-2.5% year-on-year in July), compensating for increases in other expenditure items. Food prices remain buoyant, up 3.3% year-on-year (compared with 3.1% in June), services prices posted annual inflation of 3.1% in July (after 3.3% in June), and industrial goods prices excluding energy continued to rise modestly, up 0.8% year-on-year (compared with 0.5% in June).

EU-US customs duty agreement: less uncertainty about inflation in the eurozone?

The main international institutions anticipate average inflation in the eurozone of close to 2% in 2025 and 2026. For 2025, forecasts range from 2.0% (Oxford Economics) to 2.2% (OECD). For 2026, inflation is forecast to range from 1.7% (Oxford Economics) to 2.0% (OECD), with forecasts revised downwards compared to the second quarter of 2025, largely due to the strengthening of the euro.

The July 2025 projections by Oxford Economics, which feed into STATEC's current forecast, revise the assumption for the price of Brent crude oil to USD 70 per barrel in 2025 and USD 64 per barrel in 2026 (compared with USD 67 per barrel previously), reflecting the deterioration in the global economic outlook. Furthermore, reflecting the Trump administration's economic policy, Oxford Economics forecasts a sharp depreciation of the USD exchange rate against the EUR to USD 1.13/EUR in 2025 and USD 1.16/EUR in 2026 (compared with USD 1.09/EUR and USD 1.10/EUR previously). This depreciation would further contribute to the decline in oil prices in Europe in 2026.

The trade agreement between the EU and the United States, announced on 27 July, should set a single, maximum tariff rate of 15% for US customs duties on goods originating in the European Union, half the 30% initially announced by Washington. The absence of similar retaliatory measures by the EU – the proposed surcharges on €93 billion worth of US imports having been abandoned – dispels most of the uncertainty surrounding the additional inflation that the tariff escalation could have triggered.

Inflation is expected to remain below the 2% target in Luxembourg in 2026

In Luxembourg, the recent automatic wage indexation has contributed to higher service prices. Inflation is expected to rise further in the coming months, reflecting the strengthening of positive base effects on energy and, to a lesser extent, food at the end of the year. Higher-than-expected inflation in the second quarter of 2025 and a less pronounced decline in oil prices have led STATEC to revise its inflation forecast for this year to 2.1% (from 1.9% previously).

For 2026, the expected decline in oil prices and the recently announced measures[4] on electricity prices (corresponding to a 9% decline in 2026 compared to 2025) should bring energy inflation down to -6.8% in 2026 (compared to +4.2% previously[5]), which would result in inflation of 1.4% in 2026[6]. Inflation in services is expected to be 2.3% in 2025 and 2.5% in 2026, while food inflation is expected to be 2.0% in 2025 before rising to 2.3% in 2026. According to these forecasts (which constitute STATEC's central scenario), the next wage indexation is still scheduled for the third quarter of 2026.

Forecasts based on alternative energy price assumptions

Source: STATEC (forecasts as of 06/05/2025)

* In Luxembourg, core inflation includes the price of electricity.

** These forecasts include a CO2 tax increase of EUR 5/tCO2e in 2026.

*** Average prices including VAT for a residential customer in Luxembourg with an annual consumption of 2,426 m3 of gas and 3,901 kWh of electricity. These prices are calculated assuming i) for gas: network usage tariffs increasing in 2026 at the same rate as in 2025, ii) based on assumptions by the Ministry of Economy, for electricity: from 2026, a return of the contribution to the compensation mechanism to EUR 0/kWh and a 35% reduction in network usage tariffs in 2026 compared to 2025.

Two alternative scenarios have been developed based on historical deviations in the electricity, gas and Brent oil markets (the latter affecting fuel and heating oil prices). Taking into account the measures in place (and in particular an identical price in the different scenarios for electricity in 2025), the high and low scenarios for electricity only diverge for the year 2026. The high scenario assumes that in 2026, gas prices will stabilise, Brent price will rise by 18% and electricity prices will fall by 7%. The low scenario anticipates a more pronounced decline in the price of electricity (-10%), gas (-11%) and Brent (-27%) in 2026. In the high scenario, the next wage indexation would already be paid in the second quarter of 2026. The low scenario anticipates indexation only in the fourth quarter of 2026.

[1] Higher agricultural raw material costs, increased production costs (fertiliser and animal feed prices) and climate events.

[2] In Luxembourg, the underlying index is a sub-aggregate of the general price index excluding petroleum products and other products whose prices are directly linked to international markets. Electricity, on the other hand, is included in the underlying index.

[3] The price of crude oil quoted in USD rose by +11% in June, with the depreciation of the dollar against the euro limiting the increase expressed in EUR to 9%.

[4] Announcements made in the general policy statement on the state of the nation on 13 May 2025 and the draft bill of the Government Council of 24 July 2025. The measures include a state contribution of EUR 150 million towards network usage costs and a contribution of EUR 120 million to the compensation mechanism system for 2026.

[5] Compared to the latest STATEC forecasts, based on Economic Report 1-2025, the assumption for network costs is therefore 3.9 euro cents/kWh lower (see Draft Bill 6922MLE – Commentary on the articles, Ad Article 2) and that relating to the compensation mechanism is lower by 3.63 euro cents/kWh (falling to 0 euro cents/kWh instead of its 2021 level of 3.63 euro cents/kWh). However, the exact effects on 2026 pricing for electricity network use will only be known in the autumn, once the regulatory procedure for setting tariffs has been completed.

[6] Without measures on electricity prices, inflation for 2026 would be 0.5 percentage points higher, at 1.9% – the level forecast by STATEC in its Economic Report 1-2025.

Deux scénarios alternatifs de prix énergétiques

Press office| Tél 247-88455 | press@statec.etat.lu

This publication was produced by Jill Schaul and Gabriel Gomes.

STATEC would like to thank all contributors who helped make this publication possible.

The total or partial reproduction of this publication is authorised provided that the source is acknowledged.

Last update