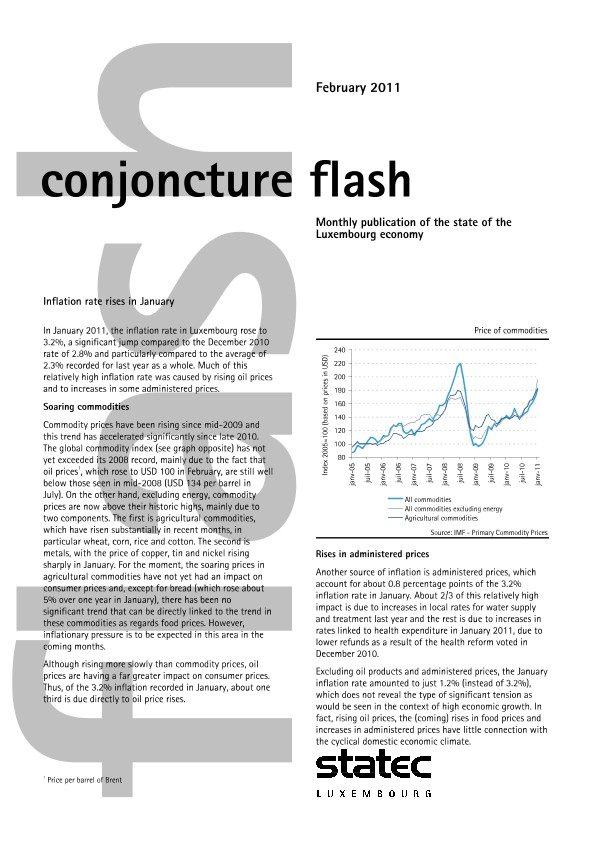

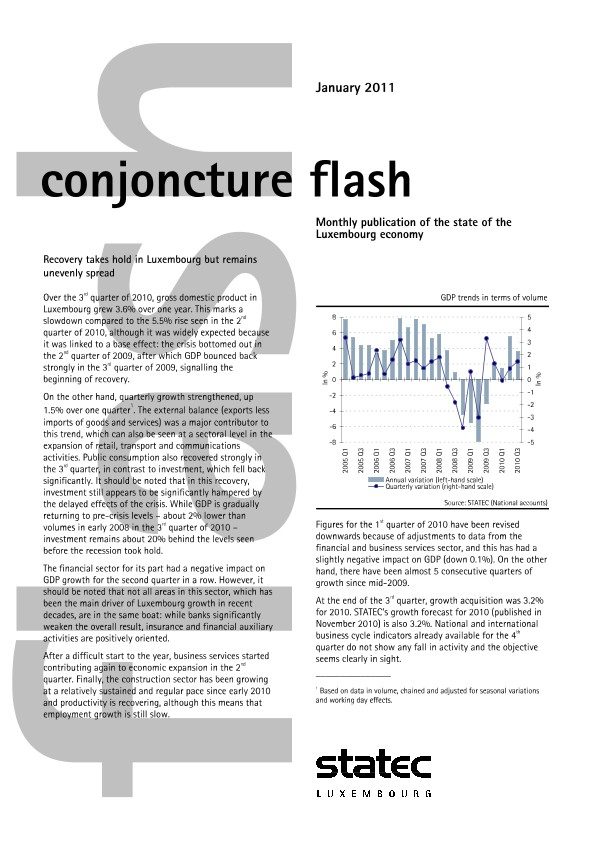

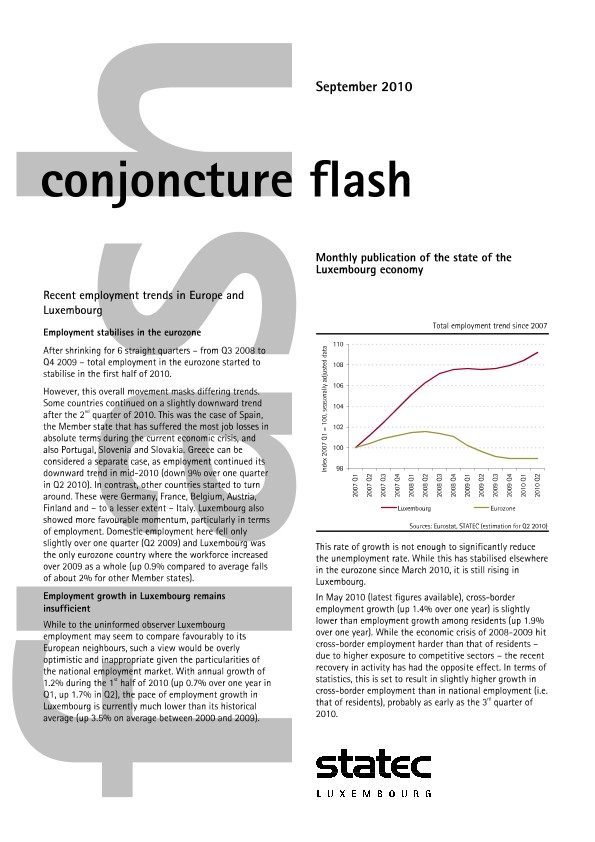

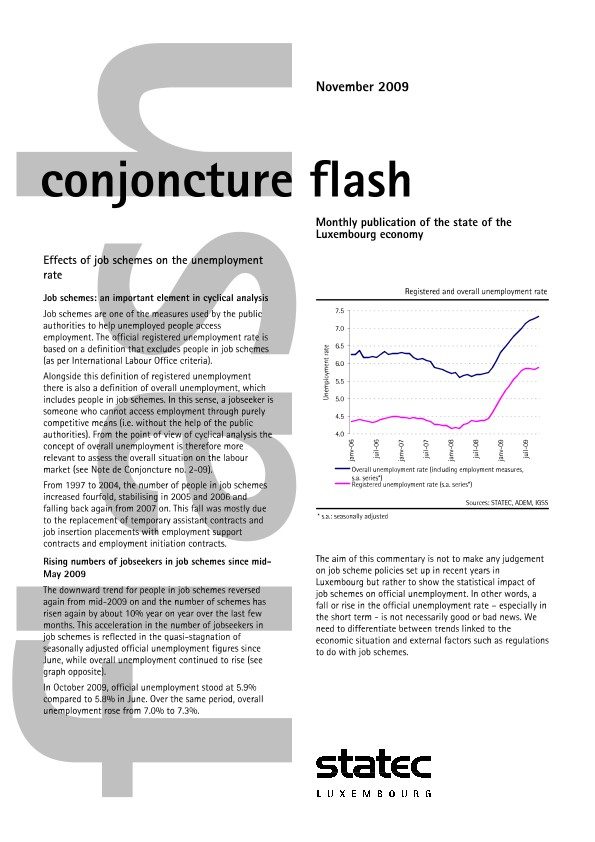

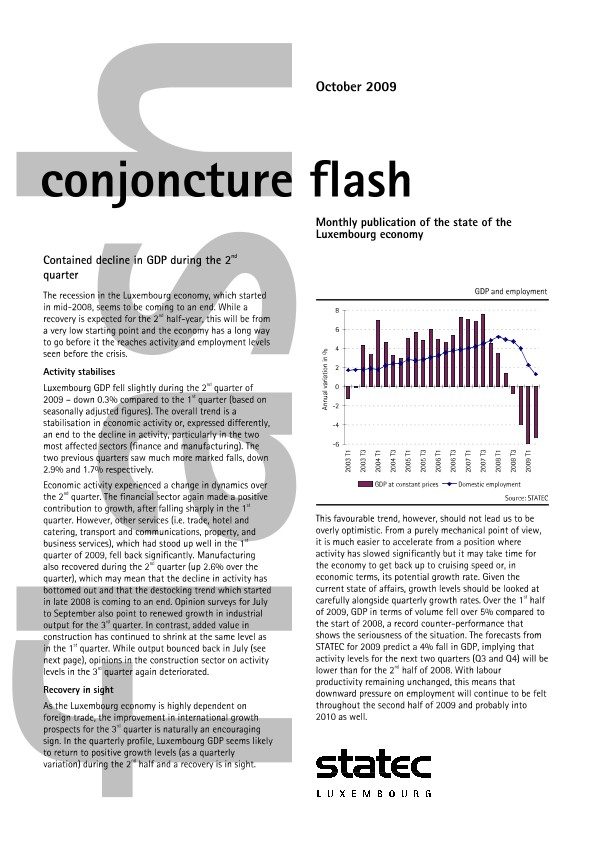

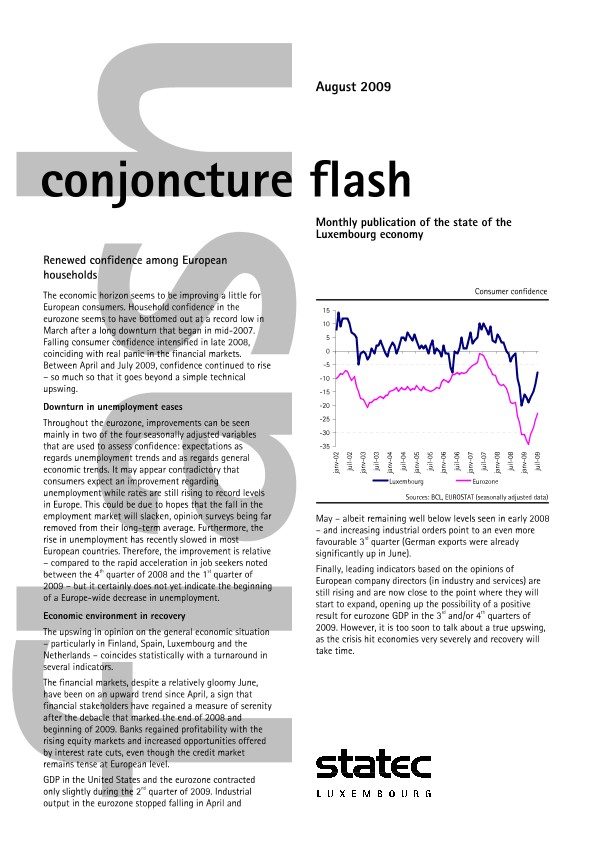

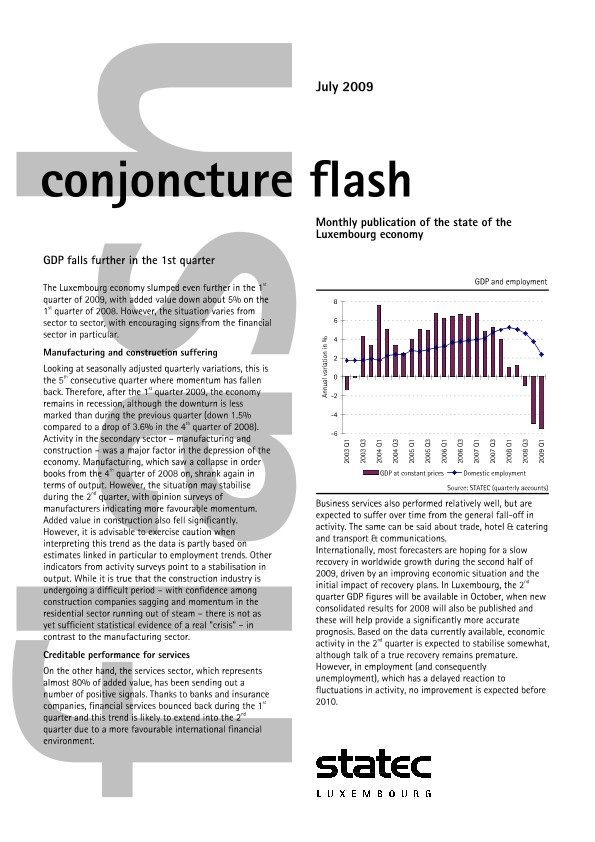

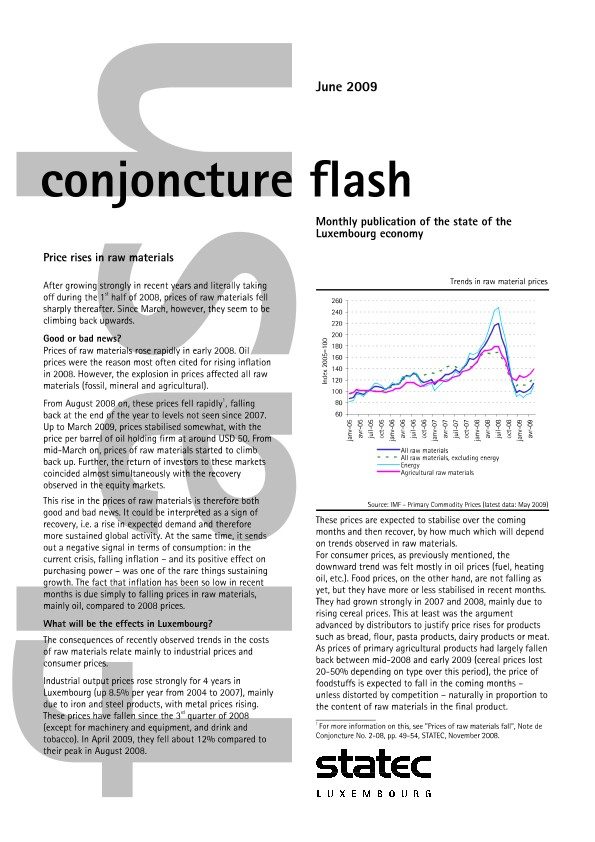

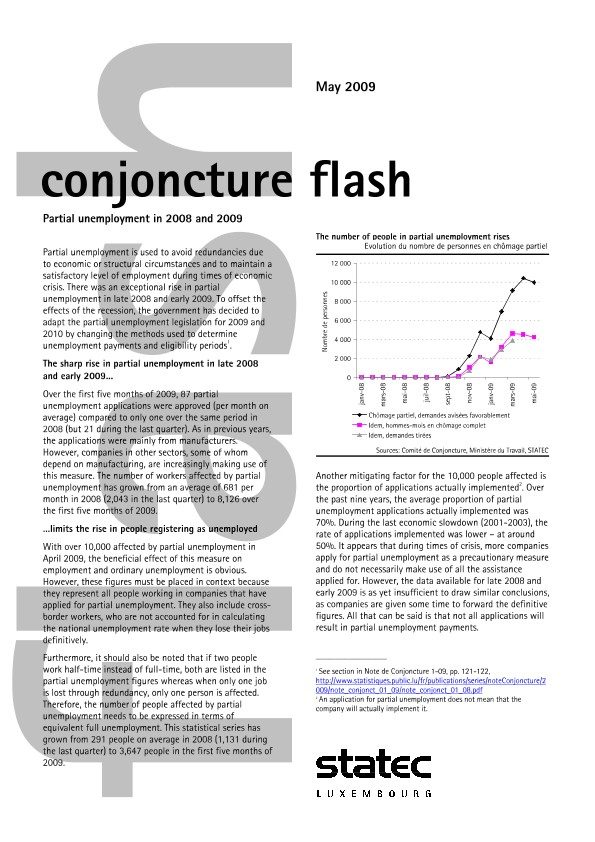

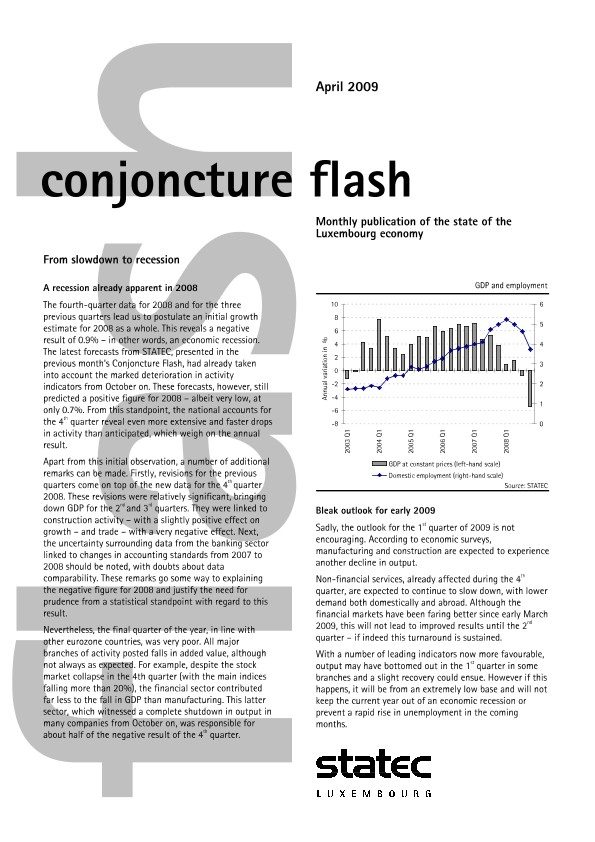

Other languages

PDF Conjoncture Flash December 2014

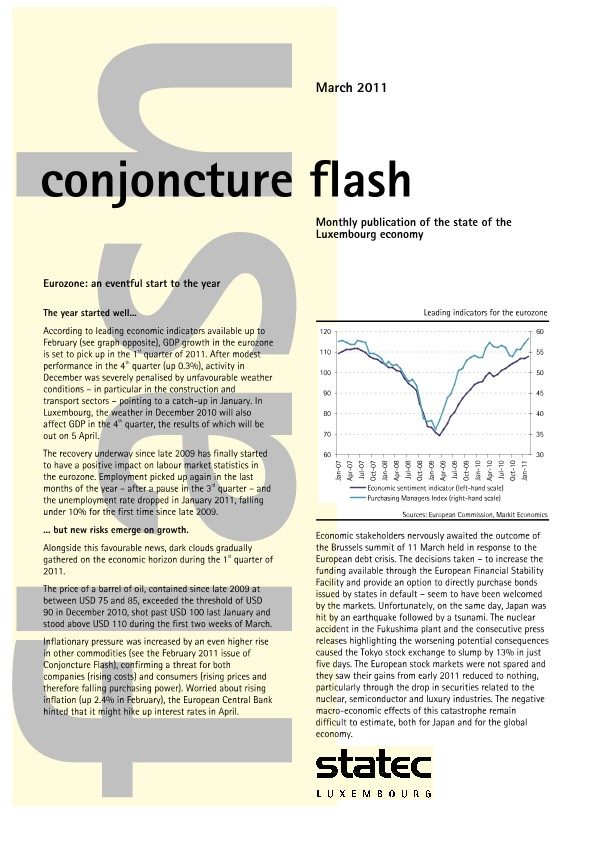

The end-of-year economic climate features contrasting indicators and signals. The downturn in confidence indicators in the euro zone seems to be over, the drop in oil prices should reduce energy bills for households and companies, and employment continues to recover. However, the European environment remains marked by deep-seated weaknesses, particularly as regards investment and economic governance. Europe is also set to take a stricter line with Luxembourg on the issue of tax harmonisation.

-

International 1/2: World trade in goods recovers

-

International 2/2: Upswing

-

Manufacturing: Sluggish investment

-

Construction: Hiring forecasts materialise

-

Labour market: Temporary employment recovers in the 3rd quarter

-

Consumer prices: Inflation pushed even further down by oil

-

Consumption: No rush to buy cars

PDF Conjoncture Flash November 2014

Since spring, international organisations have downgraded their growth forecasts for the euro zone to 0.8% for 2014 and 1% for 2015. With growth acquisition at about 3% by the end of second quarter, STATEC's forecast of a GDP in volume increase of 2.9% in 2014 for Luxembourg may seem too low. However, a number of factors give grounds for caution...

-

Manufacturing: Prolonged stagnation

-

Construction: A more favourable third quarter

-

Consumption: From thinking to buying is just one step

-

Financial sector: Funds continue to perform well

-

Labour market: Fewer bankruptcies in 2014

-

Inflation: Widespread disinflation

-

International: Euro zone: minimal growth

PDF Conjoncture Flash October 2014

GDP growth was relatively satisfactory in the 2nd quarter of 2014. Although the quarterly national accounts have been significantly revised, the new results do not substantially affect the economic momentum observed, specifically the recovery was has been underway since mid-2012. However, while activity held up favourably in the first half of 2014, the economic climate has been worsening since the summer.

-

Manufacturing: Prices recover somewhat

-

Construction: Permits remain at similar levels

-

Financial sector: Autumn starts with stock markets taking a dive

-

Labour market 1/2: Employment up except in temporary employment

-

Labour market 2/2: Unemployment growth tails off

-

Price: Inflation expected to fall (except in Luxembourg)

-

International: A better profile for Luxembourg

PDF Conjoncture Flash Septembre 2014

The unemployment rate fell in August but continues to trend upwards. Slower growth in unemployment over recent months and the healthier rate of job creations in 2014 are encouraging signals for the labour market, but a number of signals indicate that this relative improvement might not last.

-

International: The ECB propelled into action

-

Manufacturing: Output stabilises

-

Consumption: Retail improving

-

Non-financial services: Running out of steam?

-

Labour market: A rather negative signal in temporary employment

-

Inflation: Oil continues to dampen inflation

-

Public finances: Tax receipts: up 6% over one year in late August

PDF Conjoncture Flash August 2014

The 2nd quarter of 2014 was marked by lower than expected GDP growth in the eurozone. This stagnated, due notably to the counter-performance of its three leading economies. Over 2014 as a whole, growth is not expected to exceed 1%, below the trajectory anticipated last spring.

-

Manufacturing:Trend remains favourable in the 2nd quarter

-

Construction: A purely technical pull back?

-

Financial sector (1/2): Positive signals for the 2nd quarter

-

Financial sector (2/2): More flexibility in business lending

-

Labour market: Unemployment continues to rise

-

Inflation: A less significant "sales" effect in 2014

-

Consumption: Registrations start to recover

PDF Conjoncture Flash July 2014

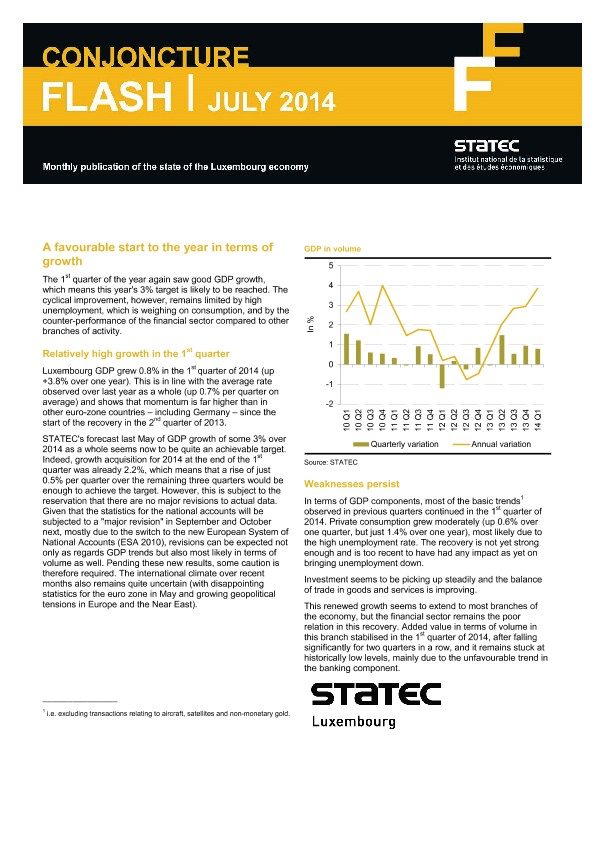

The 1st quarter of the year again saw good GDP growth, which means this year's 3% target is likely to be reached. The cyclical improvement, however, remains limited by high unemployment, which is weighing on consumption, and by the counter-performance of the financial sector compared to other branches of activity.

-

International: Negative signals in Germany

-

Investment: Investment rallies somewhat

-

Financial sector: A stormy summer on the markets

-

Labour market: Cross-border employment trending more favourably

-

Inflation: Food prices falling

-

Wages: Slight rise in wage costs in the 1st quarter

-

Public finances: Tax receipts down slightly

PDF Conjoncture Flash June 2014

Recent economic indicators for the euro zone give signs of improvement overall. Activity should become steadier in the 2nd quarter and unemployment should continue to fall, linked in particular to the recovery recorded in the southern countries. Risks are still present, however, particularly with regard to public debt and the slight increase in prices.

-

Manufacturing: Output intensifies

-

Construction: Towards less dynamic growth

-

Consumption: Registrations picked up in May

-

Financial sector: From credit to confidence

-

Labour market (1/2): Employment is increasing but not accelerating

-

Labour market (2/2): Sharp increase in vacant positions in the 1st quarter

-

Consumer prices: Inflation still very low in May

PDF Conjoncture Flash May 2014

Over recent months, the financial sector has seen relatively high wage growth, in contrast with the disappointing data on the added value of activities in this sector. STATEC has attempted to estimate the impact of exceptional redundancy payments on wage costs in the sector and in the economy overall. The impact, determined by cross-tabulating individual data on personnel costs and redundancy plans in the banking sector, appears significant but not sufficient to explain on its own the rising wages in the sector. However, the extent of the increase is probably underestimated by the method used.

-

Manufacturing: Manufacturing prices continue to fall

-

Construction: Construction prices likely to rise

-

Financial sector: Bank balance sheets slimming down

-

Labour market (1/2): More job creation

-

Labour market (2/2): Temporary employment on the up

-

Inflation: Disinflationary trends confirmed

-

International: Eurozone - moderate growth in the 1st quarter

PDF Conjoncture Flash April 2014

With GDP rising 0.7% in the last quarter of 2013, economic growth for the year as a whole was a little over 2%. Non-financial services, manufacturing and construction largely sustained activity in late 2013, but financial services unfortunately did exhibit the same momentum. 2014 will benefit from relatively high growth acquisition, which will see GDP grow more than in 2013.

-

Manufacturing: A late but pronounced recovery

-

Construction: The sector gets back on track

-

Consumption: Registrations - A disappointing 1st quarter

-

Financial sector: Contrasting trends in lending, which is generally sluggish

-

Labour market: Unemployment growth slows

-

Price: Gap with neighbouring countries narrowing

-

Public finances: Public receipts relatively well-placed in early 2014

PDF Conjoncture Flash March 2014

The indicators for consumption showed relatively contrasting results in late 2013 and early 2014. While the economic environment has improved somewhat, consumption remains lacklustre.

-

Manufacturing: Positive signal from investments

-

Manufacturing and Construction: A very good end to 2013

-

Financial sector (1/2): Rising number of banks

-

Financial sector (2/2): Favourable winds for funds

-

Labour market: Unemployment stabilising – apparently

-

Price: Inflation nose-dives

-

International: Trade in goods slows slightly

PDF Conjoncture Flash February 2014

Economic growth in the euro zone picked up to a certain extent in late 2013 with less unequal distribution among member states. Luxembourg's neighbours were among the most dynamic, an encouraging signal for external demand for Luxembourg exports. While this recovery in the euro zone has been confirmed, it remains very moderate and is unlikely to pick up any further in the coming quarters.

-

Manufacturing: Prices continue to drop

-

Construction: Progressive consolidation

-

Non-financial services: Growing optimism

-

Financial sector: Insurance premiums fall slightly in 2013

-

Labour market: Job creations remain insufficient

-

Inflation: Less inflation on the horizon

-

Property: Under-supply of apartments

PDF Conjoncture Flash January 2014

In the 3rd quarter of 2013, GDP growth was less than in the previous quarter but overall confirms the recovery that started in late 2012. These figures, together with the favourable trend of other indicators in late 2013, point to growth of at least 2.0% over the past year.

-

Manufacturing: Europe-wide recovery

-

Construction: A better end to the year ended than the start

-

Consumption: 2013 - a mediocre year for registrations

-

Financial sector: Banking income: a significant "value" effect

-

Labour market: Unemployment slowing but not halted

-

Prices (1/2): Inflation slows in 2013

-

Prices (2/2): Uneven performance in commodities

PDF Conjoncture Flash December 2013

GDP growth in the euro zone for the third quarter of 2013 was confirmed at 0.1%. In order to achieve the forecast drawn up by the European Commission in November – predicting a decline of 0.4% in euro-zone GDP over 2013 as a whole – all Member states are set to turn in a performance of at least 0.2% over the last quarter of the current year.

-

Manufacturing : Widespread but general recovery

-

Construction : Growing optimism

-

Transport : Air transport results take off

-

Financial sector : UCIs recover after a difficult summer

-

Inflation : Services contribute greatly to inflation

-

Labour market : Partial unemployment rises slightly at the end of the year

-

Hotel and catering sector : The sector beefs up again

PDF Conjoncture Flash November 2013

The main scenario adopted by STATEC forecasts slack growth in the euro zone in 2014, leading to a 1.2% rise in GDP in volume, assuming that the financial crisis will continue to subside with no major upsets.

-

International : Eurozone: a return of timid growth

-

Manufacturing and construction : Output is up but remains low

-

Construction : Fewer homes but more building

-

Consumption: Recent rally in registrations

-

Inflation : Oil prices have driven inflation below 2%

-

Labour market : A positive signal for temporary employment

-

Financial sector : Insurance: income lower since the 2nd quarter

PDF Conjoncture Flash October 2013

GDP grew quite strongly in the 2nd quarter of 2013, a trend partly linked to the exceptionally weak activity in the 1st quarter. A moderate recovery seems to be setting in, after a rather gloomy 2012. This upswing in activity is currently apparent in foreign trade, while domestic demand – private consumption and investments – is still showing signs of weakness.

-

Manufacturing and construction : Disappointing results in July

-

Financial sector : Banks - stagnating revenues

-

Non-financial services : Overall improvement in confidence

-

Labour market : Unemployment growth eases

-

Inflation : Less pressure on prices

-

Wages : Acceleration likely to be temporary

-

Foreign trade : Global trade sluggish

PDF Conjoncture Flash September 2013

The business cycle indicators for the 1st half of the year point to a highly unfavourable trend in household consumption in Luxembourg. A number of recent developments, however, hold out the hope of a more favourable trend in the long term.

-

Manufacturing : Few tensions on prices

-

Construction : Construction prices: moderate rise

-

Real estate : Apartments: higher price rises

-

Financial sector : UCIs: panic in June

-

Labour market (1): Unemployment falls in August

-

Labour market (2): Fewer applications for partial unemployment

-

Inflation : Fruit and vegetables peak in July

PDF Conjoncture Flash August 2013

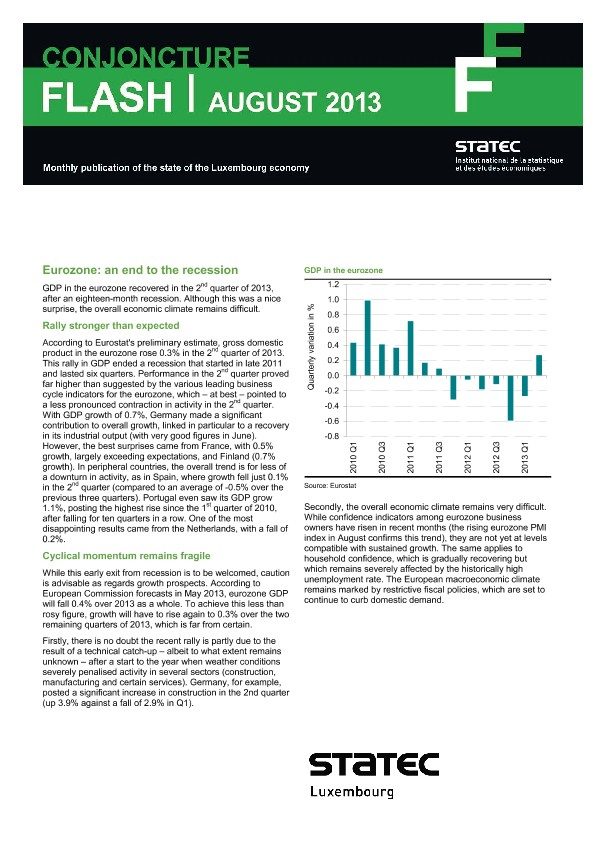

GDP in the eurozone recovered in the 2nd quarter of 2013, after an eighteen-month recession. Although this was a nice surprise, the overall economic climate remains difficult.

-

Manufacturing : Output disappointing in the 2nd quarter

-

Construction : A very tentative recovery

-

Consumption : Registrations continue to fall

-

Financial sector : Contrasting trends in deposits

-

Labour market : Fewer vacancies notified to ADEM

-

Inflation : A significant "sales" effect in 2013

-

Public finances : Tax receipts: up 5.5% over the first 7 months

PDF Conjoncture Flash July 2013

Since the publication of the last Note de conjoncture (NDC 1-13) in May 2013, the economic situation has changed, as has the outlook for the rest of 2013 and 2014. A number of elements are likely to affect the forecast, the detailed results of which will be included in the next Note (NDC 2-13) to be published in November 2013.

-

Manufacturing : Improvement remains to be confirmed

-

Construction : Increases in workforce numbers in the offing?

-

Non-financial services : Services sector more optimistic

-

Financial sector : Banking income recovers in the 2nd quarter

-

Wages : Continued modest wage growth

-

Labour market : Sharp hike in unemployment in the 1st half

-

Inflation : No noticeable slowdown in Luxembourg

PDF Conjoncture Flash June 2013

Industrial output in the eurozone has been recovering since early 2013, mainly due to Germany and the automobile industry, while the bad weather temporarily favoured energy output. Luxembourg's performance was rather disappointing until April but manufacturers' opinions rose sharply in May, a trend that remains to be confirmed.

-

International : Eurozone: contraction of activity levels off

-

Construction : After the cold, the rain

-

Real Estate : Apartment prices moderate somewhat

-

Financial sector (1) : Stormy waters on the stock markets

-

Financial sector (2) : UCIs: positive underlying trend

-

Labour market : Employment stalls

-

Inflation : Alcohol and tobacco: relatively modest price rises

PDF Conjoncture Flash May 2013

After recording almost zero growth in 2012 (up 0.3%), the Luxembourg economy is expected to see a modest and very gradual recovery, with GDP growth set to rise to 1.0% in 2013 and 2.3% in 2014.

-

International : Eurozone: lingering recession

-

Construction : Residential sector props up construction

-

Tourism : Overnight stays up substantially

-

Labour market (1) : Huge momentum in female employment

-

Labour market (2) : The number of vacancies remains high

-

Inflation : Food more expensive

-

Public finances : Public receipts grow strongly in early 2013: a temporary phenomenon

PDF Conjoncture Flash April 2013

The Luxembourg economy saw very weak growth in 2012, ending however with a relatively high increase in GDP in the 4th quarter. This end-of-year recovery was largely due to performance in non-financial services. The financial sector remains sluggish, with no return to high growth in the short term expected.

-

Construction : Bad times for construction

-

Consumption : Fall in new car registrations (expected)

-

Non-financial services : Confidence seems to be gradually returning

-

Labour market : Fall in subsidised jobs pushes unemployment up

-

Wages : Redundancies weigh on wage costs

-

Inflation : Price falls in raw materials

-

International- Eurozone : Limited tensions on government bonds

PDF Conjoncture Flash March 2013

The last few weeks have been marked by renewed cause for concern as regards the economic outlook in the eurozone. Alongside the threats weighing on southern European countries (Italy and Cyprus) which affected market investors, the economic surveys at the end of the 1st quarter show a slump in business confidence.

-

Manufacturing : Persistent downturn

-

Financial sector 1/2 : Contrasting upswing in confidence

-

Financial sector 2/2 : UCIs: Luxembourg consolidates its top ranking

-

Employment : Employment continues to fall in the eurozone

-

Inflation : Slowdown less severe in Luxembourg

-

Real Estate : Strong demand for apartments

-

Bankruptcies : Job losses linked to bankruptcy remained significant in 2012

PDF Conjoncture Flash February 2013

2012 ended badly for the eurozone, with GDP falling sharply in the 4th quarter. The forecasts for 2013 indicate virtual stagnation, even though there have been some recent positive signs pointing to more favourable developments.

-

Manufacturing : Output falls 6% in 2012

-

Construction 1/2 : Gloomy economic situation in 2012

-

Construction 2/2 : Licensed to build

-

Financial sector : Insurance receives a boost

-

Labour market : Temporary employment continues to fall

-

Consumption : Consumers worried about their future

-

International trade : Global trade rallies in November 2012

PDF Conjoncture Flash January 2013

Economic activity in Luxembourg fell in most sectors during the 3rd quarter and continues to suffer from the sluggishness in domestic demand. The international climate is also expected to remain unfavourable in the 4th quarter.

-

Manufacturing : No rally expected in the 4th quarter

-

Financial sector : Sustained growth in UCIs

-

Non-financial services : Businesses a little more confident

-

Labour market : Unemployment rises considerably in late 2012

-

Wages : Real wage costs continue to fall

-

Inflation : Prices rose 2.7% in 2012

-

Consumption : Registrations rally temporarily

PDF Conjoncture Flash December 2012

Opinion surveys conducted among businesses in the eurozone have been trending more favourably of late, catching up with the renewed confidence seen in the stock markets since the summer of 2012. For households, however, which continue to suffer from the difficult labour market, the outlook has yet to improve.

-

Manufacturing 1/2 : Output falls slightly in the 3rd quarter

-

Manufacturing 2/2 : Investment set to fall sharply in 2013

-

Construction : Confidence grows

-

Financial sector : Slight improvement

-

Employment : Employment falls again in the eurozone

-

Inflation : The inflation differential widens again

-

Wholesale and retail trade : A positive signal for retail sales

PDF Conjoncture Flash November 2012

While the results expected for Luxembourg in 2012 have been revised slightly upwards in STATEC's latest forecasts, these also include a significant downward revision for 2013. The general profile drawn up by these forecasts is that of continuing low growth – well below average past performance – rising just 0.5% in 2012 and 1.0% in 2013.

-

International1/2: Recession confirmed in the eurozone

-

International 2/2: More moderate growth in emerging countries

-

Manufacturing: Recent price falls

-

Construction: Fewer authorisations in the non-residential sector

-

Financial sector: A good 3rd quarter for UCIs

-

Employment: Working hours fall

-

Unemployment: Unemployment picks up again in the Greater Region

PDF Conjoncture Flash October 2012

Recently published growth figures give a rosier picture of the economic climate in early 2012, particularly in the financial sector. However, they also reveal worrying trends in other sectors and come with a negative outlook for the 3rd quarter. Growth forecasts for next year are also in doubt, with more pessimistic projections for the eurozone as a whole.

-

Manufacturing: Bearish trend continues

-

Construction: Negative signal in the 3rd quarter

-

Consumption: New car registrations stall

-

Financial sector: Confirmed growth in insurance

-

Employment: Employment recovers slightly in the 1st half of 2012

-

Wages: Low wage growth in the 2nd quarter of 2012

-

International: Less pressure on southern Europe

PDF Conjoncture Flash September 2012

The economic outlook as revealed by economic surveys carried out over the summer is marked by gloominess and point to a recessionary climate. While the financial markets seemed to have responded relatively well to the decisions made at European level, these effects have not yet filtered down to the real economy.

-

Real Estate : Apartment sales hold up well

-

Consumption : Negative signals

Employment : Employment in the eurozone no longer falling

Unemployment : Unemployment recedes very slightly in August

Price : Black gold and yellow gold weigh on inflation

Financial sector : Stock markets bounce back

PDF Conjoncture Flash August 2012

After stabilising in the 1st quarter of 2012, eurozone GDP again contracted in the 2nd quarter (down 0.2% on the previous quarter). Although the eurozone is not strictly speaking in a technical recession – which would require two consecutive quarters of falling GDP – it is well on the way. The cyclical indicators available at the start of the 3rd quarter hold out little hope of escaping a further drop in GDP in the next quarter.

-

Eurozone : Leading indicators at lowest point

-

Manufacturing : No improvement in sight

-

Construction : Persistent decline

-

Financial sector : UCIs: A stagnant 2nd quarter

-

Labour market : Employment in finance remains dynamic

-

Price : Diverging trends in raw materials

-

International trade : Trade in goods falls in the eurozone

PDF Conjoncture Flash July 2012

The results for the 1st quarter of the current year and the outlook for the 2nd quarter indicate that economic activity is weakening in Luxembourg and throughout the eurozone. Consequently, growth forecasts for 2012 and 2013 have been revised downwards.

-

Manufacturing : Downbeat forecast

-

Construction : Downturn confirmed

-

Wholesale and retail trade : Contrasting trends in retail

-

Non-financial services : Minimum service

-

Labour market : Slight rise in assisted jobs

-

Inflation- wages : Real wages fall

-

Public finances : Tax receipts down

PDF Conjoncture Flash June 2012

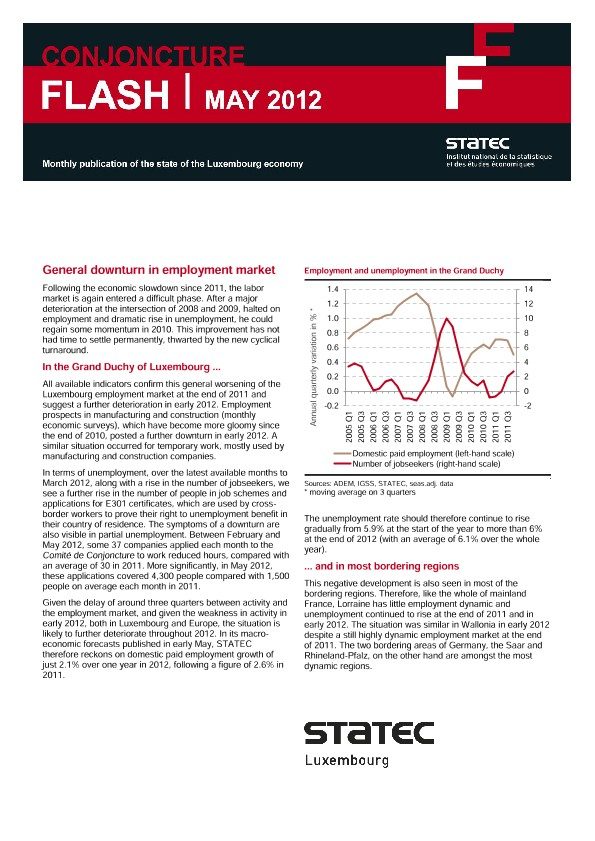

Following the economic slowdown since 2011, the labor market is again entered a difficult phase. After a major deterioration at the intersection of 2008 and 2009, halted on employment and dramatic rise in unemployment, he could regain some momentum in 2010. This improvement has not had time to settle permanently, thwarted by the new cyclical turnaround.

-

Manufacturing : Confidence: after a fall … freefall

-

Real Estate : Prices remain high in the 1st quarter

-

Financial sector : A good start to the year for insurers

-

Business services : Strong growth in early 2012

-

Bankruptcies : Considerable job losses due to bankruptcy in 2011

-

Inflation : Correction in oil and fuel prices

-

Forecasts : Weak growth in 2012 and 2013

PDF Conjoncture Flash May 2012

Following the economic slowdown since 2011, the labor market is again entered a difficult phase. After a major deterioration at the intersection of 2008 and 2009, halted on employment and dramatic rise in unemployment, he could regain some momentum in 2010. This improvement has not had time to settle permanently, thwarted by the new cyclical turnaround.

-

International : Eurozone: between stagnation and recession

-

Manufacturing : Investment expected to rise in 2012

-

Consumption : Retail sales holds up well

-

Non financial services : Contradictory signals

-

Financial sector : A boost for funds in the 1st quarter

-

Wages : Restrained rise in wages

-

Public finances : Public debt still a source of concern

PDF Conjoncture Flash April 2012

GDP grew slightly in Q4 2011, up 0.2% on Q3 (up 0.8% over one year). This, combined with the results for the first 3 quarters of 2011 (which were revised slightly upwards), ultimately resulted in GDP growth of 1.6% for 2011 as a whole, after rising 2.7% in 2010 (and falling 5.3% in 2009).

-

Manufacturing : No clear direction on prices

-

Construction : Slowdown

-

Financial sector (1) : Fewer loans to non-financial companies

-

Financial sector (2) : Confidence rises (temporarily?)

-

Labour market : Cross-border workers hold half of all jobs

-

Inflation : Food prices relatively calm

-

International : PMI falls sharply in April

PDF Conjoncture Flash March 2012

Recent months have been marked by a progressive improvement in the European financial environment. While this longed-for ray of sunshine holds out the long-term prospect of a more favourable environment for European growth, economic activity in early 2012 has remained hampered by relatively gloomy indicators.

-

Manufacturing : Output down

-

Construction : 2011 a relatively satisfactory year

-

Real estate : No crisis for apartment prices

-

Labour market (1) : Employment slows slightly in 2011

-

Labour market (2) : Unemployment rises in early 2012

-

Inflation : Administered prices contribute little to the NCPI

-

Consumption : Favourable trend in car sales

PDF Conjoncture Flash February 2012

The eurozone ended the year with a slump in GDP in the 4th quarter which few countries escaped. Luxembourg is likely to go down the same road as most of the economic indicators in late 2011 were disappointing.

-

Consumption: Consumers (a little) more confident

-

Credit: Slight tightening of lending conditions

-

Financial sector: UCIs: a turbulent 2nd half

-

Labour market (1) : Less reliance on overtime

-

Labour market (2) : Unemployment continues to rise, as does employment

-

Inflation: Pump prices at their highest

-

Transport: More passengers, less freight

PDF Conjoncture Flash January 2012

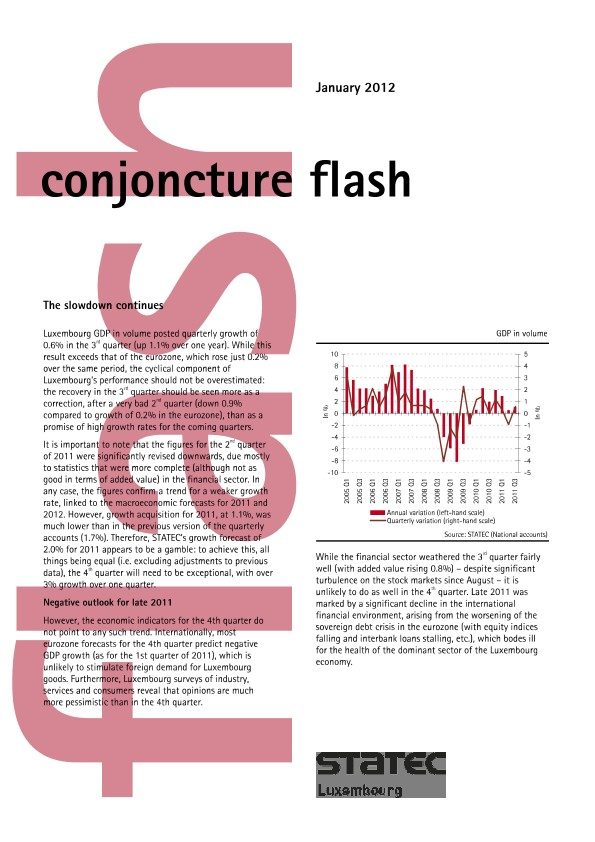

Luxembourg GDP in volume posted quarterly growth of 0.6% in the 3rd quarter (up 1.1% over one year). While this result Luxembourg's performance should not be overestimated: the recovery in the 3rd quarter should be seen more as a correction, after a very bad 2nd quarter (down 0.9% compared to growth of 0.2% in the eurozone), than as a promise of high growth rates for the coming quarters.

Eurozone : Leading indicators recover

Manufacturing : Bleak outlook

Construction : Projects despite the crisis

Financial sector : Disappointing results for banking employment

Labour market : Overall decline in the labour market

Inflation and wages : The main price trends in 2011

Foreign trade : Global trade falls at the start of 2012

PDF Flash 2011-12

-

Construction: morale good but not results

-

Financial sector (1): respite for UCIs in October

-

Financial sector (2): employment grows slightly

-

Labour market (1): employment falls throughout the eurozone

-

Labour market (2): partial employment on the up again

-

Inflation and wages: wage indexation postponed

-

Property: asking prices for apartments fall

PDF-Flash-2011-11-EN

-

Manufacturing: prices stabilise

-

Construction: tensions over housing prices

-

Financial sector: fees rise unexpectedly in the 3 quarter

-

Non financial services: prospects down significantly

-

Labour market: number of bankruptcies remains high in early 2011

-

Inflation and wages: prices in services adapted to indexation

-

Consumption: householders worried

PDF-Flash-2011-10-EN

-

Manufacturing: output bounces back in July

-

Construction: positive signal from planning authorisations

-

Financial sector: interbank lending continues to recover

-

Labour market (1): employment remains dynamic in the second quarter of 2011

-

Labour market (2): sharp rise in new registrations with ADEM

-

Inflation - Wages: slowdown in average wage costs

-

Transport: contrasting indicators in air transport

PDF-Flash-2011-09-EN

-

Manufacturing: Moderation of business outlook

-

Construction: Prospects remain favourable

-

Financial sector: Meltdown of funds in August

-

Labour market (1): High increase in unemployment

-

Labour market (2): A very good beginning to the year, but then ...

-

Inflation - Wages: Respite on the price of raw materials

-

Consumption: Car registrations up over the summer

PDF-Flash-2011-08-EN

-

Manufacturing: stagnant production

-

Construction: favourable global economy

-

Financial sector: banking employment continues downward

-

Consumption: (temporary) rise in consumer morale

-

Labour market: negative signals

-

Inflation: brake on inflation

-

Foreign trade: stagnation in global exchange of goods

PDF-Flash-2011-07-EN

-

Manufacturing: Price rises likely to slow

-

Construction: Construction prices: the recovery is confirmed

-

Financial sector: Banking income disappointing in the 2nd quarter

-

Public finances: Is growth in receipts set to tail off?

-

Labour market: Is the unemployment trend set to reverse?

-

Inflation: Inflation forecasts: 3.3% in 2011 and 2.1% in 2012

-

International environment: Stock market indices fall

PDF-Flash-2011-06-EN

-

Manufacturing: Moderate increase in output

-

Construction: A satisfactory start to the year

-

Financial sector: Banks: less weight internationally

-

Transport: Transport loses speed

-

Labour market: Employment trends for cross-border and resident workers

-

Inflation: Inflation becomes widespread

-

Foreign trade: Impressive recovery in exports of goods

PDF-Flash-2011-05-EN

-

Manufacturing: economic situation remains buoyant in manufacturing

-

Property: record number of transactions in the 4th quarter

-

Financial sector: UCIs: Luxembourg leads the pack

-

Consumption: disappointing start to the year for car sales

-

Labour market: unemployment falls in early 2011

-

Inflation: increasing tension on food prices

-

Foreign trade: trade sluggish in the 2nd quarter

PDF-Flash-2011-04-EN

-

Manufacturing: favourable prospects for the 1st quarter

-

Construction: snow in December, renewed activity in January

-

Financial sector: Interbank lending stagnates

-

Consumption: consumer morale peaks

-

Labour market: employment recovers in all branches

-

Inflation: factors affecting inflation since 2010

-

Public finances: a successful quarter

PDF-Flash-2011-03-EN

-

Manufacturing: Price rises in industrial products

-

Construction: More planning permission, but for smaller buildings

-

Financial sector: UCIs - adverse effects of the dollar in January

-

Labour market: Employment on the rise in Europe

-

Labour market: More bankruptcies in the financial sector in 2010

-

Inflation: Increased volatility in energy prices

-

Transport: Mixed performance by national airlines in 2010

PDF Conjoncture Flash february 2011

Manufacturing: A disappointing end to the year

Construction : Construction prices grow slightly

Financial sector : Equity growth?

Retail trade : Retail sluggish in the 4th quarter

Labour market : Temporary work recovers significantly in 2010

Wages : Rebound of wage bill

International : European recovery remains modest

PDF Conjoncture Flash January 2011

Manufacturing: Is this slowdown in pace purely temporary?

Construction : A solid recovery

Financial sector : Banking income before provisions down sharply

Labour market (1) : Employment: favourable trend in services

Labour market (2) : Moderate increase in unemployment in 2010

Inflation : Inflationary and deflationary forces

Public finances : Tax receipts improve in 2010

PDF Conjoncture Flash Septembre 2010

Manufacturing: Productivity starts to recover

Property: Apartment prices under pressure

Financial sector: Lacklustre margins

Construction: Luxembourg holds its own

Labour market: Both job applications and job vacancies rise

Inflation - wages: Inflation forecasts: 1.9% in 2011 for NCPI

Transport: More goods, fewer people

PDF Conjoncture Flash August 2010

Manufacturing: production growth is likely to slow

Construction: positive trend

Financial sector: UCIs remain on course

Consumption: consumers confident about the recovery

Labour market: unemployment in Europe reaches its upper limit

Inflation - wages: rise in the underlying inflation rate

Hotel and catering sector: Tourism: 2009 was an unremarkable year

PDF Conjoncture Flash July 2010

Manufacturing: rise in prices linked to iron and steel

Construction: planning permission: a satisfactory first quarter

Financial sector: limited employment perspectives

Consumption: positive signs for car registrations

Labour market: low and disparate growth in employment

Inflation - wages: food prices relatively steady

Foreign trade: trade on the right track

PDF Conjoncture Flash June 2010

Manufacturing: a significant rally – after a sharp fall

Construction: measured optimism

Financial sector: a symbolic rise

Transport: overcast skies in April

Labour market: cross-border employment expected to rise

Inflation - wages: public charges recover

International: worries over European indebtedness

PDF Conjoncture Flash May 2010

Manufacturing: manufacturing starts to recover

Hotel and catering businesses: a difficult year

Financial sector: UCIs stage a comeback

Consumption: a good start to the year in car sales

Labour market: a seasonal fall

Foreign trade (1/2): exports of financial services hold up well

Foreign trade (2/2): e-commerce companies stood up well in 2009

PDF Conjoncture Flash April 2010

Manufacturing: european manufacturers regain confidence

Construction: residential projects fall again in 2009

Financial sector: lower earnings on loans

Inflation: inflation rises 2.3% in March

Labour market (1/2): Labour market comes out of the red...

Labour market (2/2): … but remains sluggish

Foreign trade: exports of goods recover

PDF Conjoncture Flash March 2010

Manufacturing: confirmed turnaround

Construction: back to work

Financial sector: UCIs: a relatively satisfactory result in January

Tourism: a very bad year in 2009

Labour market: unemployment levels off

Inflation - wages: Inflation at 1.5% in February

Transport: recovery after free-fall

PDF Conjoncture Flash February 2010

Manufacturing 1: manufacturing prices fall sharply in 2009

Manufacturing 2: steel production recovers

Construction: construction prices stagnate

Financial sector: banking employment falls slightly in the 4th quarter

Labour market: downturn less than predicted

Inflation - wages: underlying inflation at its lowest level in 10 years

Consumption: sharp slump in confidence must be put in context

PDF Conjoncture Flash January 2010

Manufacturing: the trend remains upward

Construction: a relatively optimistic Luxembourg

Consumption : new car registrations fall in 2009

Financial sector: Contrasted performance compared to the end of 2008

Labour market: unemployment rises again

Inflation - wages: underlying inflation continues to slow

Foreign trade: global trade recovers but the euro zone lags behind

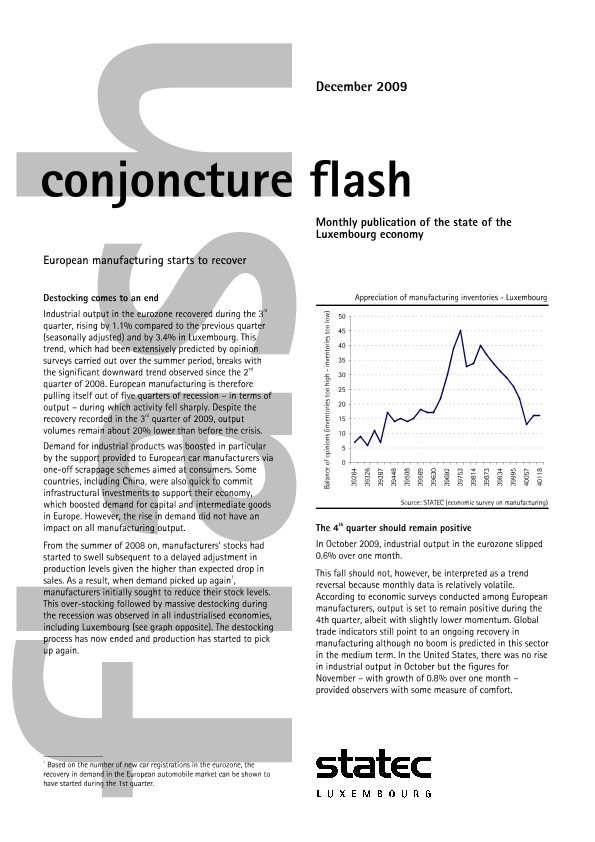

PDF Conjoncture Flash December 2009

Construction: fewer planning authorisations

Housing: apartment prices remain stable

Financial sector: favourable trend for UCIs

Transport: air transport remains in difficulty

Labour market: mixed results for job schemes

Inflation - wages: wages stagnate in early 2009

Consumption: consumers worried about unemployment

PDF Conjoncture Flash November 2009

Manufacturing: no further improvement in November

Construction: recent brightening in prospects

Financial sector: banking employment continues to fall

Tourism: fewer arrivals overnight stays

Labour market: impact of partial unemployment

Inflation - wages: inflation rises in late 2009

International: end to recession in the eurozone

PDF Conjoncture Flash October 2009

Manufacturing: disappointing output levels in July

Construction: a nice surprise

Financial sector: banks benefit from market recovery

Consumption: fewer retail sales

Labour market: employment slows drastically in early 2009

Inflation - wages: little increase in wages in early 2009

International: early recovery in emerging countries

PDF Conjoncture Flash September 2009

Manufacturing: continuing downward pressure on prices

Construction 1/2: fewer planning permits, fewer transactions

Construction 2/2: Luxembourg holds its own

Financial sector: UCIs up in July

Labour market: employment in Europe continues to fall

Inflation - wages: sharp slowdown in food prices

Foreign trade: trade in goods recovers

PDF Conjoncture Flash August 2009

Manufacturing: encouraging prospects for the 3rd quarter

Construction: no improvement in sight

Consumption: falling car sales in Europe

Financial sector: banking employment trends remain down

Labour market: drastic fall in temporary employment

Inflation - wages: underlying inflation slows

Euro zone: GDP contracts slightly during the 2nd quarter

PDF Conjoncture Flash July 2009

Manufacturing: improvement in sight

Construction: contrasting situation in planning permission

Construction: downward pressure on construction costs

Financial sector: the upward trend in the markets continues

Labour market: employment stagnant in early 2009

Inflation - wages: wages fall at the start of the year

Foreign trade: recovery in sight for global trade

PDF Conjoncture Flash June 2009

Manufacturing: has the low point been reached?

Construction: falling activity but less than elsewhere in Europe

Financial sector: a more serene environment

Consumption: confidence grows

Labour market: european unemployment up

Inflation - wages: negative inflation for mid 2009

Transport: air traffic down

PDF Conjoncture Flash May 2009

Manufacturing: output at its lowest during the 1st quarter

Construction: Luxembourg holds its own

Financial sector: banking employment slows even further

Consumption: new car registrations stall

Labour market: slowdown in employment

Inflation - wages: purchasing power rises in 2009

Foreign trade: global trade stabilises at low levels

PDF Conjoncture Flash April 2009

Manufacturing: turbulent times

Construction: mixed opinions on the 1st quarter

Financial sector: markets up since March

Labour market (1): temporary employment falls in late 2008

Labour market (2): unemployment continues to accelerate

Inflation - wages: wages fall in the financial sector

Consumption: consumers demoralised

PDF Conjoncture Flash March 2009

Manufacturing: a dispirited end to 2008

Construction: fewer housing units granted planning permission in 2008

Financial sector: respite for UCIs in January

Services: a less buoyant climate for services

Labour market: sharp slowdown in paid employment in late 2008

Inflation - wages: a technical rise in underlying inflation

Foreign trade: trade deficit rises substantially

PDF Conjoncture Flash February 2009

Manufacturing: industrial prices drop

Construction: output down, moderate price growth

Financial sector: banking employment falls slightly

Consumption: trade in difficulty

Labour market: unemployment growth accelerates

Inflation - wages: wage adjustment due on 1 March 2009

Foreign trade: current account surplus drops

PDF Conjoncture Flash January 2009

Manufacturing: general drop in demand

Construction: a chill in the sector

Financial sector: banks under pressure but holding firm

Consumption: confidence falls further in December

Labour market: unemployment rises sharply in December

Inflation - wages: oil prices responsible for one third of inflation in 2008

Foreign trade: trade in goods slows down

PDF Conjoncture Flash December 2008

Manufacturing: A difficult end to the year expected

Construction: Planning authorisations recover

Financial sector: A turbulent autumn for UCIs

Consumption: Vehicle registrations down

Labour market: Fewer job vacancies

Inflation - wages: Oil shock repercussions

Horeca: Fewer tourists in the 1st half-year of 2008

PDF Conjoncture Flash November 2008

Manufacturing: manufacturers depressed since October

Construction: a difficult end to the year

Financial sector: banking employment holds up…

Consumption: a particularly satisfying 3rd quarter for vehicle sales

Labour market: bad news on short-time working

Inflation - wages: limited wage increases in the 1st half-year

Foreign trade: structural falls in exports of goods

PDF Conjoncture Flash october 2008

Manufacturing: deteriorating prospects

Construction: drop in mortgages

Financial sector: autumn turbulence for UCIs

Consumption: relatively good performance

Labour market: unemployment stable in September at 4.4%

Inflation - wages: food inflation set to slow down

Foreign trade: services still sound in 1st half of 2008

PDF Conjoncture Flash September 2008

Manufacturing: prices again driven by iron and steel

Construction: grants for planning permissions fall again in Q2

Financial sector: a highly troubled summer for the markets

Consumption: confidence rises tentatively in August

Labour market: unemployment in August stable at 4.4%

Inflation - wages: significant downturn in oil prices

Foreign trade: foreign trade sluggish

PDF Conjoncture Flash August 2008 EN

Manufacturing: contrasting results during the 1st half-year

Construction: mixed opinions for the 3rd quarter

Financial sector: a pleasant surprise for banking employment

Consumption: new car registrations recover during the 2nd quarter

Labour market: unemployment continues to rise

Inflation - wages: inflation forecast: 3.9% in 2008 and 3.0% in 2009

Foreign trade: exchange terms fall

PDF Conjconcture Flash July 2008 EN

Manufacturing: stormy waters

Construction: fewer planning permissions granted in Q1

Financial sector: some respite for UCIs in April and May

Consumption: retail trade holds its own during the 1st quarter

Labour market: change of trend

Inflation - wages: slight rise in wages during Q1 2008

Foreign trade: current account surplus falls

PDF Conjconcture Flash June 2008 EN

Manufacturing: output holds up while orders fall back

Construction: a relatively satisfactory first quarter

Financial sector: a difficult 1st quarter for banks

Consumption: Encroaching gloom

Labour market: unemployment of 9.1% in the Greater Region in 2006

Inflation - wages: the unfavourable inflation differential falls

Foreign trade: exports of services: up 12% in 2007

PDF Conjoncture Flash May 2008

Manufacturing: output down in early 2008

Construction: downbeat forecast

Financial sector: a difficult end to 2007 for the insurance sector

Consumption: new vehicle registrations down in the 1st quarter

Labour market: employment in Luxembourg continues to accelerate

Inflation, wages: slowdown in wage growth throughout 2007

Foreign trade: exports of services: up 12% in 2007

PDF Conjoncture Flash April 2008

Manufacturing: Food prices still under pressure

Construction: More housing units anticipated

Financial sector: Slowdown in banking employment

Trade: Mixed performance in retail trade

Labour market: Falling numbers of people in job schemes

Inflation, wages: Price hikes in services

Foreign trade: Stabilisation of the current balance in 2007

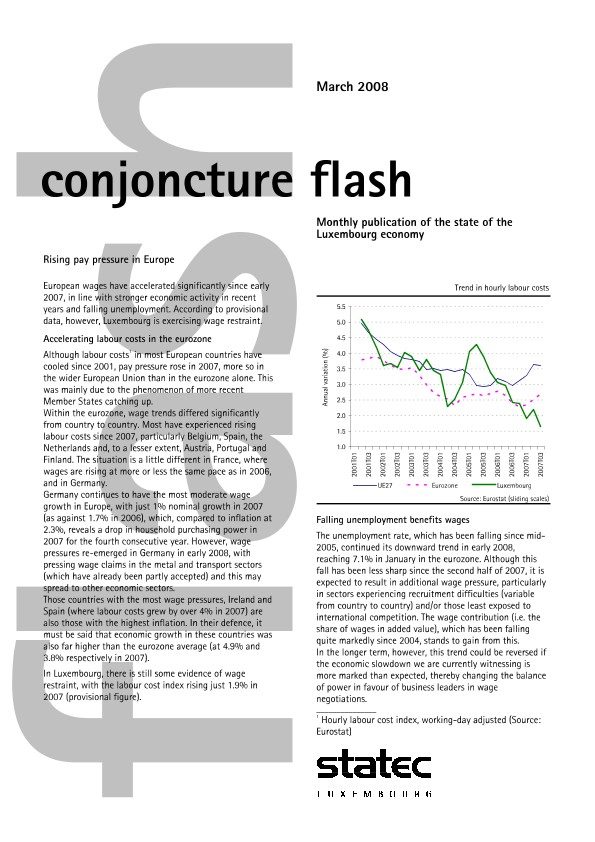

PDF conjoncture flash march 2008

Manufacturing: Measured optimism in a difficult context

Construction: Activity more sluggish in early 2008

Financial sector: A bad start to the year for UCIs

Tourism: A satisfactory 2007

Labour market: Job creations also benefit residents

Inflation, wages: Inflation set to remain high in 2008

Foreign trade: A weakening dollar

PDF Flash February 2008

Construction: Construction prices remain relatively modest

Consumption (1): Slight rise in new vehicle registrations in 2007

Consumption (2): Slump in confidence less severe in Luxembourg

Financial sector: A halt to the rise in UCIs

Labour market: Fall in unemployment since mid-2007

Inflation, wages: Foodstuffs generate more inflation

Foreign trade: Exports of goods more focused on Europe

PDF Flash January 2008

Manufacturing: Less investment in 2008

Construction: A difficult end to the year

Financial sector: Panic sweeps through the markets

Financial sector: Fairly satisfactory results in the banking sector for 2007

Labour market: Employment in Europe continues to accelerate

Wage inflation: Moderate growth in average wage costs

Foreign trade: Current account surplus remains high

PDF EN Conjoncture Flash december 2007

Industry: Prices ease against a backdrop of mixed trends

Construction: Downturn in construction permits in the 3rd quarter

Financial sector: Good results for UCIs in October

Consumption: More new vehicle registrations during the 3rd quarter

Labour market: Employment accelerates

Wage inflation: Wage increase threshold exceeded in November

Foreign trade: Stabilization in terms of trade

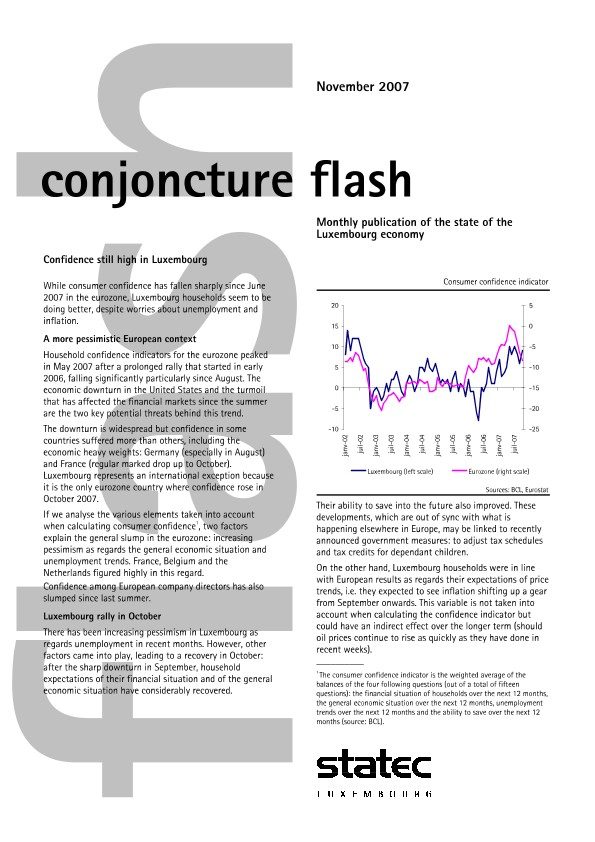

PDF CONJONCTURE FLASH EN 11.2007

Industry: Slight improvement in opinions

Construction: Gloomy outlook

Financial sector: Banking employment peaks

Financial sector : Markets under pressure

Labour market: Employment up by 5.1% in July 2007

Wage inflation: Inflation rises to 2.9% in October 2007

Foreign trade: The euro breaks record after record

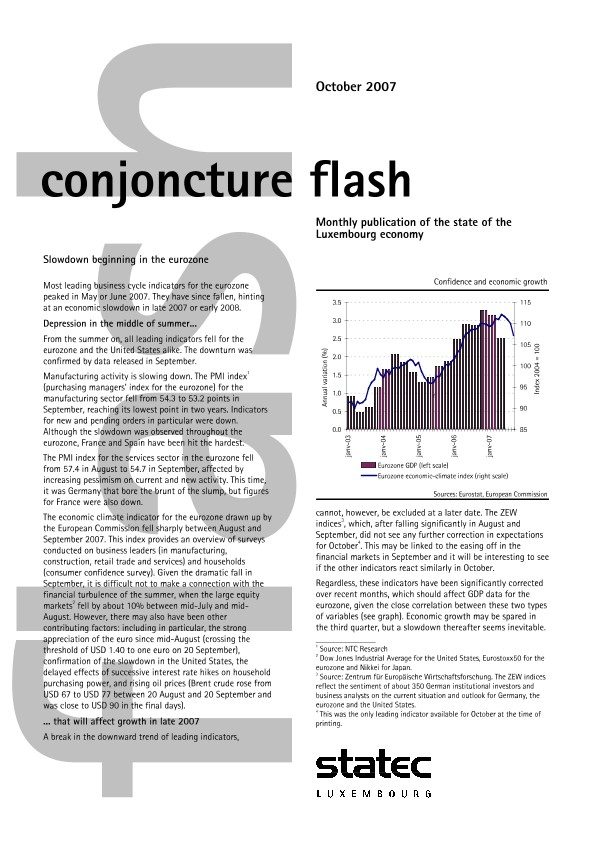

PDF Conjoncture Flash October 2007

Manufacturing: Iron and steel drive production figures

Construction: Civil engineering makes a comeback

Financial sector (1): Banking activity holds its own in the 3rd quarter

Financial sector (2): UCIs affected by financial turbulence

Labour market: Job vacancy rate up in Luxembourg

Wage inflation: Food price tensions

Foreign trade: Current account surplus remains high

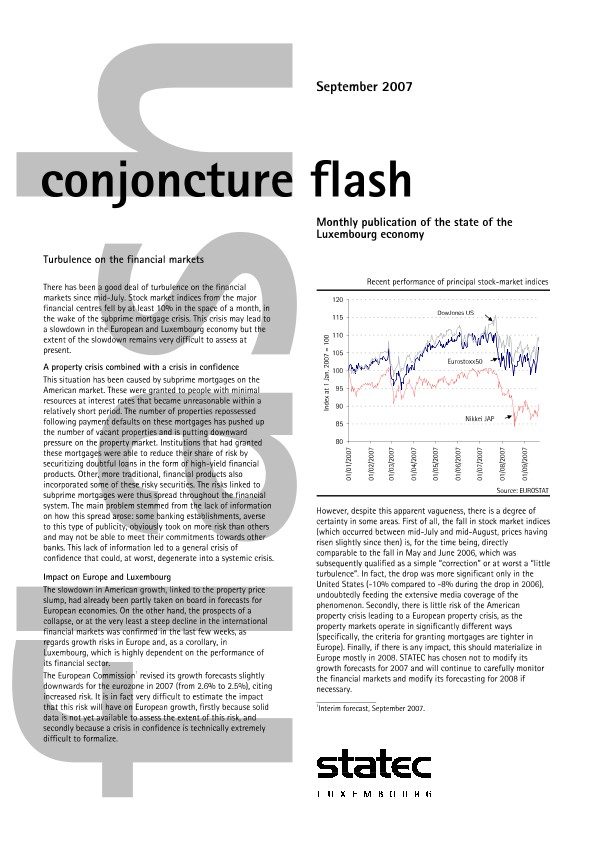

PDF Conjoncture Flash September 2007

Manufacturing: euphoria returns to earth

Construction: net rise in construction permits

Wholesale and retail trade: a difficult start to the year

Financial sector and other market services: UCIs: limited increase in July

Labour market: falling numbers of job seekers

Wage inflation: wages continue to rise

Foreign trade: oil prices at an all-time high but no shock in sight

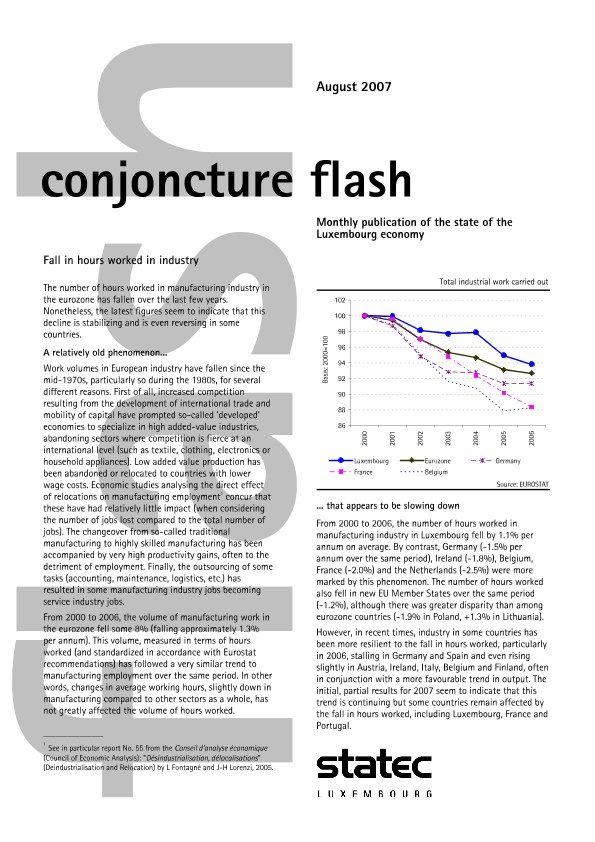

PDF Conjoncture Flash August 2007

Industry: rising prices, except in energy

Construction: construction prices boosted by metal prices

Wholesale and retail trade: a good start to 2007 for hotels

Financial sector and other market services: banking employment still growing, but less quickly

Labour market: labour market: +4,300 residents over one year

Wage inflation: underlying inflation slows down

Foreign trade: refocusing exports of goods on Europe

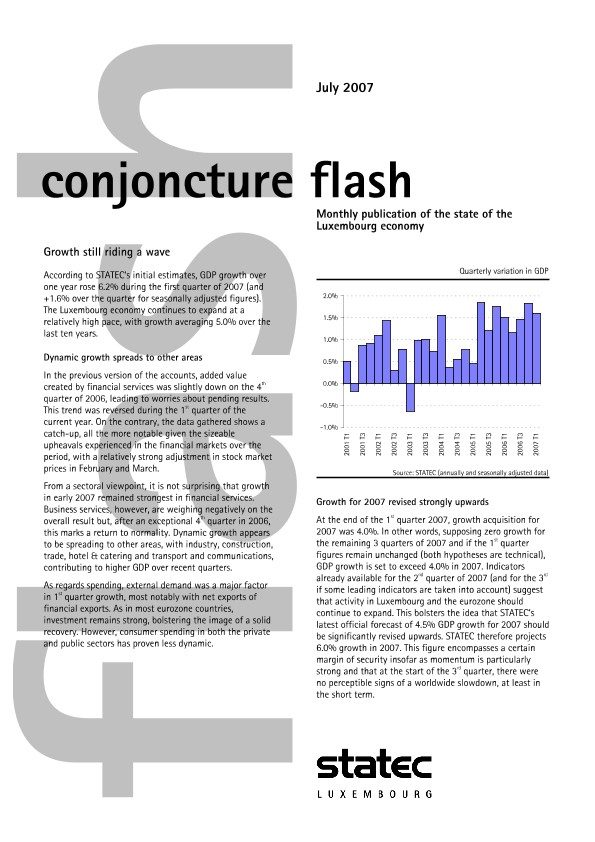

PDF Conjoncture Flash July 2007

Manufacturing: modest performance set to improve

Construction: an exceptional start to the year

Wholesale and retail trade: new car registrations stall

Financial sector and other market services: satisfactory first half for banks

Labour market: temporary work continues to accelerate

Inflation, wages: price hike in oil products

Current account surplus stabilises Foreign trade: current account surplus stabilises

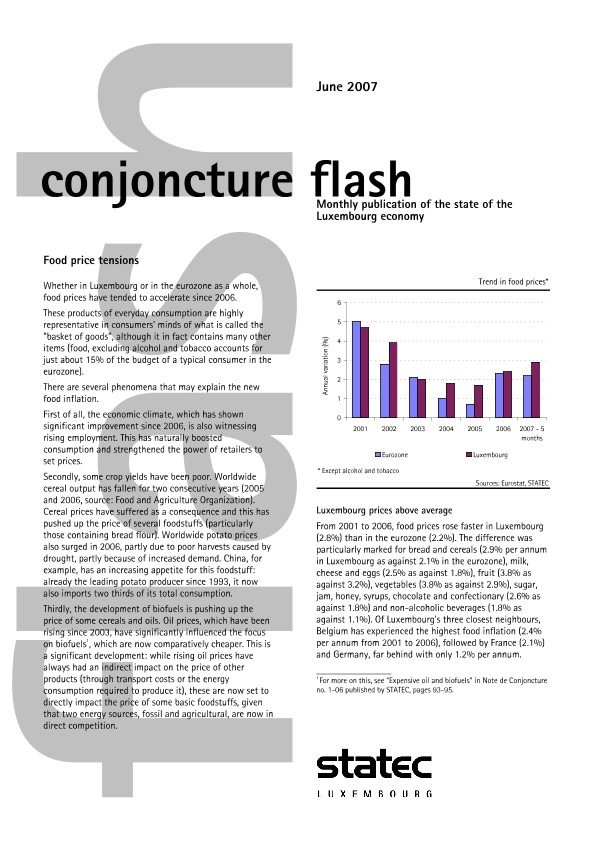

PDF Conjoncture Flash June 2007

Manufacturing: manufacturers confident

Construction: muted outlook

Financial sector: UCIs remain on course

Business trends: fewer bankruptcies

Labour market: fall in unemployment

Inflation - wages: higher wage growth

Foreign trade: mixed start to the year for trade in goods and services