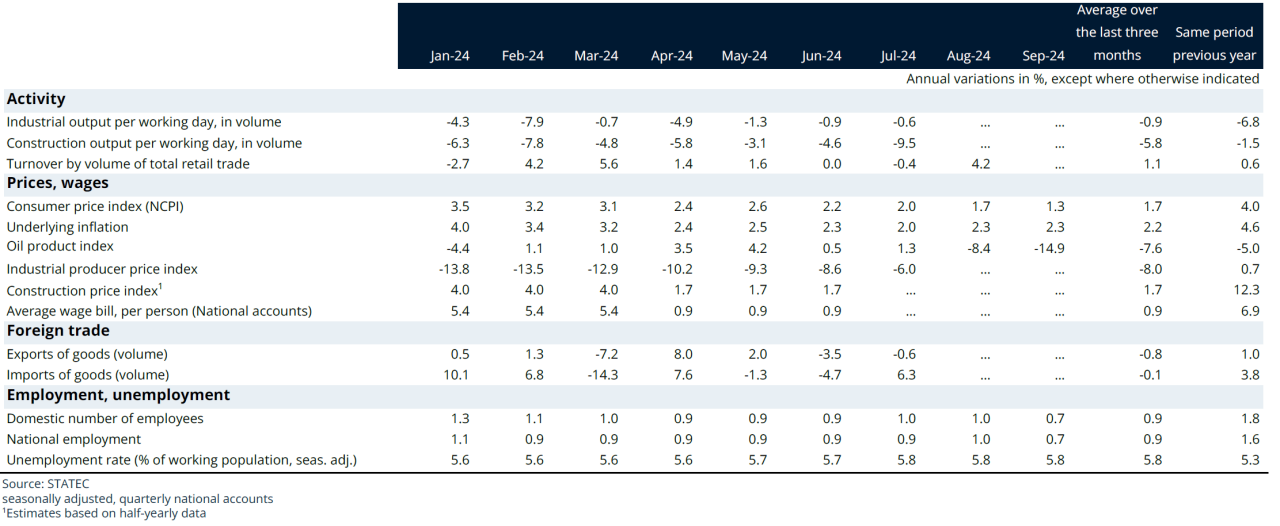

Conjoncture Flash October 2024: Construction remains in critical condition

The construction sector, which has already been struggling for some time, is showing little sign of recovery. Activity and employment are still falling, while business confidence has stabilised at a very low level. The property market is beginning to improve, but this will not have a significant impact on construction activity in the immediate future.

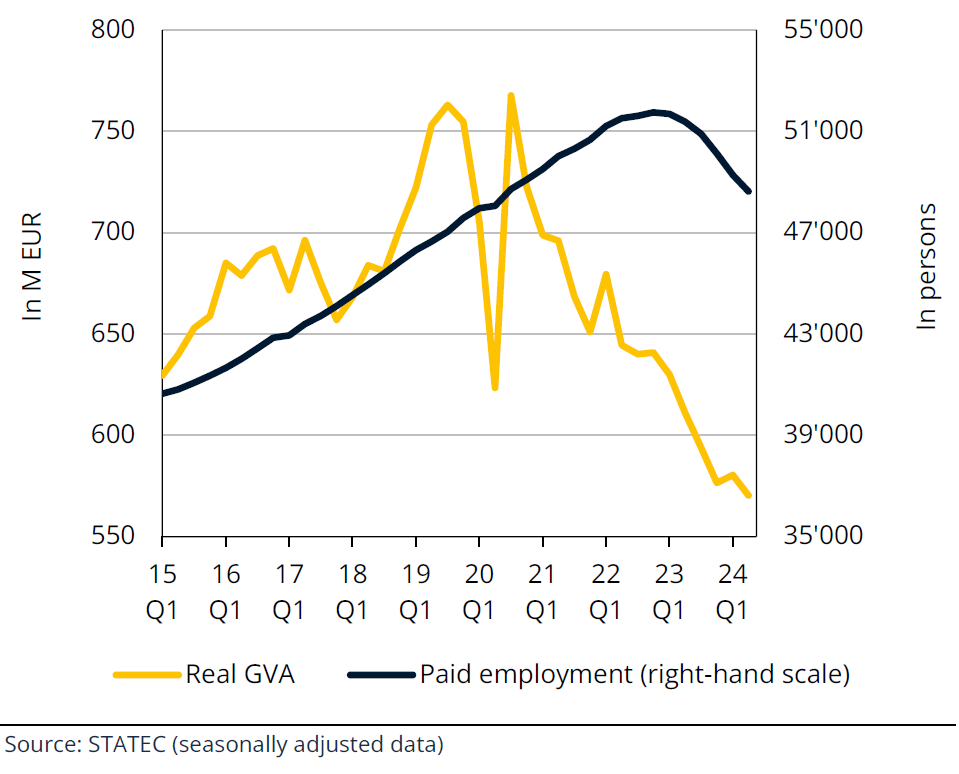

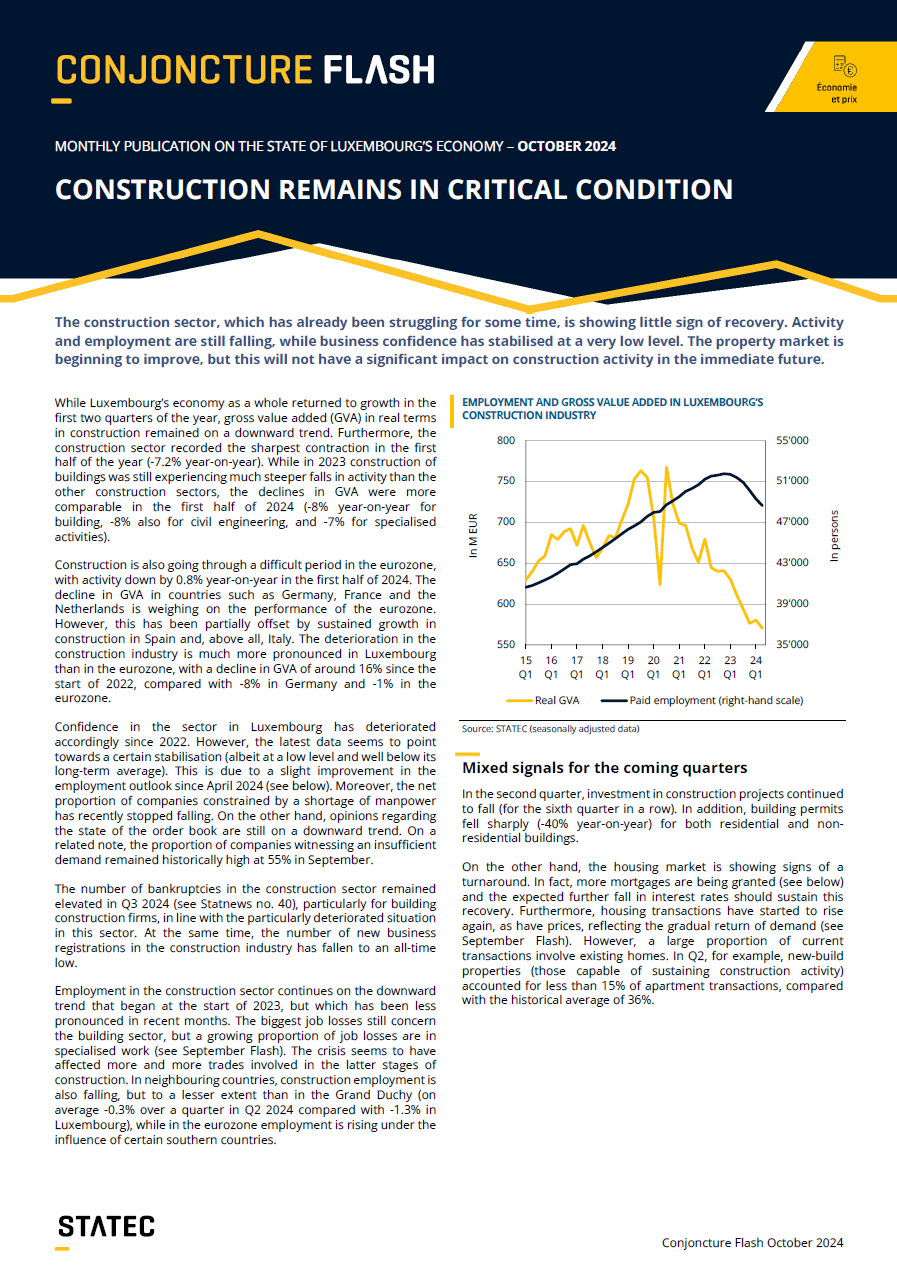

While Luxembourg’s economy as a whole returned to growth in the first two quarters of the year, gross value added (GVA) in real terms in construction remained on a downward trend. Furthermore, the construction sector recorded the sharpest contraction in the first half of the year (-7.2% year-on-year). While in 2023 construction of buildings was still experiencing much steeper falls in activity than the other construction sectors, the declines in GVA were more comparable in the first half of 2024 (-8% year-on-year for building, ‑8% also for civil engineering, and -7% for specialised activities).

Construction is also going through a difficult period in the eurozone, with activity down by 0.8% year-on-year in the first half of 2024. The decline in GVA in countries such as Germany, France and the Netherlands is weighing on the performance of the eurozone. However, this has been partially offset by sustained growth in construction in Spain and, above all, Italy. The deterioration in the construction industry is much more pronounced in Luxembourg than in the eurozone, with a decline in GVA of around 16% since the start of 2022, compared with ‑8% in Germany and -1% in the eurozone.

Confidence in the sector in Luxembourg has deteriorated accordingly since 2022. However, the latest data seems to point towards a certain stabilisation (albeit at a low level and well below its long-term average). This is due to a slight improvement in the employment outlook since April 2024 (see below). Moreover, the net proportion of companies constrained by a shortage of manpower has recently stopped falling. On the other hand, opinions regarding the state of the order book are still on a downward trend. On a related note, the proportion of companies witnessing an insufficient demand remained historically high at 55% in September.

The number of bankruptcies in the construction sector remained elevated in Q3 2024 (see Statnews no. 40), particularly for building construction firms, in line with the particularly deteriorated situation in this sector. At the same time, the number of new business registrations in the construction industry has fallen to an all-time low.

Employment in the construction sector continues on the downward trend that began at the start of 2023, but which has been less pronounced in recent months. The biggest job losses still concern the building sector, but a growing proportion of job losses are in specialised work (see September Flash). The crisis seems to have affected more and more trades involved in the latter stages of construction. In neighbouring countries, construction employment is also falling, but to a lesser extent than in the Grand Duchy (on average -0.3% over a quarter in Q2 2024 compared with -1.3% in Luxembourg), while in the eurozone employment is rising under the influence of certain southern countries.

Employment and gross value added in Luxembourg’s construction industry

Mixed signals for the coming quarters

In the second quarter, investment in construction projects continued to fall (for the sixth quarter in a row). In addition, building permits fell sharply (-40% year-on-year) for both residential and non-residential buildings.

On the other hand, the housing market is showing signs of a turnaround. In fact, more mortgages are being granted (see below) and the expected further fall in interest rates should sustain this recovery. Furthermore, housing transactions have started to rise again, as have prices, reflecting the gradual return of demand (see September Flash). However, a large proportion of current transactions involve existing homes. In Q2, for example, new-build properties (those capable of sustaining construction activity) accounted for less than 15% of apartment transactions, compared with the historical average of 36%.

International

Composite PMI of activity in China

Source: S&P Global (last point: Sept. 2024)

Massive stimulus package in China

Chinese GDP slowed significantly in Q2 (+0.7%, less than half the pace of the previous three quarters), and this downturn is likely to intensify in Q3. Since June, business surveys have been displaying a less favourable scenario, and September's results confirm the trend: the composite PMI index is back towards 50 points, indicating that activity is stagnating, and the index for industry is even in contractionary territory. This poor economic performance has prompted the Chinese authorities to introduce massive support measures since the end of September (some of which remain vague): lowering interest rates, recapitalising major state banks, providing financial support to local governments and easing restrictions on home ownership.

The package aims to revive the Chinese economy (Beijing has set a growth target of 5%), which is hampered by the crisis in its property sector and weak household demand (the two factors are linked, with Chinese households preoccupied as the vast majority have invested their savings in property), local authority debt and consumer prices that are flirting with deflation.

Activity

Consumer confidence indicator

Source: ECB (seasonally adjusted data)

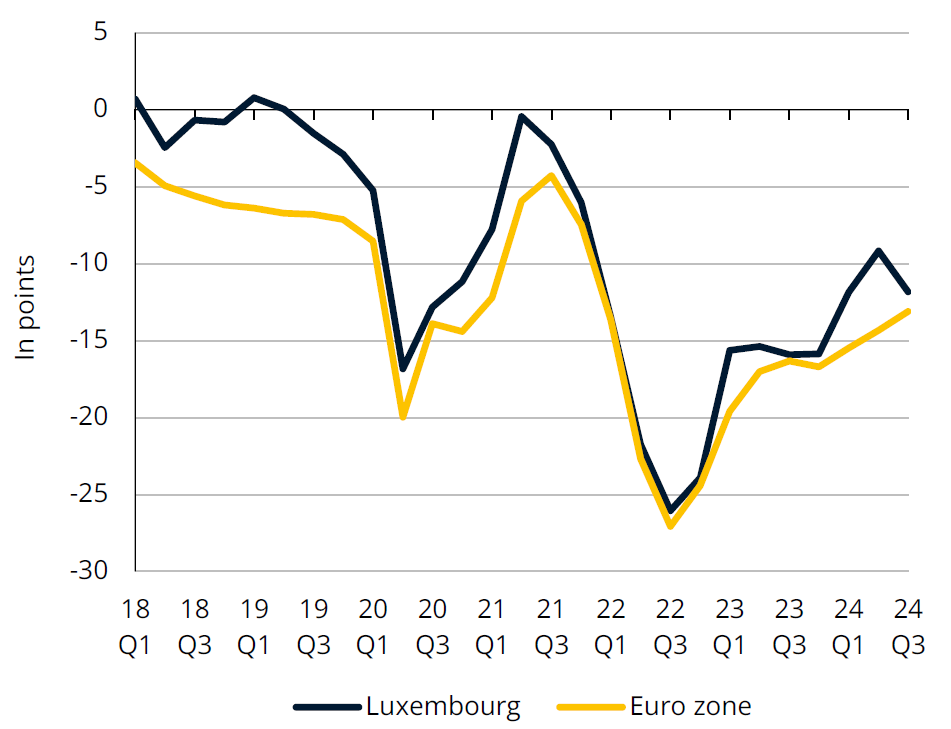

Consumer morale remains low

By the end of 2021, at the end of the health crisis, consumer confidence had more or less returned to its pre-pandemic level.

With Russia's invasion of Ukraine and the ensuing energy crisis - marked by soaring consumer prices - household morale has been affected in a much more pronounced and lasting manner. Although it has been trending upwards since the start of 2023, it is still a long way from reaching its pre-crisis levels.

As we approach 2025, consumers in Luxembourg and in the eurozone remain downbeat with regard to the general economic outlook, with sentiment much lower than before the war in Ukraine. For the other components of the confidence indicator (financial situation over the past year and over the next 12 months, purchase intentions of equipment goods), the catch-up has been clearer, but remains incomplete over the same period.

Financial sector

New loans granted by Luxembourg banks

Source: BCL (seasonally adjusted data, three-month centred moving average)

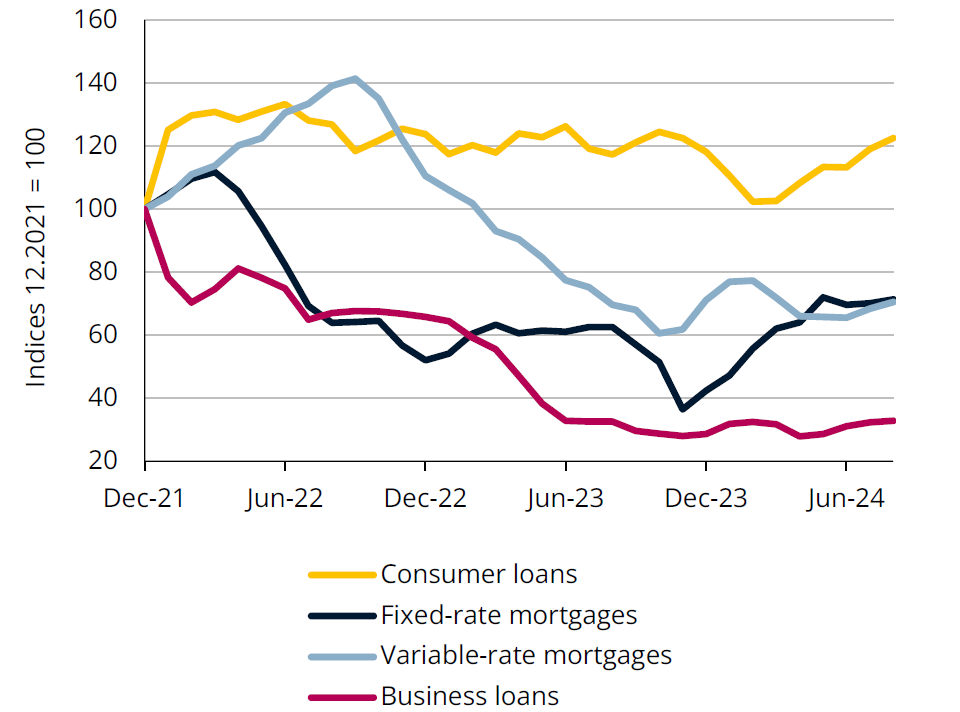

Household lending rising, businesses lending lagging

According to the bank lending survey, household demand for consumer and housing loans continued to rise in Q3 in Luxembourg and the eurozone, thanks to the improved outlook for the property market and the fall in interest rates. Demand for fixed-rate loans has been supported by the decline in associated rates since the beginning of 2024. Variable rates have only recently started to fall - with the first cut in key rates by the ECB in June - and are set to fall significantly following the two further cuts in key rates in September and October.

Demand for loans from companies is not yet picking up in Luxembourg and half the countries in the eurozone, due to the weakness of fixed investment (demand from companies is expected to pick up in Germany, Spain and France). Banks, for their part, continue to refuse certain loan applications from SMEs. New loans granted by Luxembourg banks to businesses fell by a further 3% year-on-year over the summer, reaching historically low levels.

Inflation and wages

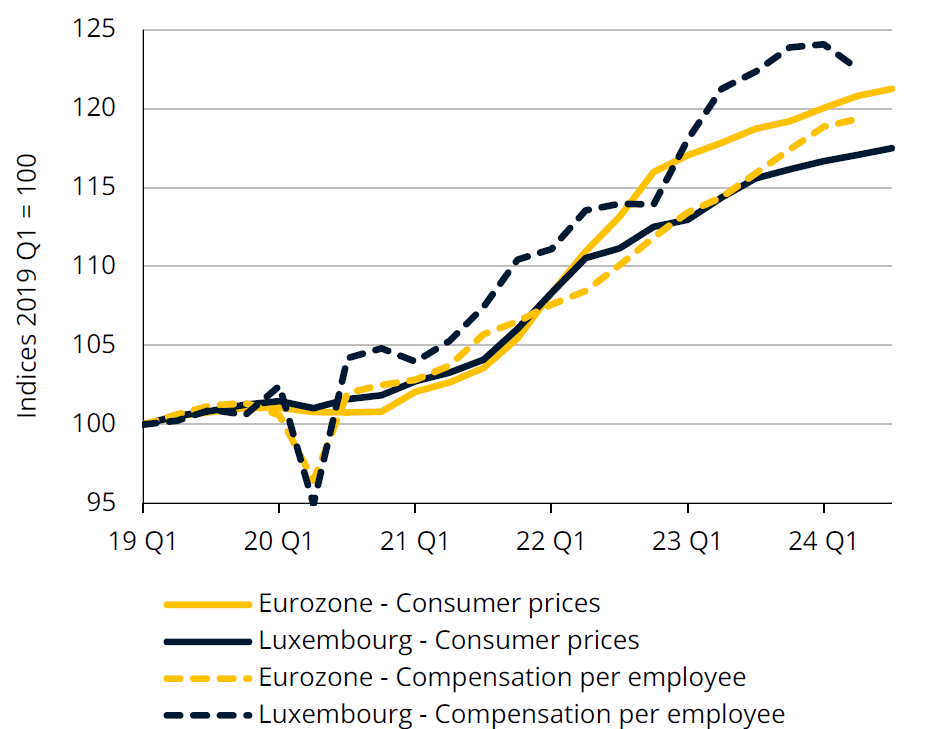

Consumer prices and wages

Sources: STATEC, Eurostat (seasonally adjusted data)

Gap between wages and consumer prices narrowing

In Luxembourg, wages (compensation per employee) have risen more sharply than prices since the health crisis in 2020. In 2022 and 2023, this gap widened further, following sustained wage growth in Luxembourg (+7.3% year-on-year in 2023), boosted by three successive indexations and slower price rises (+3.7% compared with +5.4% in the eurozone in 2023). The latter have been reduced by the fact that certain services are free. These developments have boosted consumer purchasing power. However, the gap has been narrowing since the start of 2024. According to an initial estimate, the compensation per employee fell by 1.3% over a quarter in Q2, after already slowing from +1.3% to +0.2% between Q4 2023 and Q1 2024 (a slowdown partly attributable to the compensation for the September 2023 index bracket which takes place from Q1).

In the eurozone, on the other hand, wages have shown little dynamism over this period compared to the surge in prices in 2022 and 2023, reflecting a fall in wage purchasing power across the monetary zone as a whole over this period. But here too the gap has narrowed considerably since 2024. In Luxembourg, as in Belgium, wage indexation has enabled wages to adjust much more quickly to the recent surge in prices than in the rest of the eurozone, where this adjustment is still ongoing.

Inflation

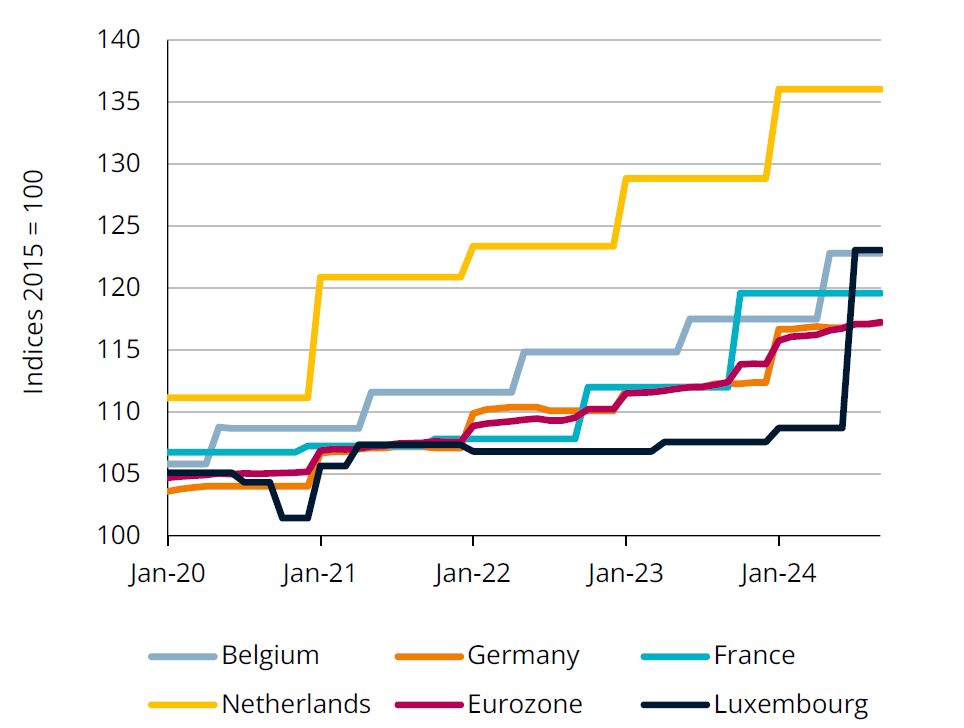

Prices for household waste collection

Source: Eurostat

Catch-up on prices for household waste collection

In July, prices for household waste collection rose sharply in Luxembourg's consumer price index (+13% over one month), largely as a result of the sharp rise in rates charged by the SIDEC inter-municipal association in the north of the country. This increase comes after several years of stable prices for this item of expenditure, during which neighbouring countries, and most other European countries, have continually increased their prices. Since January 2020 (and until September 2024), the cost of waste collection has risen by 12% in the eurozone, 12% in France, 13% in Germany, 16% in Belgium, 17% in Luxembourg (+3% only until June 2024) and 22% in the Netherlands.

Against this backdrop, it should also be noted that for other municipal tariffs, such as the price of water supply and the price of wastewater collection, price trends in Luxembourg remain relatively low at this stage compared with neighbouring countries and other countries in the eurozone (at around +8% between January 2020 and September 2024, compared with +15% over this period in the eurozone).

Labour market

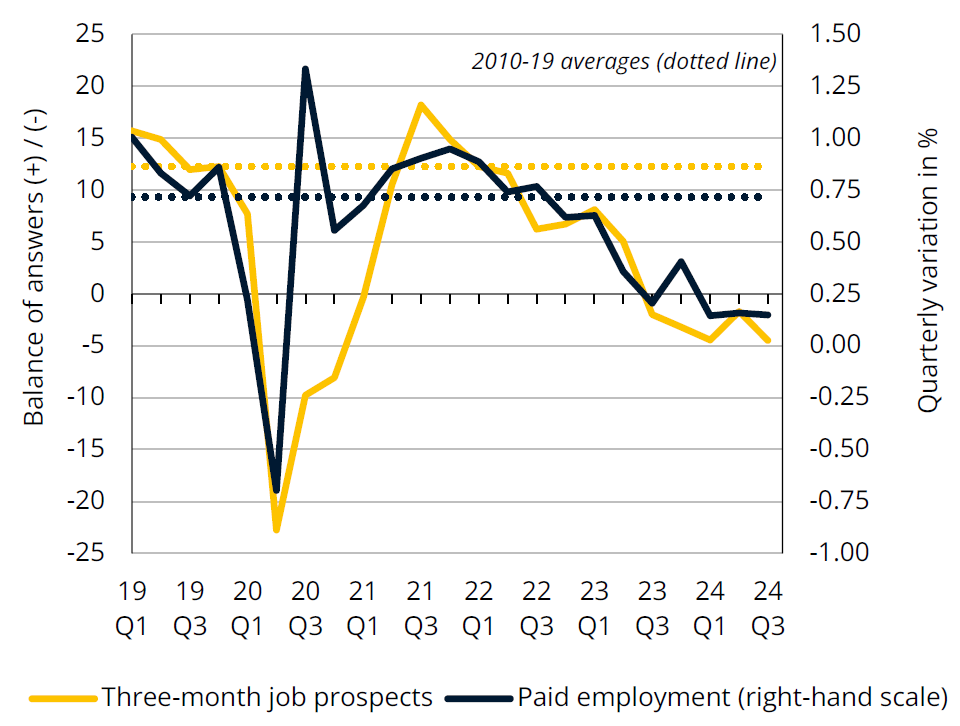

Employment prospects and paid employment in Luxembourg

Sources: IGSS, STATEC - business surveys (seasonally adjusted data)

Employment remains sluggish

The employment outlook (based on business surveys) does not point to any short-term upturn in employment. It improved slightly in Q2, but fell back again in Q3, in line with other economic signals. Economic activity picked up significantly in the first half of the year, but this trend has not yet been passed on to employment, which continues to grow at a historically low rate.

In Luxembourg, companies in the retail trade and in other non-financial services have revised their hiring intentions downwards for Q3, while the outlook for construction - which has been steadily deteriorating since 2022 - shows signs of a slight improvement. For industry, business expectations have recovered somewhat since the start of the year. Employment trends in industry and construction have weighed heavily on total employment in recent quarters, but preliminary data for Q3 suggest a less unfavourable outcome (in line with survey results for these two sectors).

Energy

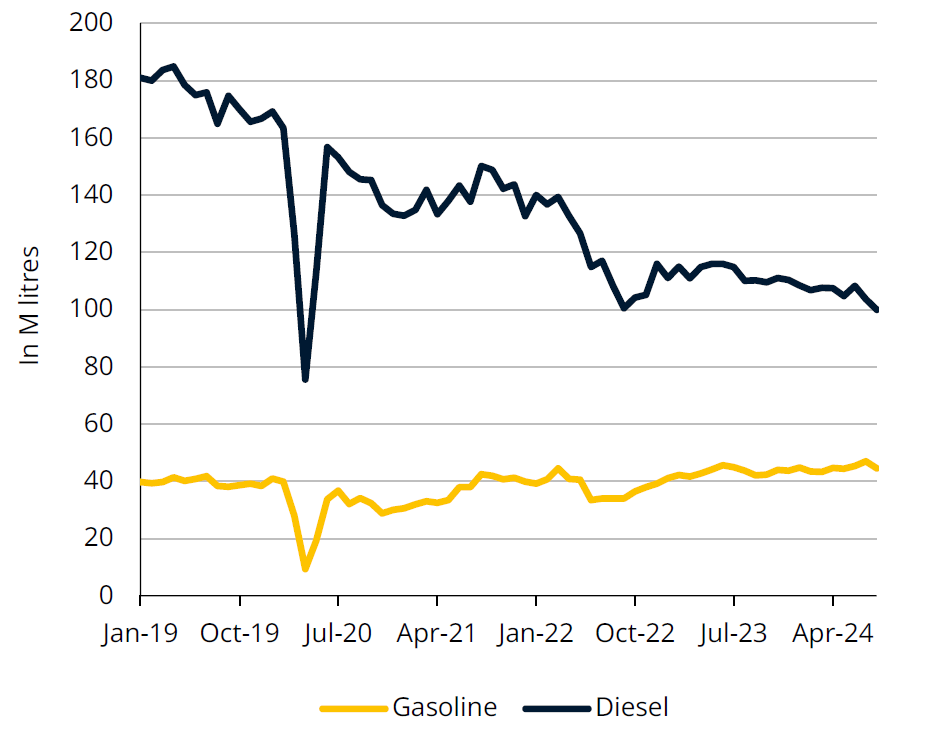

Fuel sales in Luxembourg

Sources: Ministry of Energy, STATEC (seasonally adjusted data)

Fewer sales at the pump

Fuel sales fell by 2% in 2023, a trend that is continuing in 2024. Over the first eight months of the year, sales fell 4% compared to the same period in 2023. This decline is attributable to diesel sales, which fell by 7%, while gasoline sales rose by 3%.

The fall in diesel sales can be explained by a less favourable price differential for diesel sold to professional customers, particularly in comparison to Belgium and France. This loss of competitiveness is due above all to the increase in the CO2 tax (from EUR 30 to 35/tCO2) at the start of 2024, making the professional price cheaper - compared with Luxembourg - by around 9 cents per litre in Belgium and 1 cent per litre in France.

In addition, the number of diesel cars registered in Luxembourg continues to fall, from around 185 000 at the end of 2023 to around 172 000 in September 2024. By contrast, the rise in gasoline sales seems to be underpinned by the continued influx of gasoline-electric hybrid cars (+6 600 over the same period) and a slight increase in cars running exclusively on gasoline (+1 300).

Dashboard

Indicators

Last update