Conjoncture Flash May 2025: Eurozone: Promising start of the year, but what next?

Economic growth in the eurozone strengthened slightly in Q1 2025, however there were marked differences between the major economies. Q2 business surveys point towards a loss of momentum in the services sector, which is also evident in Luxembourg.

Eurozone GDP rose 0.3% over one quarter in Q1 2025, following +0.2% increase in Q4 2025. Similar to previous quarters, Spain remains one of the most dynamic of the eurozone's leading economies, posting a 0.6% rise over the quarter. The activity was driven by all the components of domestic demand (private and public consumption and investment, with a contribution of 0.4 percentage points) as well as external demand (0.2 percentage points). Germany is gradually gaining momentum with a 0.4% increase in GDP, its best performance for over two years[1]. Foreign trade made a strong contribution, with a sharp recovery in the export of goods, particularly pharmaceuticals, cars, and trailers and semi-trailers – all important export categories for the US market. This trend could be linked to expectations of an increase in US tariffs[2] and may therefore only be temporary. However, German household consumption (+0.5%) was more dynamic than in previous quarters, as was investment (rising for the second consecutive quarter in both construction and machinery and equipment).

Italy also announced encouraging data with growth of 0.3% (the strongest for two years), driven notably by the performance of its agricultural and industrial sectors. France posted a moderate recovery, with +0.1% over the quarter (after a 0.1% fall in Q4, marked by the after-effects of the Olympic Games). This modest recovery is mainly the result of an increase in inventories, with the other components of demand reflecting a less buoyant climate: stagnation in household consumption, a fall in investment (-0.2%, after falling by 0.1% in the previous quarter) and a negative contribution from foreign trade (with exports down by 0.7%, compared with +0.2% in Q4 2024).

Slowdown in services activity on the horizon in the eurozone and Luxembourg?

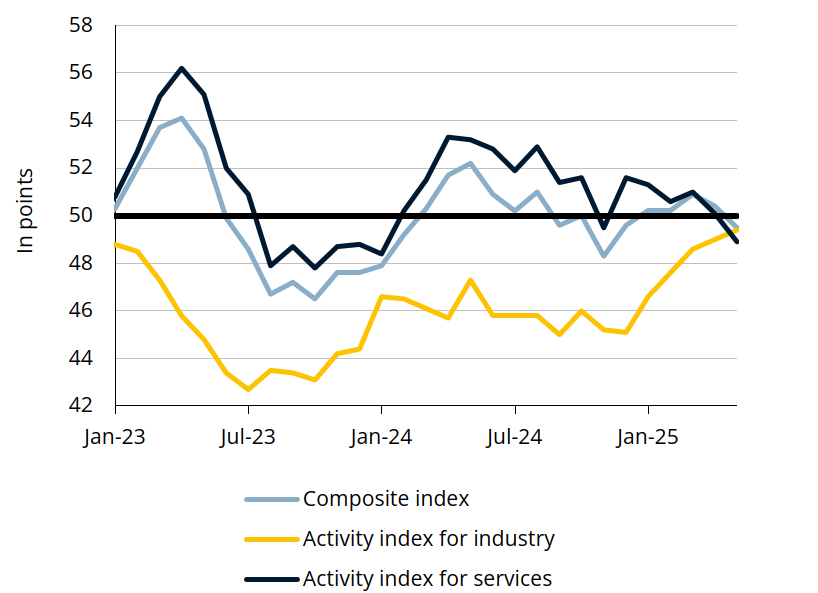

The outlook for Q2 looks less favourable. Business surveys indicate that service companies are feeling the pinch. The composite PMI activity index for the eurozone had already fallen in April and continued to decline in May, dropping below 50 points for the first time in five months, indicating a slight contraction in activity.

[1] Better than initially announced, as initial estimates put German growth at just 0.2% for Q1.

[2] https://www.destatis.de/EN/Press/2025/05/PE25_182_811.html

Indices PMI pour la zone euro

Sources: HCOB, S&P Global PMI

The downturn was driven by services activities, reflecting weakness in domestic demand. This loss of momentum in services is also being felt in Luxembourg, where confidence among those working in the sector fell slightly between February and April, although it remained stable in May. However, the outlook for business health and demand prospects is less favourable, particularly in business services[3].

On the other hand, manufacturers' opinions are improving The corresponding PMI activity index for the eurozone rose for the fifth consecutive month in May (industrial confidence in Luxembourg stabilised over this period). The press release accompanying the May results indicates that the entry into force of the new US tariffs - at a rate of "only" 10% for EU countries until 8 July - may have boosted industrial activity. It remains to be seen how events will unfold in this respect. Moreover, in yet another reversal of fortune, on 23 May, President Trump threatened to raise US tariffs on European products to 50% from 1 June, before delaying its implementation to 9 July two days later (to leave room for possible negotiations).

[3] This is particularly true of legal and accounting activities, head offices and management consultancy, rental services and tour operators.

Activity

Business surveys in the construction industry

Sources: European Commission, STATEC (seasonally adjusted data, provisional for May).

Note: The confidence indicator is the average of the balance of opinions on the state of the order book and the outlook for employment trends.

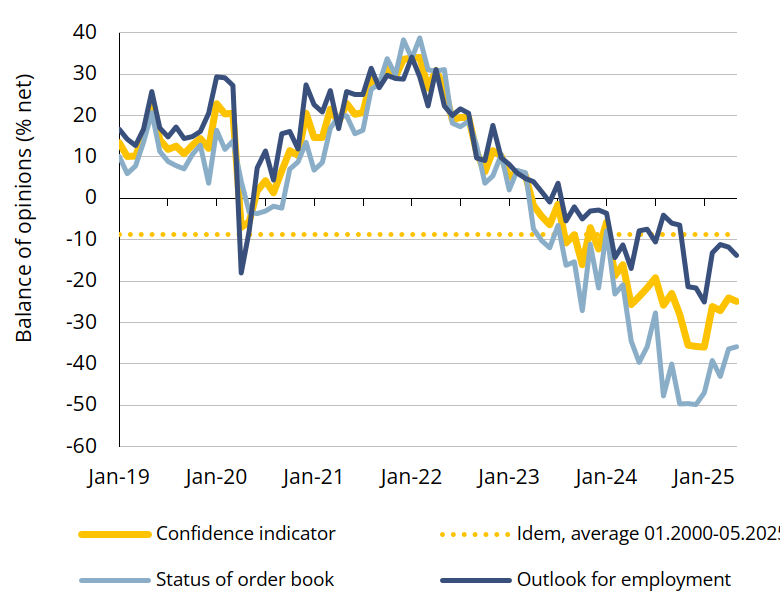

Tentative recovery in confidence in the construction industry

Confidence in the construction industry, which had been in freefall since the start of 2022, is beginning to show signs of improvement. Although it has risen slightly in recent months, it remains at a low level and well below its long-term average.

Since the start of the year, the proportion of companies rating their order backlog as insufficient has been falling, whereas it had been rising steadily until the end of 2024. In addition, assessments of recent activity seem to have stopped deteriorating (and even increased, according to provisional data for May), and the proportion of companies reporting insufficient demand has stopped rising (despite remaining at a very high level of around 60%). These positive trends relate more specifically to the building sector, and reflect the recent upturn in new housing transactions.

The outlook for employment reached a low point towards the end of 2024, but it has been improving slightly ever since. Furthermore, the proportion of companies citing a lack of manpower, which has been falling sharply since mid-2022, has recently stabilised. On the other hand, more and more companies say they are limited by financial constraints (over 20% at present).

Financial environment

Key rates forecasts

Source: IMF (April 2025 forecasts compared with dotted forecasts for October 2024)

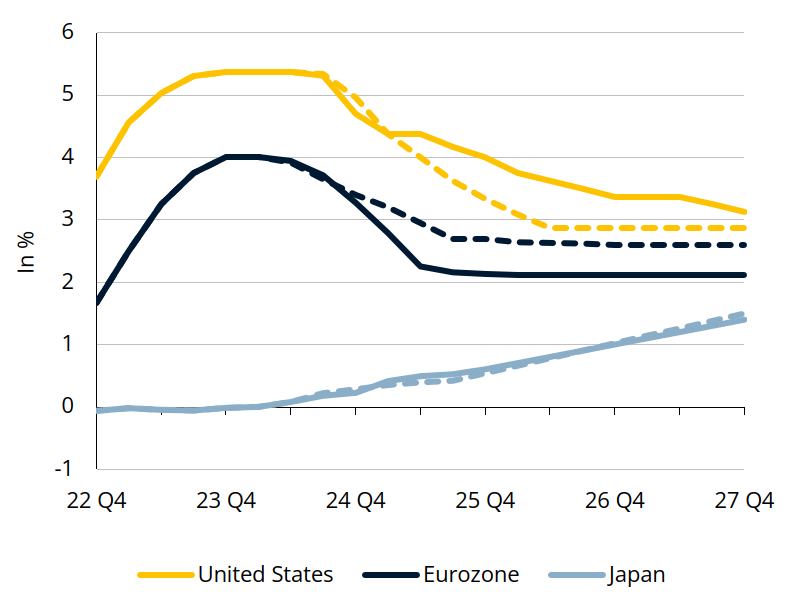

Relatively sharp and rapid fall in eurozone interest rates

Most of the major advanced economies have continued to cut the key interest rates in recent months. In the eurozone, there have been three cuts this year, and two further (of 25 basis points each) are expected in 2025 according to the IMF and the OECD, given the predominance of downside risks to the inflation and growth outlook. In the United States, the reduction is likely to be weaker than predicted in autumn 2024, with inflation forecast above its target level, regardless of the tariff scenario. A gradual easing is also planned over the next two years in Australia and the UK. In Canada, key rates are likely to be cut further, although the extent of the cuts is highly uncertain (and will depend very much on tariffs).

In Japan and Brazil, on the other hand, key rates may be raised gradually to ensure that inflation expectations remain well anchored.

Financial sector

Bank decisions on lending margins in Luxembourg

Source: BCE (enquête sur le crédit bancaire, moyennes mobiles sur 3 trimestres)

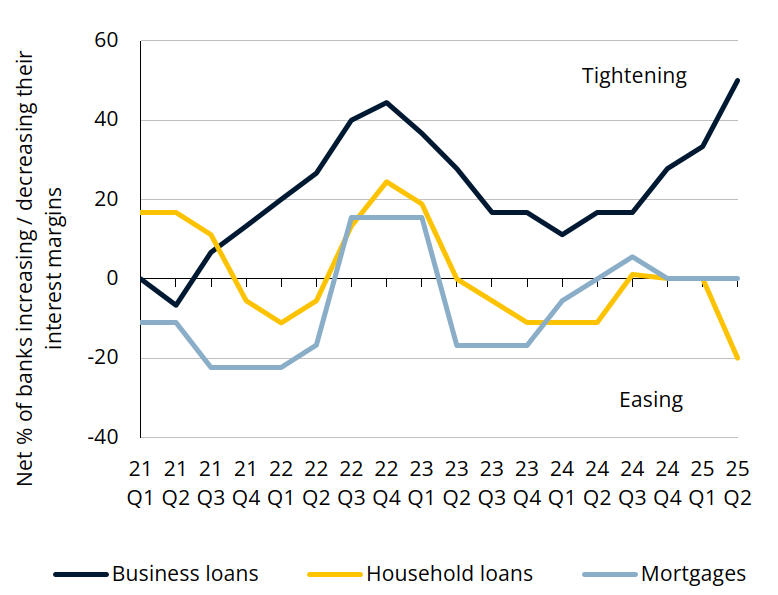

Household borrowing conditions ease

With key rates falling, borrowing costs continue to fall for businesses and households in Luxembourg. The interest rate reached in March 3.8% on variable-rate mortgages (-1.1 percentage points over one year), 4.0% on new consumer loans (-0.5 percentage points) and 3.1% on business loans (-0.5 percentage points). Fixed rates on new mortgages rose slightly in Q1 (+0.2 percentage points between December 2024 and March 2025, -0.2 percentage points over one year), driven by the rise in long-term rates in the eurozone.

In Q1 2025, banks in Luxembourg relaxed their general conditions on consumer credit, according to the bank credit survey. This easing was mainly due to lower interest rates and tighter lending margins. Conditions on home loans are unchanged, having been eased in the last quarter of 2024 via the duration of contracts. On the other hand, the criteria and conditions for granting loans to businesses have been tightened further (especially margins and non-interest charges) due to a worsening economic outlook and an increase in the risks relating to the collateral required and the costs associated with equity capital.

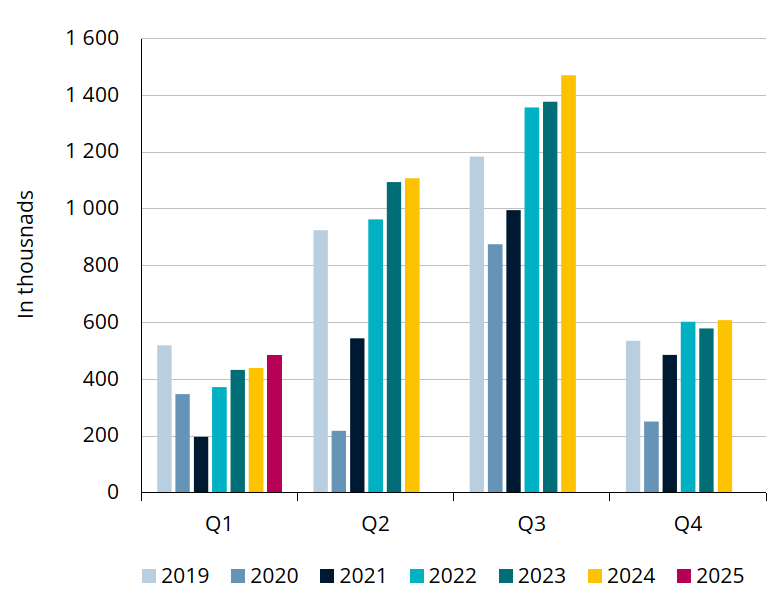

Tourism

Overnight stays in tourist accommodation

Source : STATEC

Tourism off to a good start

Luxembourg posted encouraging tourism data last year. The number of arrivals in accommodation establishments rose by almost 7%, compared with just 2% for the eurozone as a whole (although Spain, Portugal, Malta and France posted encouraging figures). Moreover, in 2024, the number of visitors to Luxembourg passed the 1.5 million for the first time.

Even if it is not the busiest period for welcoming tourists, Q1 2025 shows a continuation of this positive trend for establishments in the Grand Duchy, with an increase in arrivals of 7.3% year-on-year (compared with a fall of 0.3% in the eurozone over the same period). In terms of overnight stays, the rise was almost 10% over the same period, indicating a slight increase in the average length of stay.

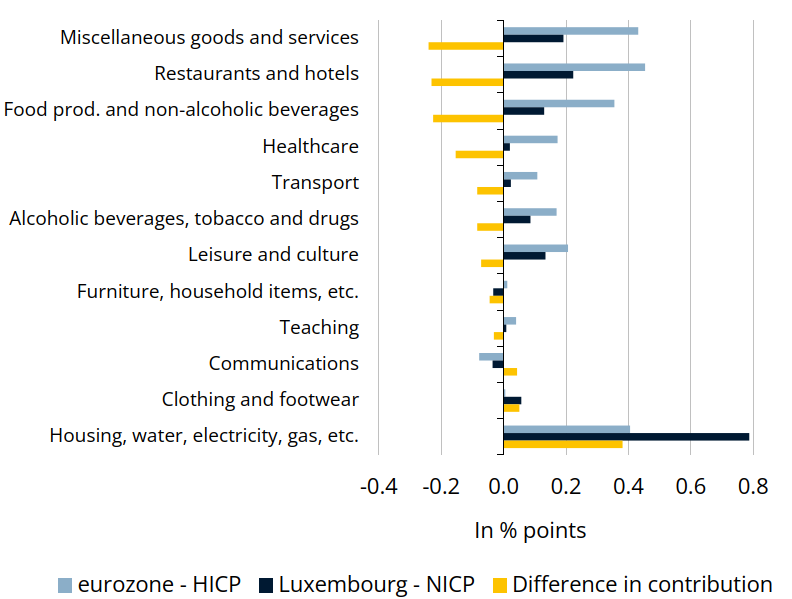

Inflation

Contributions to inflation in 2025, 4 months

Source : STATEC

Inflation in Luxembourg remains low compared with the eurozone

At the start of 2025, inflation in Luxembourg remains lower than the levels recorded in eurozone (1.7% compared with 2.3% over the first four months of the year), for 8 of the 12 categories of the consumer price index. The price of “miscellaneous goods and services”, restaurants and hotels, and food and non-alcoholic beverages have in fact progressed less in Luxembourg. Among the categories with the highest inflation in Luxembourg, “housing, water, electricity, gas and other fuels” stand out, mainly due to the rise in electricity prices in Luxembourg following the partial lifting of price caps, bringing then 0.4 percentage points to inflation.

Over the next few months, inflation in Luxembourg should pick up slightly as a result of the wage indexation in May 2025. In its latest forecasts, STATEC expects inflation to reach 1.9% in 2025 and 2026, relatively close to the European Commission's latest projection for the eurozone (2.1% in 2025 and 1.7% in 2026.

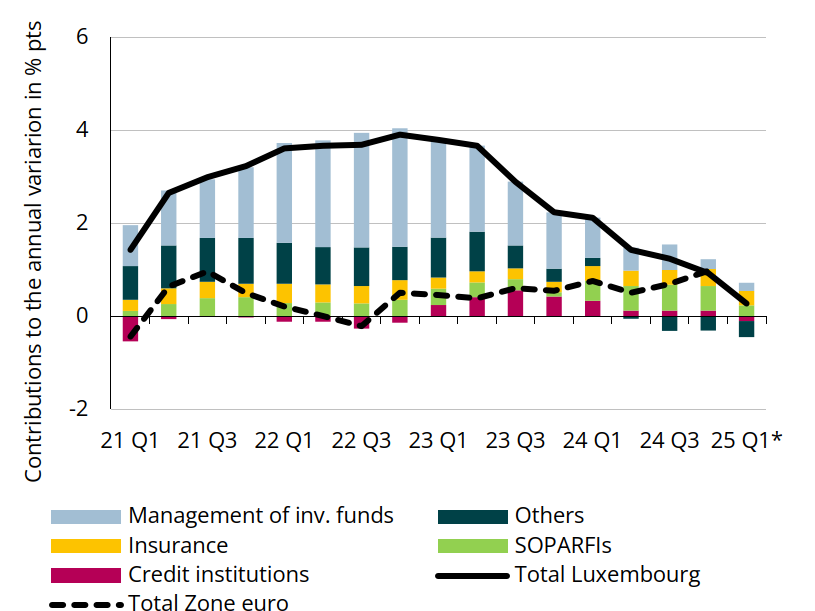

Labour market

Employment in the financial sector

Sources: IGSS, Eurostat

* January and February 2025

The financial sector no longer creates many jobs

Job creation has slowed markedly in the financial sector. In Q4 2024, annual growth fell to 0.9%, after posting close to +4% in the last quarter of 2022. Preliminary data for Q1 shows growth of 0.3%, the pace observed at the end of 2020, in the midst of the COVID crisis. Employment has slowed significantly, especially in investment fund and pension management (+0.2% year-on-year in Q4 2024 and Q1 2025, after rising +2.5% at the end of 2022). However, this sub-branch is still job creator at the beginning of 2025, along with financial holding companies (SOPARFIs) and insurance. On the other hand, employment fell slightly in credit institutions (-0.1% year-on-year) and, to a greater extent, in other sub-branches (mainly as a result of restructuring).

In the eurozone, where employment in this sector has grown at a much slower pace than in Luxembourg since 2021, job creation has picked up slightly, reaching +1.0% year-on-year in Q4 2024, after declining -0.2% in Q3 2022. The recovery towards the end of 2024 was mainly driven by Germany, Ireland and Spain. On the other hand, France, the Netherlands and the Grand Duchy are experiencing a slowdown.

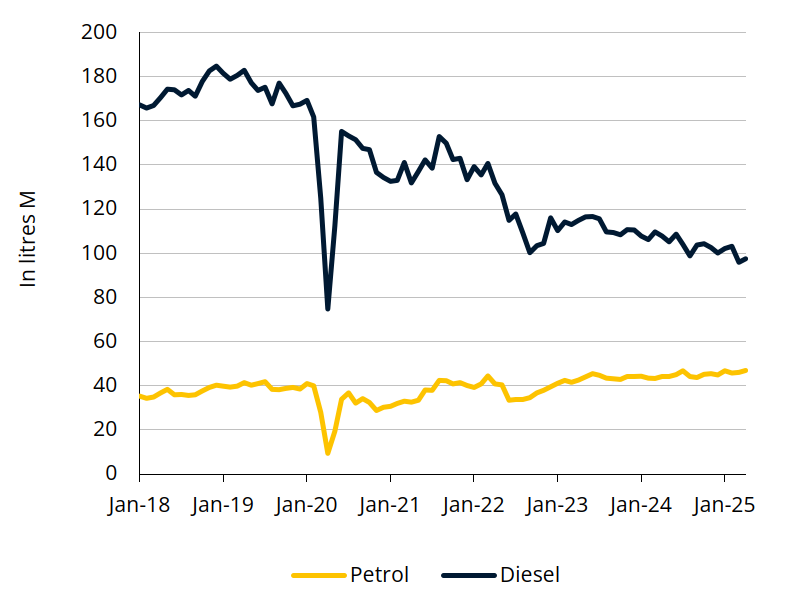

Energy

Fuel sales in Luxembourg

Sources : Ministère de l'Economie, STATEC (données désaisonnalisées)

Fuel sales continue to decline

Fuel sales in Luxembourg are continuing the downward trend that began in 2019. In the first four months of 2025, sales were down by almost 4% compared with the same period last year. This decline is attributable to diesel sales, which fell by more than 7% over the same period. On the one hand, the number of diesel-powered cars in Luxembourg is falling steadily (down by a third since 2019). On the other hand, the price differential with neighbouring countries has gradually narrowed over the last few years, in particular due to the continuous increase in CO2 tax in Luxembourg, which has moreover played a key role in achieving its climate objectives. For commercial diesel, the differential has even been reversed, with diesel now cheaper in Belgium and France than in Luxembourg.

However, petrol sales rose by 6% at the start of the year, even though the number of cars running exclusively on petrol in Luxembourg has stabilised. The increase is mainly due to the emergence of hybrid cars, most of which are equipped with petrol engines to complement their electric motor.

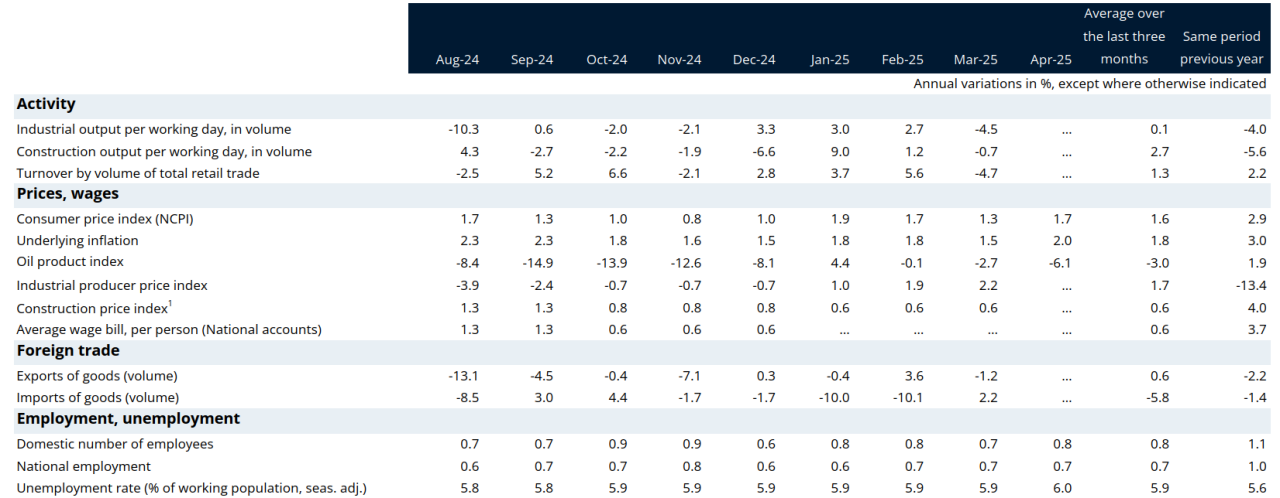

Dashboard

Source: STATEC

seasonally adjusted, quarterly national accounts

1 Estimates based on half-yearly data

Indicators

Dernière modification le