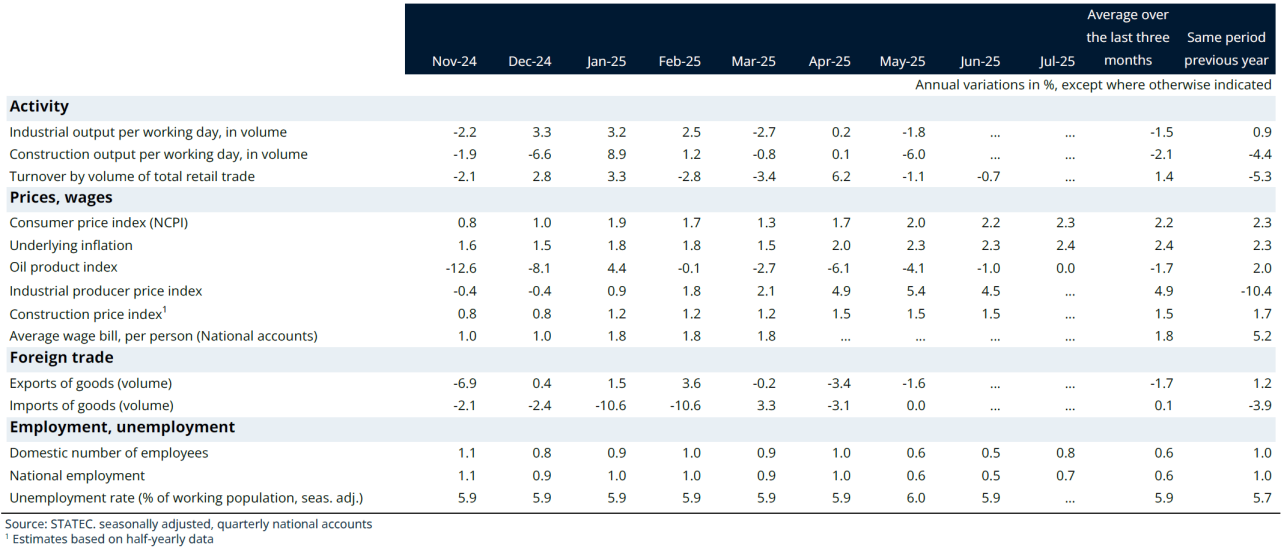

Conjoncture Flash August 2025: International environment in turmoil in the first semester

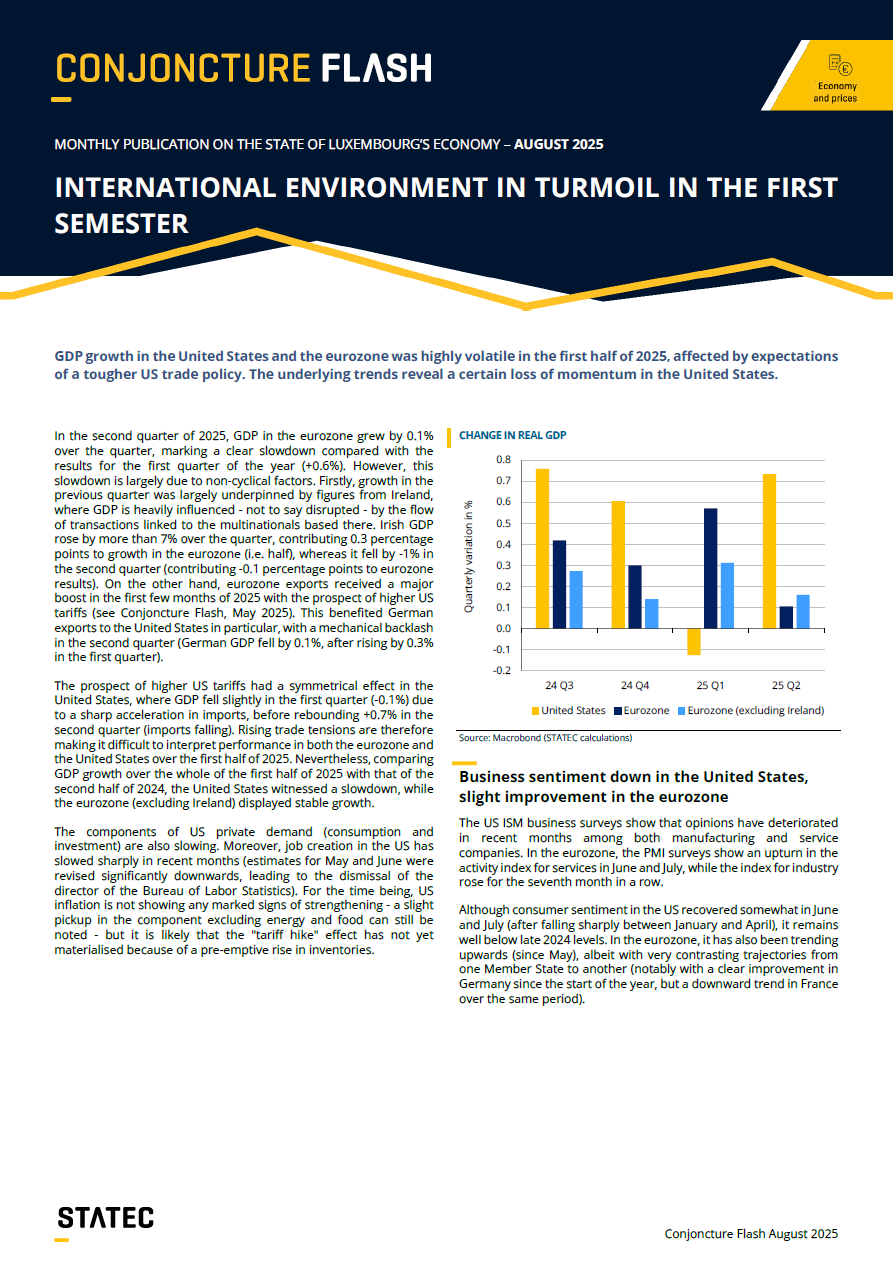

GDP growth in the United States and the eurozone was highly volatile in the first half of 2025, affected by expectations of a tougher US trade policy. The underlying trends reveal a certain loss of momentum in the United States.

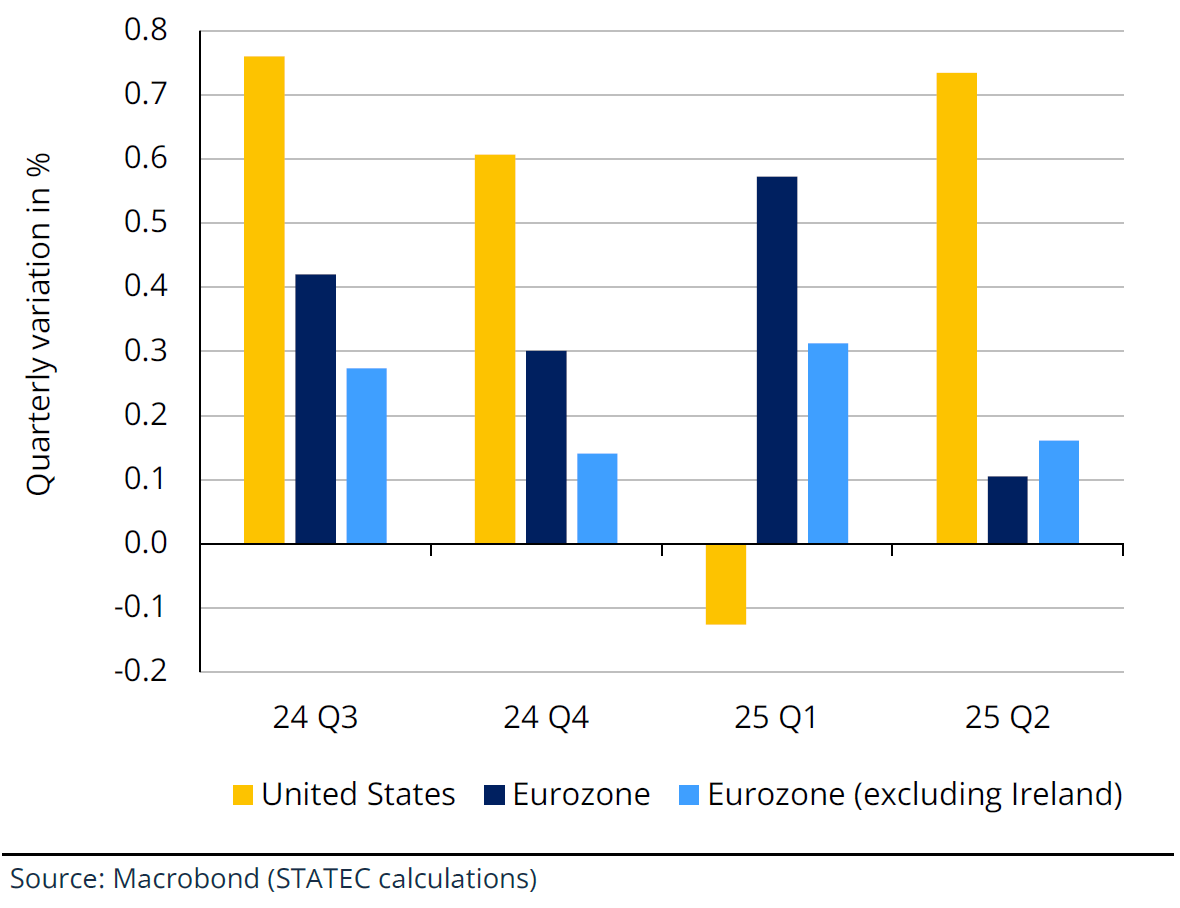

In the second quarter of 2025, GDP in the eurozone grew by 0.1% over the quarter, marking a clear slowdown compared with the results for the first quarter of the year (+0.6%). However, this slowdown is largely due to non-cyclical factors. Firstly, growth in the previous quarter was largely underpinned by figures from Ireland, where GDP is heavily influenced - not to say disrupted - by the flow of transactions linked to the multinationals based there. Irish GDP rose by more than 7% over the quarter, contributing 0.3 percentage points to growth in the eurozone (i.e. half), whereas it fell by -1% in the second quarter (contributing -0.1 percentage points to eurozone results). On the other hand, eurozone exports received a major boost in the first few months of 2025 with the prospect of higher US tariffs (see Conjoncture Flash, May 2025). This benefited German exports to the United States in particular, with a mechanical backlash in the second quarter (German GDP fell by 0.1%, after rising by 0.3% in the first quarter).

The prospect of higher US tariffs had a symmetrical effect in the United States, where GDP fell slightly in the first quarter (-0.1%) due to a sharp acceleration in imports, before rebounding +0.7% in the second quarter (imports falling). Rising trade tensions are therefore making it difficult to interpret performance in both the eurozone and the United States over the first half of 2025. Nevertheless, comparing GDP growth over the whole of the first half of 2025 with that of the second half of 2024, the United States witnessed a slowdown, while the eurozone (excluding Ireland) displayed stable growth.

The components of US private demand (consumption and investment) are also slowing. Moreover, job creation in the US has slowed sharply in recent months (estimates for May and June were revised significantly downwards, leading to the dismissal of the director of the Bureau of Labor Statistics). For the time being, US inflation is not showing any marked signs of strengthening - a slight pickup in the component excluding energy and food can still be noted - but it is likely that the "tariff hike" effect has not yet materialised because of a pre-emptive rise in inventories.

Change in real GDP

Business sentiment down in the United States, slight improvement in the eurozone

The US ISM business surveys show that opinions have deteriorated in recent months among both manufacturing and service companies. In the eurozone, the PMI surveys show an upturn in the activity index for services in June and July, while the index for industry rose for the seventh month in a row.

Although consumer sentiment in the US recovered somewhat in June and July (after falling sharply between January and April), it remains well below late 2024 levels. In the eurozone, it has also been trending upwards (since May), albeit with very contrasting trajectories from one Member State to another (notably with a clear improvement in Germany since the start of the year, but a downward trend in France over the same period).

Consumption

New registrations of private cars

Sources: ACEA, SNCA, STATEC (seasonally adjusted data)

Environment remains difficult for vehicle sales

In the first half of 2025, new car sales in the eurozone were down by around 2.5% on the previous year. This trend has affected most Member States, particularly those bordering Luxembourg (-5% in Germany, -8% in France and -11% in Belgium). In Spain, on the other hand, registrations rose by 14% over the same period, reflecting the dynamism of the Spanish economy. Luxembourg also displayed an increase, although much more modest (+1%), following a lacklustre year in 2024 (-5%, while the eurozone stagnated). In the Grand Duchy, as in the eurozone as a whole, new car registrations are still lower than pre-pandemic (down by around 15% and 20% respectively).

For commercial vehicles (vans, trucks and buses), the trend is also downwards in the eurozone (around -15% year-on-year in the first semester). Luxembourg's result was better (up by around 6% over the same period), but again after a year in 2024 well below the performance in Europe.

Financial environment

Interest rates on mortgages in Luxembourg

Sources: BCL, BCE (seasonally adjusted data)

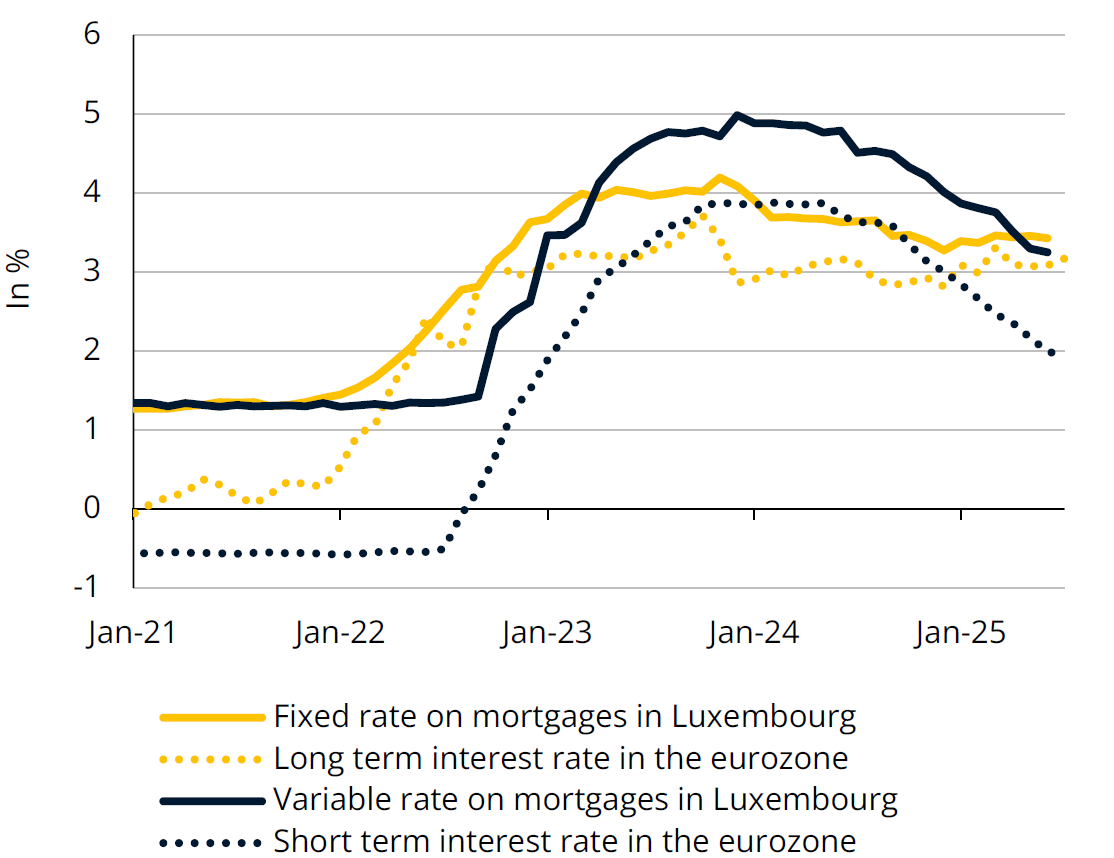

Variable-rate loans are becoming attractive again

Mortgages granted by banks in Luxembourg rebounded strongly in the second quarter (+33% year-on-year, +30% quarter-on-quarter). They were bolstered by interest rate cuts, the easing of lending criteria and state subsidies (some of which expired at the end of June). The rebound concerned all types of property (flats and houses), buyers (developers and private individuals) and credit contracts (fixed or variable rate).

After trending downward over the last three years, variable-rate loans jumped by almost 50% between the first and second quarters (+25% for fixed-rate loans). In June, variable-rate loans accounted for 44% of new loans granted, compared with 34% in late 2024. The average variable interest rate has been slightly below the fixed rate since May and should continue to fall as key rates are cut. Fixed rates - which depend on long-term rates in the eurozone - should stabilise at around 3.4%. According to the bank lending survey, banks do not intend to change their lending criteria in the third quarter, but they anticipate a fall in demand for home loans.

Financial sector

Composition of green investment funds in Luxembourg

Source: CSSF (Articles 8 and 9 of the SFDR – Sustainable Finance Disclosure Regulation)

Note: Fund units can be listed in several categories.

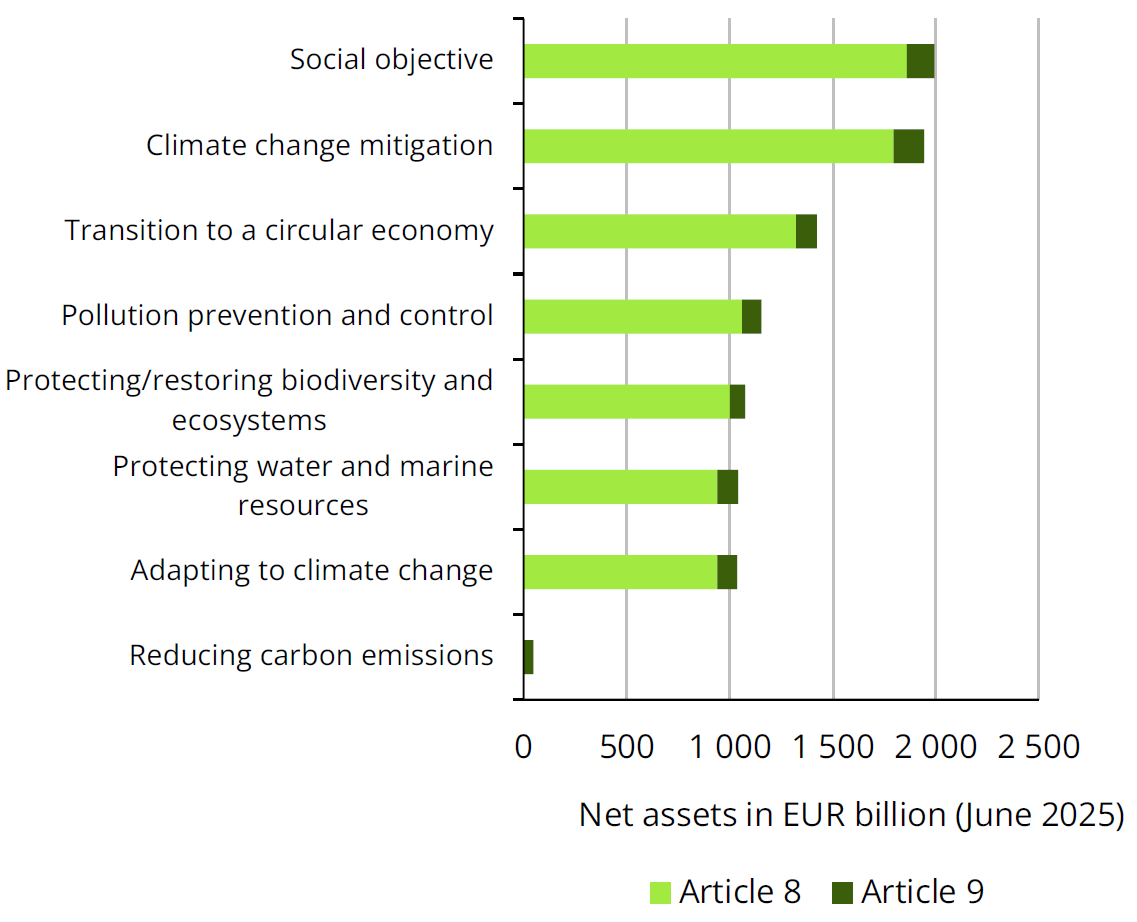

Relatively large "green" funds in Luxembourg

Since the European SFDR Regulation came into force in March 2021, asset managers have been required to provide information on the sustainability risks and impact of their investment products sold in the EU. Funds stating that they take environmental and/or social characteristics into account (Article 8 funds, known as “light green” funds) accounted for 61% of the assets of undertakings for collective investment in Luxembourg in June 2025. Funds with a sustainable investment objective ("dark green” Article 9 funds) accounted for 3%. According to EFAMA, Luxembourg is home to 35% of the assets of Article 8 European funds and 54% of Article 9 funds.

More than half of the green funds in Luxembourg declare a social objective and/or include climate change mitigation in their selection criteria. According to Morningstar, Article 8 European equity funds have seen their exposure to defence companies quadruple since the start of the war in Ukraine in 2022 (accounting for 2.5% of assets). EU Article 8 funds recorded a total of EUR 43 billion in new capital in Q2 (35% of overall EU fund flows), while Article 9 funds, which have an explicit sustainability objective, continued to record capital outflows for the seventh consecutive quarter.

Activity

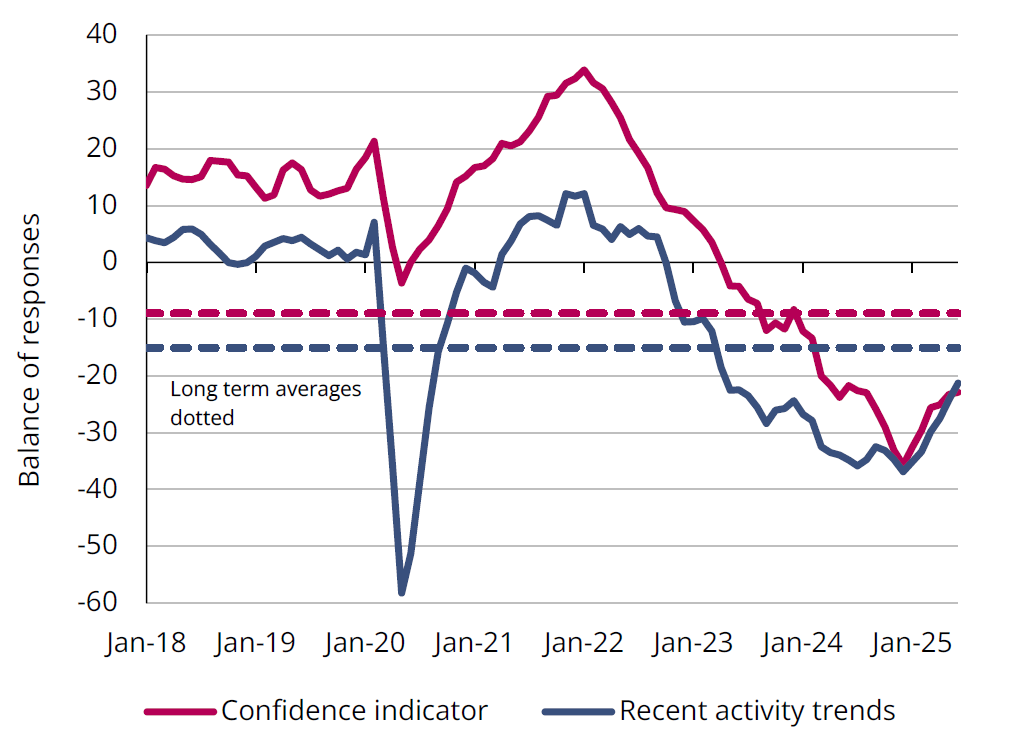

Business surveys in the construction sector

Sources: European Commission, STATEC (seasonally adjusted data, smoothed over 3 months).

Slight rise in morale in the construction sector

Confidence in the construction sector continues to improve slowly but remains below its long-term average. The building sector, in particular, has seen clear progress since the start of the year, while there has been a stagnation for specialized construction activities.

The order books of businesses are recovering (despite dipping slightly in June-July) and the duration of assured activity increased over the first half of the year. In addition, business surveys show an improvement in recent construction activity since the start of the year. This change is mainly due to the fact that fewer companies are reporting a decline in activity (most are instead reporting that the situation has stabilised).

Lack of demand remains a major constraint, despite a slight improvement in recent months (it was cited by 57% of companies in July, after peaking at 66% in February). The outlook for employment in this sector is also tending to improve (see below).

Labour market

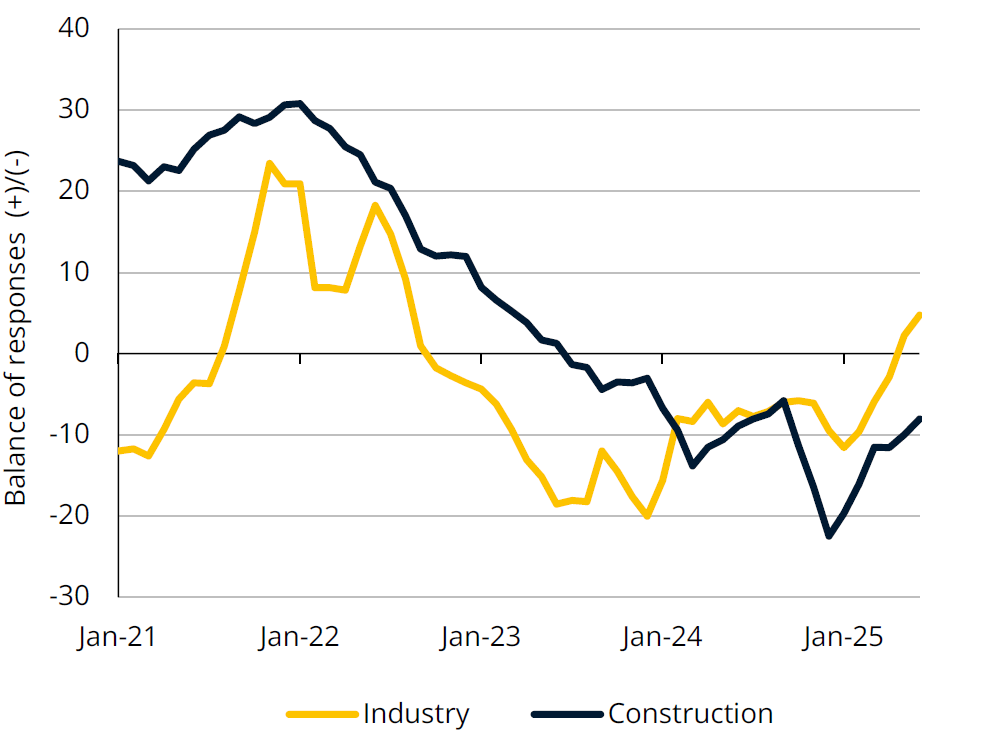

Employment expectations in 3 months (business surveys)

Sources: European Commission, STATEC (seasonally adjusted data, smoothed over 3 months)

Improving employment prospects

Although employment prospects in industry and construction have recovered in Luxembourg since early 2025, they remain below their long-term average. In the eurozone, hiring prospects have also improved in the construction sector in recent months, while they have stabilised at extremely low levels in manufacturing. In Luxembourg, this improvement can also be seen in industrial employment, which rose by 0.1% over a quarter in Q2 2025, after ‑0.1% in Q1. Employment is still falling in construction (-0.6% over the quarter) but less sharply than in previous quarters.

Over the first 5 months of 2025, the agri-food industry contributed the most to the positive trend in industrial employment (+126 people compared to December 2024), followed by metallurgy, wood products and energy production and distribution (+35 people each). The manufacture of metal products and the manufacture of machinery and equipment, on the other hand, posted significant job losses over this period (-219 and -63 people respectively). In construction, employment remained relatively stable in civil engineering, while it continued to fall in specialised construction activities (-314) and building construction (-268).

Inflation

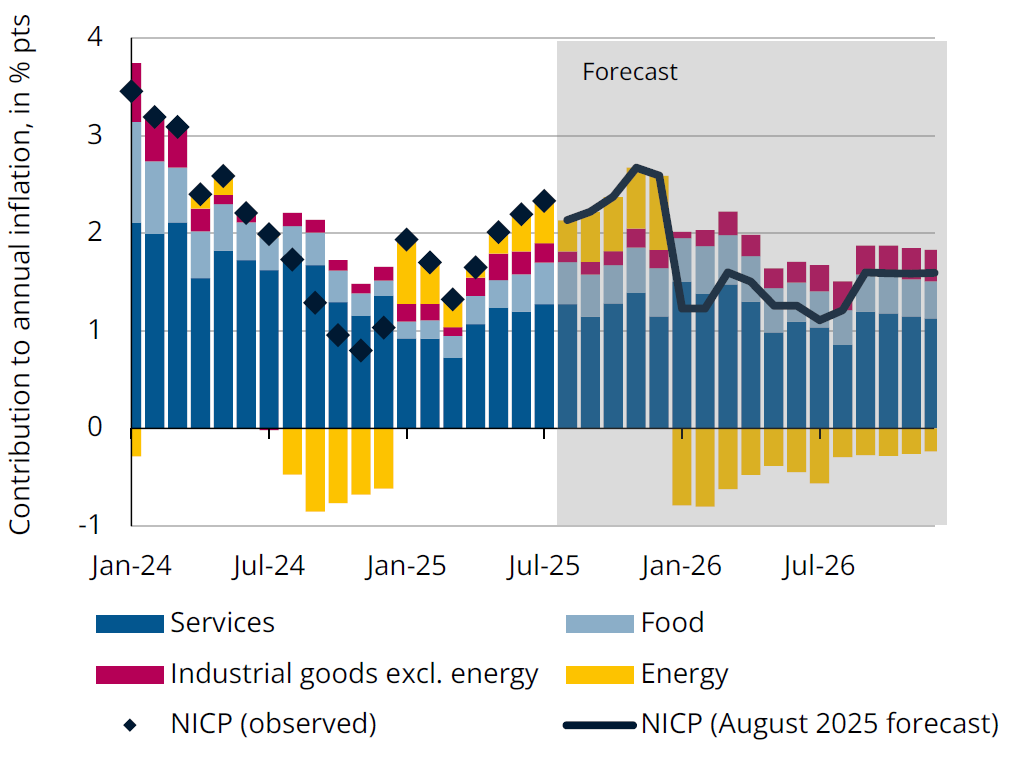

Annual inflation rate and contributions

Source: STATEC (forecasts dated 06/08/2025)

Inflation set to fall below the 2% target in Luxembourg in 2026

The recent automatic wage indexation has contributed to an increase in the price of services. Inflation is set to rise further over the coming months, reflecting the strengthening of positive base effects on energy towards the end of the year. Higher than expected inflation in Q2 2025 has led STATEC to raise its inflation forecast to 2.1% for this year (from 1.9% previously).

For 2026, an expected fall in oil prices, together with government measures on electricity prices (corresponding to a 9% fall over 2026 as a whole), should bring energy prices down by almost 7% in 2026, contributing to bring general inflation down to 1.4%. Inflation in services is set to be 2.3% in 2025 and 2.5% in 2026, while food inflation is set to be 2.0% in 2025 before rising to 2.3% in 2026. According to these forecasts, the next wage indexation is scheduled for the third quarter of 2026. The trade agreement announced on 27 July between the EU and the United States should set a single overall maximum rate of 15% for customs duties levied by the United States on goods originating in the EU. As the EU has refrained from similar retaliatory measures, most of the uncertainty surrounding additional inflation that the escalating tariffs could have triggered has dissipated.

Energy

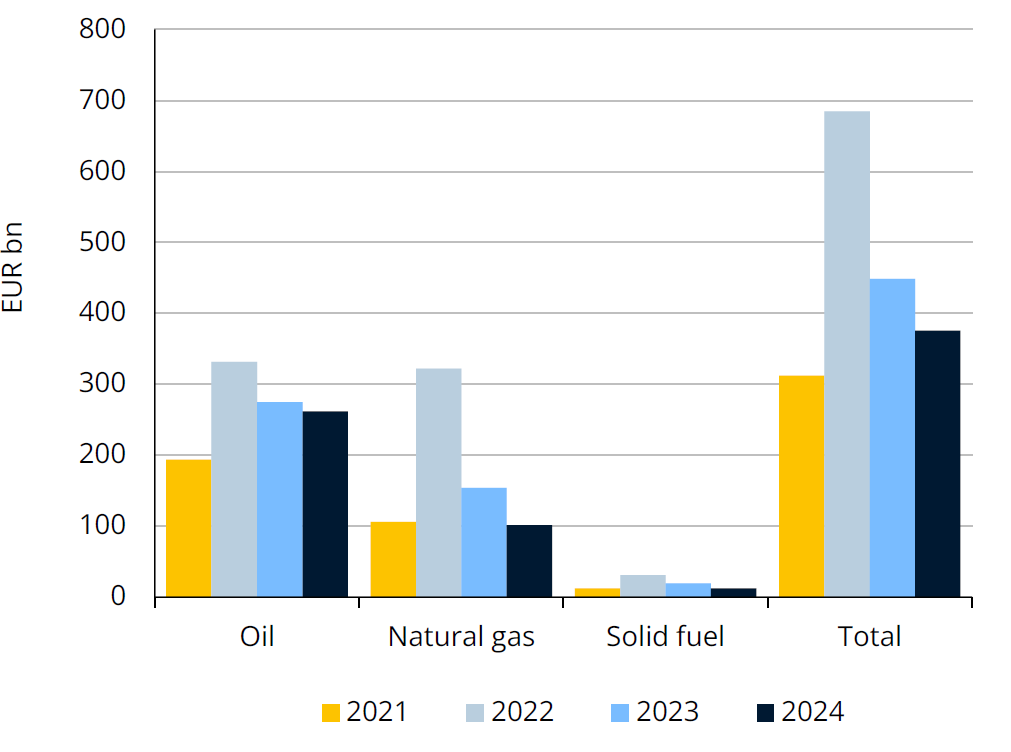

European union energy imports

Source: Eurostat

USD 250 billion in American energy for Europe?

As part of the trade agreement between the US and the EU, Europe has announced its intention to import USD 250 billion (approx. EUR 215 billion) of US energy every year up to 2028. This represents more than a tripling of US energy imports compared to 2024 (EUR 65 billion) and more than half of all energy imports into Europe (EUR 375 billion in 2024).

These targets will thus be difficult to achieve, even though US liquefied natural gas (LNG) imports jumped by 60% in the first half of 2025, after reaching almost EUR 20 billion in 2024. These could grow further, with the Americans planning to almost double their export capacity between 2024 and 2028. And Europe has the capacity to handle more LNG, for example to replace the remaining Russian gas. On the other hand, with the ramp-up in US production set to slow due to the expected weakness in oil prices, increases in oil imports (EUR 42 billion imported from the US in 2024) are likely to be limited.

Finally, it is not the EU as such that imports energy but its companies – and these cannot be forced to favour American supplies.

Dashboard

Indicators

Dernière modification le