Conjoncture Flash October 2025: How have exports of goods to the United States developed?

The volume of exports of goods from Luxembourg to the United States has fallen slightly this year, particularly in the case of metals and related products, however in a less pronounced way than on a European level. On the other hand, the value of these exports has increased and the United States' share of Luxembourg exports remains stable.

Following the agreement reached on 27 July, customs duties applied by the United States on imports from the European Union have been 15% on most goods since 7 August (rather than the 20% announced on 2 April to mark ‘Liberation Day’). Steel and aluminium products are a notable exception: they had already been subject to customs duties of 25% since 11 February, a rate which the United States raised to 50% on 4 June[1]. This is not insignificant from Luxembourg's perspective, as even though its exports of goods to the United States account for only 3% of the total, they consist primarily of metals and metal products (accounting for just over 40% of the total in recent years[2]).

Over the first 8 months of 2025, the volume of exports of goods from Luxembourg to Uncle Sam's country fell by 2%. For metals and related products, the fall was around 5% over the same period, albeit with mixed trends (a fall of around 18% for raw products, but an increase of around 15% for works using these metals). On the other hand, the volume of shipments increased for other product categories, notably plastics (+180% over the first 8 months), rubber (+70%) and textiles (+50%), with trends remaining favourable overall until August.

This fall in Luxembourg’s export volumes needs to be considered in the context of the trend observed at European level, i.e. an even steeper decline of almost 10% for the EU as a whole (still over the first 8 months of 2025). However, the results vary greatly from one Member State to another. The downturn in Europe was due mainly to declines in Spain (-20%), the Netherlands (-12%) and - to a lesser extent - Finland (-27%), Greece (-20%) and Germany (-6%). Other countries have seen double-digit growth over the same period, notably Belgium, Denmark and Ireland.

[1] This rate applies to all countries except the UK (which continues to benefit from the 25% rate).

[2] See study 7.1, "A trade war clouded by uncertainty", Note de conjoncture 1-25.

Volume of exports of goods from Luxembourg to the United States

Fall in volume, rise in value

Considering the value of goods exports to the United States, Luxembourg displayed a year-on-year increase of around 15% (over the first 8 months), a result which again compares favourably with the European trend (+10% over the same period).

This increase in value in the face of a fall in volume, or alternatively a smaller fall in value than in volume, reflects an increase in the proportion of more expensive products exported compared with last year, and concerns a majority of EU countries. As a result, the United States' share of Luxembourg's total exports of goods in value terms will remain similar in 2025 (at least over the first 8 months of the year) to that recorded in previous years, i.e. slightly above 3%.

The fact remains that the value of goods exports to the United States has tended to fall in recent months in many European countries, but not in Luxembourg, where it has remained relatively stable. It should be noted, however, that exports to the United States had risen sharply at the start of the year in anticipation of the increase in US customs duties for several EU countries (though not significantly in Luxembourg), leading to a mechanical downward adjustment thereafter. The question remains as to whether the recent fall in EU shipments to the United States is still the result of this adjustment, or whether it will become a lasting trend.

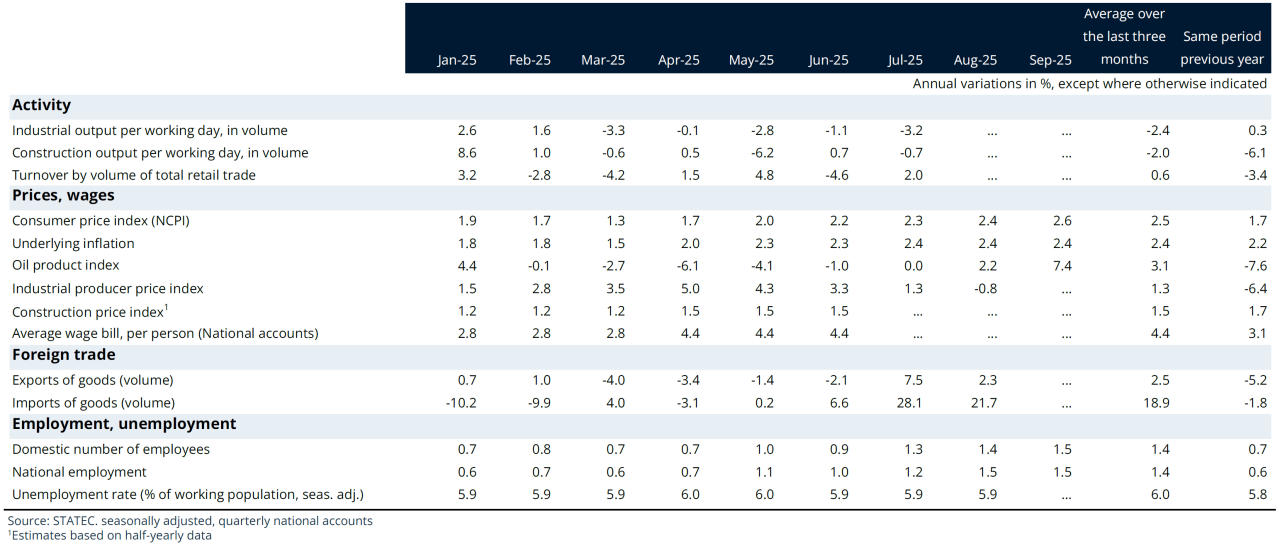

Activity

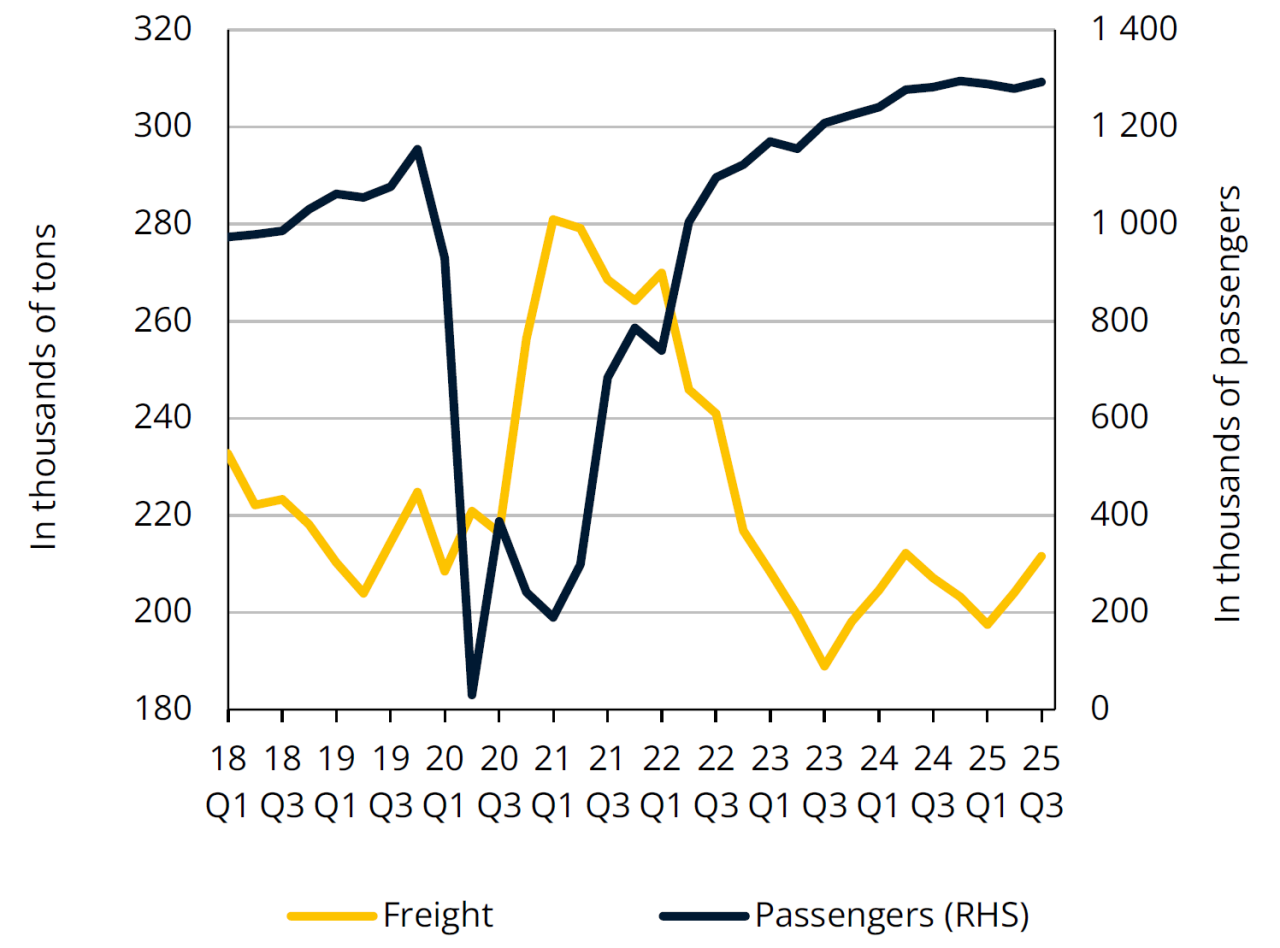

Air traffic at Findel airport

Sources: ANA, STATEC (seasonally adjusted data)

Little dynamism in the air transport sector

The number of passengers recorded at Luxembourg airport is stabilizing. Over the first nine months of 2025, it rose by 1.2% year-on-year. In 2024, it grew by around 7.5%, a result very similar to those observed in Germany and Belgium (the increase was less pronounced in France, +4.5%), and exceeded the 5 million mark for the first time (which should still be the case this year). It should be noted that the number of passengers in Luxembourg had already exceeded its pre-pandemic level by 2023, whereas this was not yet the case for Luxembourg's three neighboring countries in 2024 (‑12% compared to 2019 in Germany, -2% in Belgium, and -1% in France).

In the field of air freight, Luxembourg experienced an almost reverse trend, with a sharp increase in tonnage during the pandemic crisis (this was also the case for Belgium from 2020, but only from 2021 in France and Germany) followed by a decline from 2022 onwards. After reaching a low point in the third quarter of 2023, charter volumes resumed a moderate upward trend but remain slightly below re-COVID levels.

Property

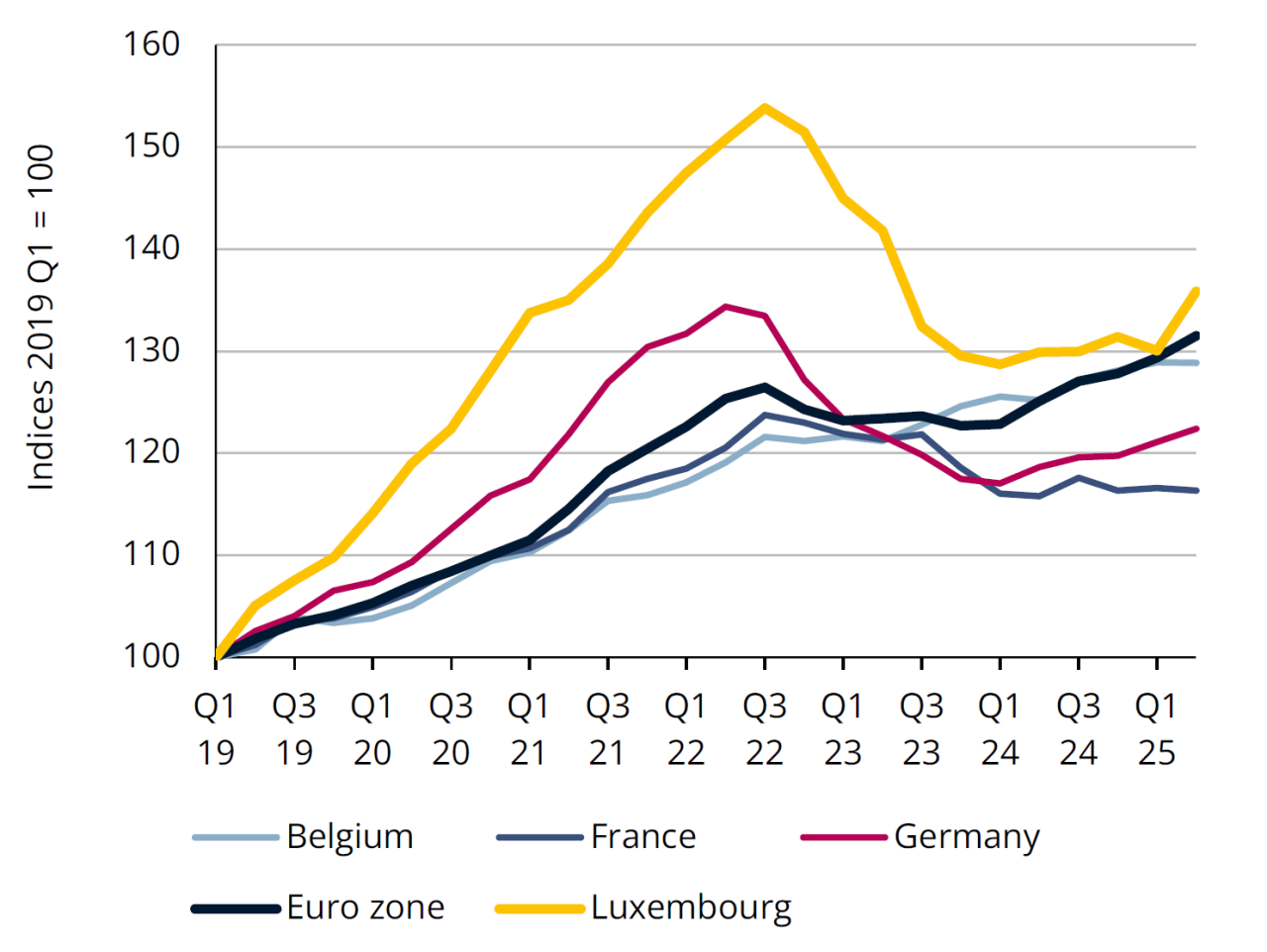

Sales prices of housing

Sources: Eurostat, STATEC

Property prices remain on an upward trend

In the 2nd quarter of 2025, house prices in Luxembourg rose by 4.5% over the quarter, after a drop of -1% in the previous quarter. As in the case of transactions, this particularly strong increase may be due to a temporary effect caused by the expiration of government measures at the end of June. Housing transactions surged in the 2nd quarter (to over 3,000, representing an 85% year-on-year increase), although a lower level is expected in the 3rd quarter given the amount of new loans granted during the summer (as at the turn of the year, although the underlying trend should remain upwards).

In the euro zone, house prices rose by 5% year-on-year, with however major disparities. The only country to still show a fall in prices is Finland (-1%), while others are showing record increases (e.g. Portugal with +17% or Spain with +13%). In France, prices are stagnating and in Germany growth is rather timid (+3% compared with +7% on average between 2016 and 2022). In Luxembourg, France and Germany, prices are still clearly below the peak observed in 2022.

Financial sector

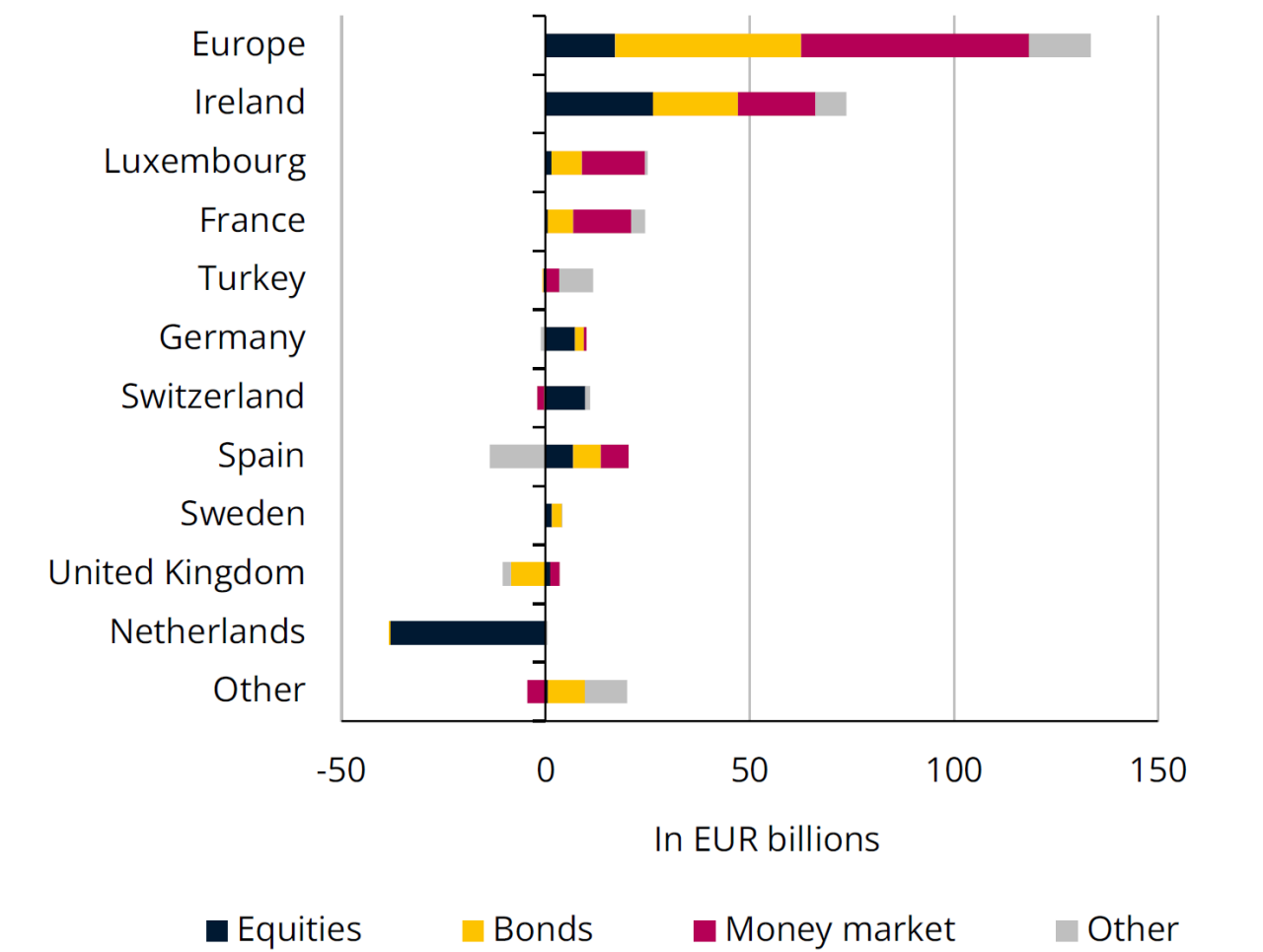

Net issues in UCIs in H1 2025

Source: EFAMA

Higher issues in bond and money market funds

In the 1st half of 2025, collective investment undertakings recorded net inflows of EUR 133 billion in Europe, three-quarters of which related to fixed-income assets (bonds and money markets). In Luxembourg, 91% of net issues were recorded in bond or money market funds, compared with 54% in Ireland. Ireland is still a major magnet for capital in equity and bond exchange-traded funds (ETFs). These ETFs accounted for almost half of net issuance in Europe in the 1st half of the year, with two-thirds going to Ireland and a quarter to Luxembourg (which has exempted from subscription tax all ETFs, including actively managed funds since January). Ireland saw its market share increase to 21.3% (+0.9 % points year-on-year), moving closer to the share held by Luxembourg (which fell by 0.7 % points to 24.6%).

Investor confidence improved further in Q3, supported by a less uncertain outlook for future US trade and monetary policy. The markets were mainly influenced by expectations of interest rate cuts in the United States, while no further cuts are expected in the euro zone since June. Long-term rates, on the other hand, are on the rise. Against this backdrop, equity and fixed-income UCI categories recorded positive capital investment overall. Net issuance in Luxembourg funds has even reached in August a record level since 2021.

Inflation

Prices linked to education and childhood

Source: STATEC, seasonally adjusted data

*The components (educational books, teaching, canteens, boarding schools, crèches and day-care centres, children's clothing and footwear) account for 4% of the NICP basket.

Education and childcare prices bounce back

Over the last decade, the expenses associated with childhood and education have benefited from a number of cost-cutting measures: introduction of more advantageous rates for nursery and daycare centres from October 2017, free textbooks in secondary education since the start of the 2018/2019 school year, free crèches and daycare centres for children in basic education during school weeks and free school canteen meals since the start of the 2022/2023 school year. The start of the 2025/2026 academic year was nevertheless marked by a doubling of tuition fees at the University of Luxembourg, making a significant contribution (0.1% points) to overall inflation in September (2.6%).

Growth in education and child-related prices has been limited to just 1.0% a year over the last ten years (compared with around 1.7% in the euro zone), i.e. a cumulative rise of 10.5% in Luxembourg between September 2015 and September 2025. Over this period, the price of educational books fell by 91.5%, canteen prices by 17.2% and nursery and daycare centres by 2.7%. By contrast, education prices rose by 29.8%, boarding schools by 23.4% and children's clothing and footwear by 21.2%.

Labour Market

Labour hoarding indicator in Luxembourg

Source: STATEC - Business surveys, seasonally adjusted and smoothed data

Workforce retention remains high

Since 2023, the European Commission has been calculating a labour hoarding indicator based on business survey data. It measures the extent to which companies plan to retain their employees despite a deterioration in their business prospects.

Overall, this indicator shows similar trends in Luxembourg and the euro zone, with sharp rises at the time of the Covid pandemic (2020) and the energy crisis (2022-23). The indicator subsequently fell back slightly, but remains at a relatively high level compared with the pre-pandemic period.

This decline in labour hoarding can be seen in most sectors (industry, commerce and services), both in Luxembourg and in the euro zone, with the notable exception of construction. Retention in this sector is tending to stabilise in the euro zone, but has continued to rise in the Grand Duchy this year (after two years of very strong growth, reflecting the particularly marked deterioration in construction activity).

Energy

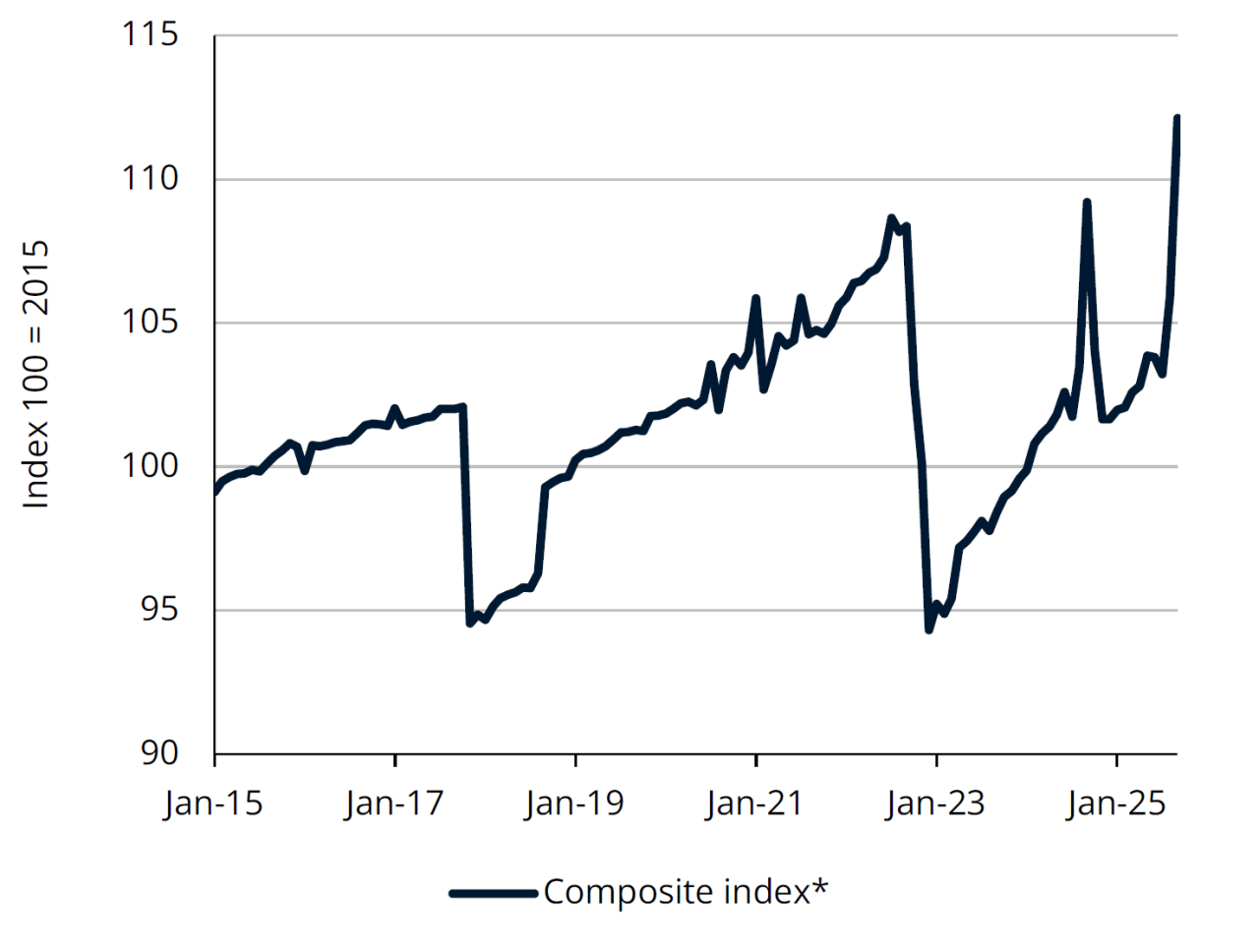

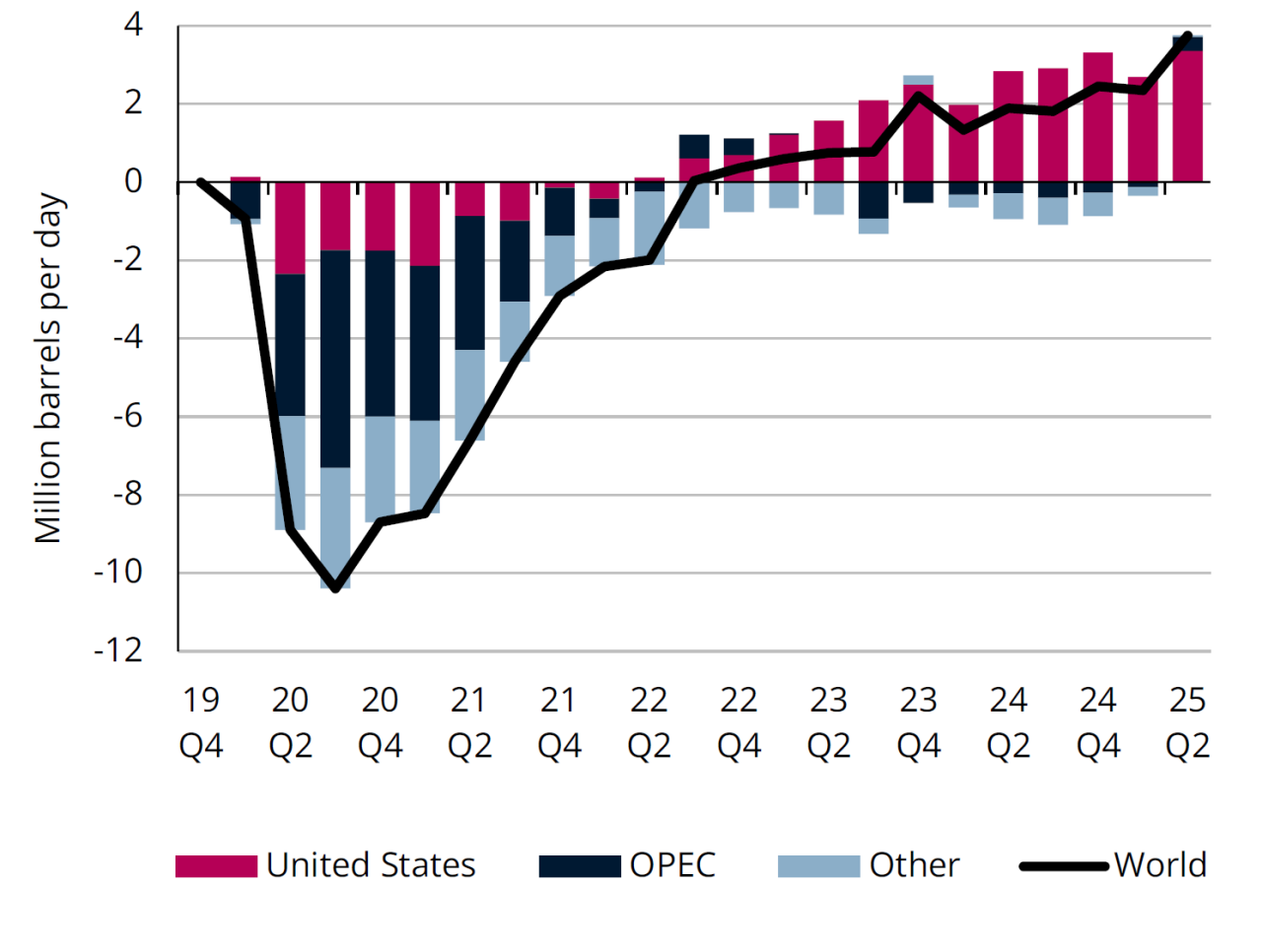

Change in oil production compared to the end of 2019

Source: U.S. Energy information administration

World oil production continues to increase

After the historic fall in world oil production linked to the Covid crisis (with negative prices on US futures contracts in April 2020), oil production rebounded strongly, reaching a new record in the 2nd quarter of 2025. The increase in production compared with the pre-Covid situation was almost entirely driven by the United States, now the world's leading producer – even before the return of Donald Trump and his "Drill Baby Drill" policy. It is only since the beginning of 2025 that OPEC countries have begun to increase their production again, following the cuts introduced at the end of 2022.

This increase in world production may come as a surprise, given that, since the end of 2022, the price of oil has been on a downward trend (Brent crude is currently at USD 61/barrel, its lowest level since 2021), with production rising faster than world consumption. The surplus production seems to have been absorbed mainly by a rise in strategic stocks, especially in China, which has likely prevented prices from falling even further. However, further growth in production remains uncertain in the face of expectations that oil prices will remain relatively low in 2026.

Public finances

Tax receipts

Sources: STATEC, AED (cash basis data)

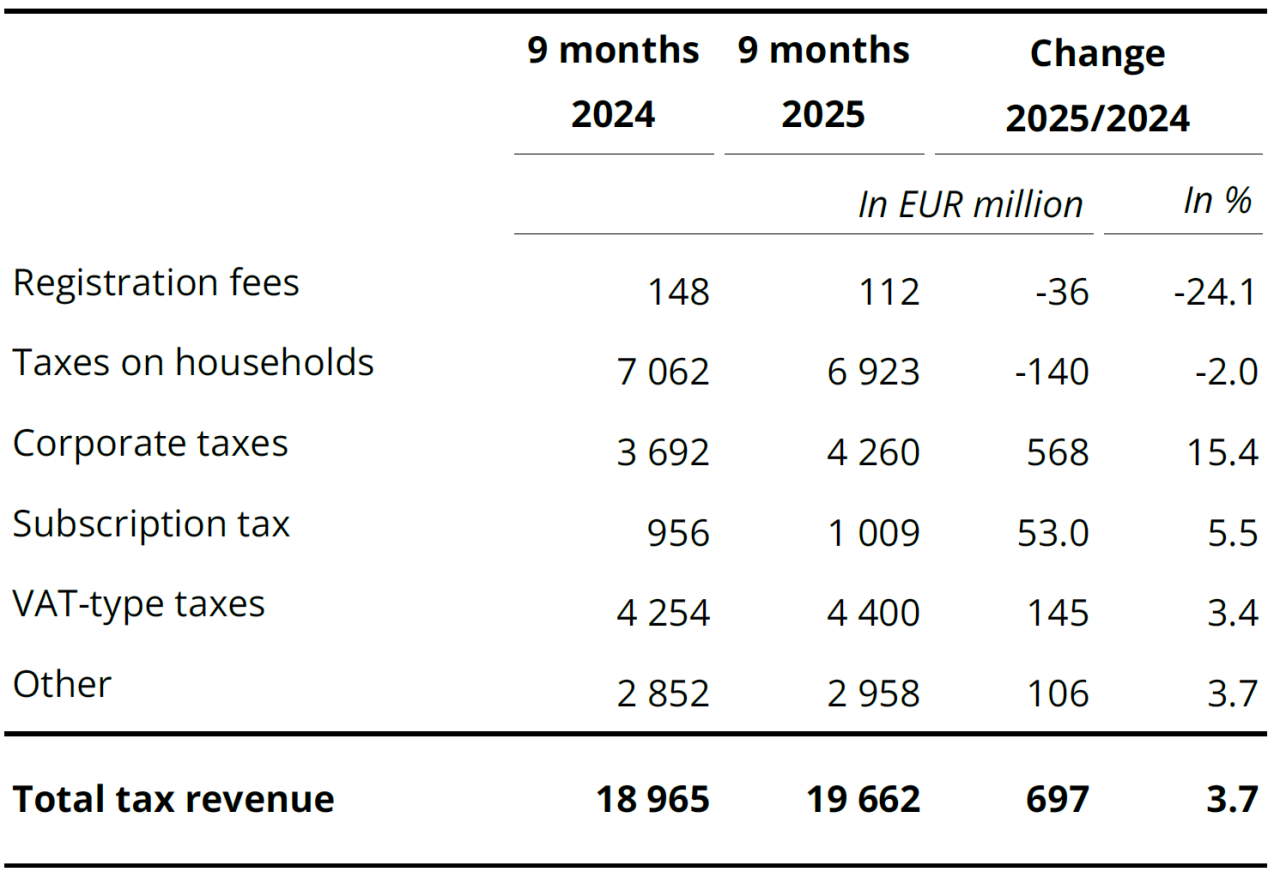

Support measures slow revenue growth

Growth in tax revenues is slowing sharply, rising by just 3.7% year-on-year in September (following growth of +13% in 2024, on a cash basis). Registration fees fell by 24% despite a rise in property transactions (+68% in the 1st half of the year). This fall is a direct consequence of the halving of the tax base. Taxes collected on household income fell by 2% due to adjustments to tax scales, a lower level of progress in the processing of files and a fall in capital gains. Corporation tax, which had risen sharply at the turn of 2025 under the impetus of a few companies, fell back in the 2nd and 3rd quarters. It should be noted that the rate of corporation tax has been reduced by one percentage point since the beginning of 2025.

The 2026 budget proposal incorporates new measures that should have a positive impact on revenues: the increase in contribution rates linked to the reform of the pension system (EUR +378 million from 2026 according to the estimates in the proposal), the introduction of the "Pillar 2" minimum tax on companies (EUR +80 million) and the increase in excise duty on tobacco and cigarettes (EUR +35 million).

Dashboard

Indicators

Dernière modification le