Conjoncture Flash January 2025: Industry faces increased international competition

Since 2023, European industries have reported increased competition from third countries. Luxembourg has not been spared and several major industrial sectors have been affected.

European industry remains in difficulty. Despite a slight recovery in industrial production in the eurozone in October and November 2024, it remains around 5% below the average level recorded in 2022[1]. The decline in industrial production witnessed since 2023 reflects a number of factors, such as the rise in energy prices linked to the consequences of the war in Ukraine, the weakness of construction activity in several European countries (and hence lower demand for industrial products from this sector), and the sluggishness of the European car market (which is impacting car manufacturers).

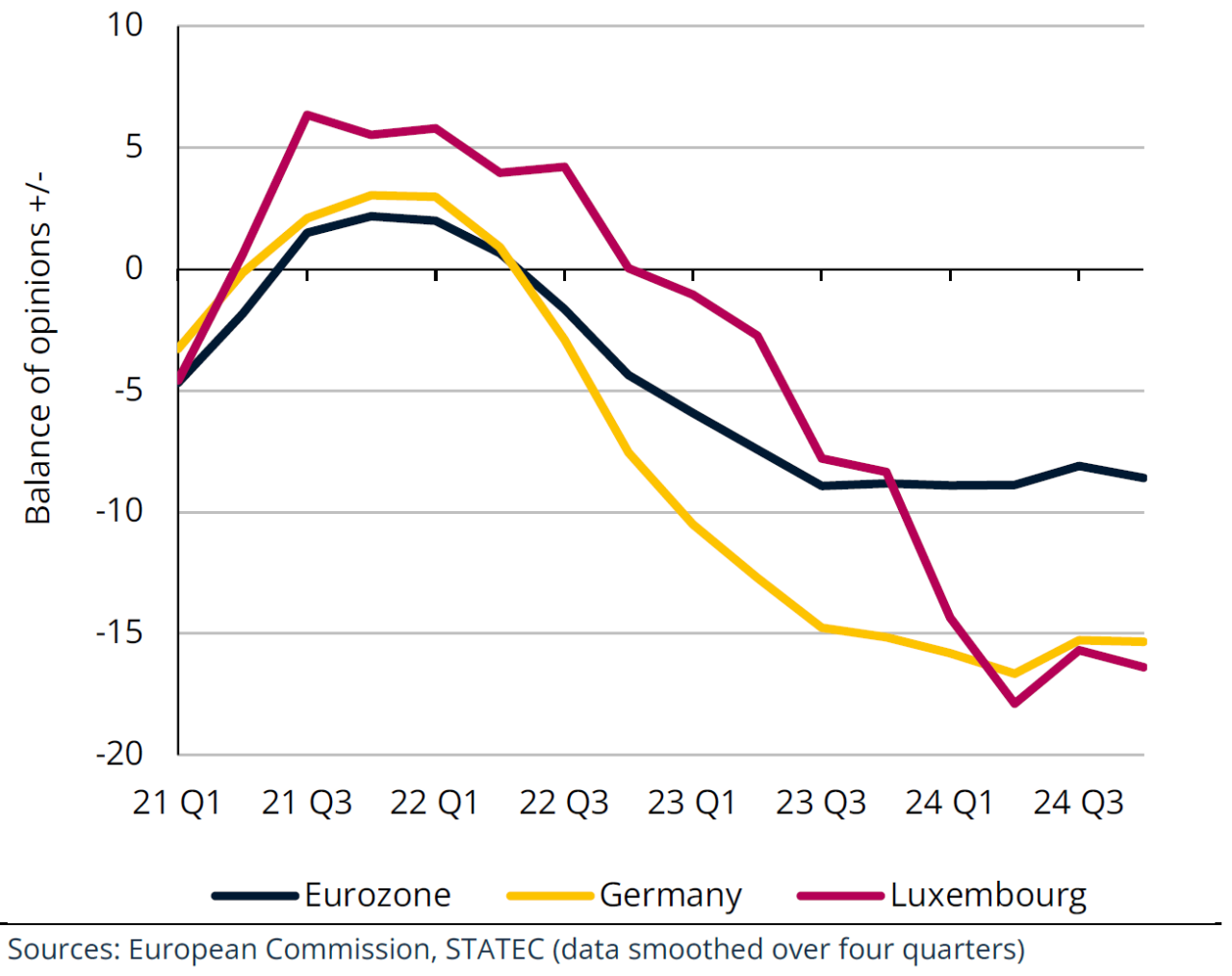

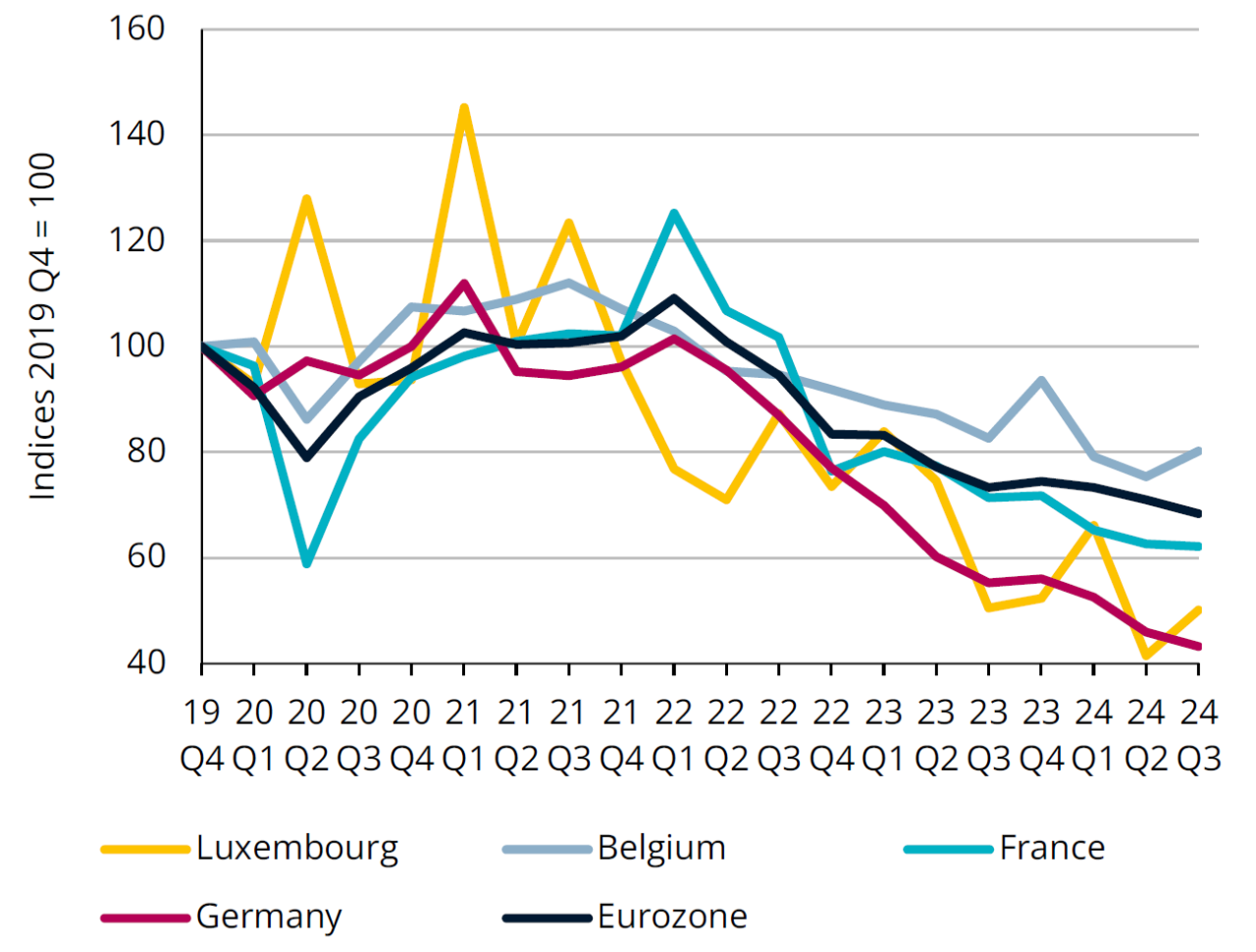

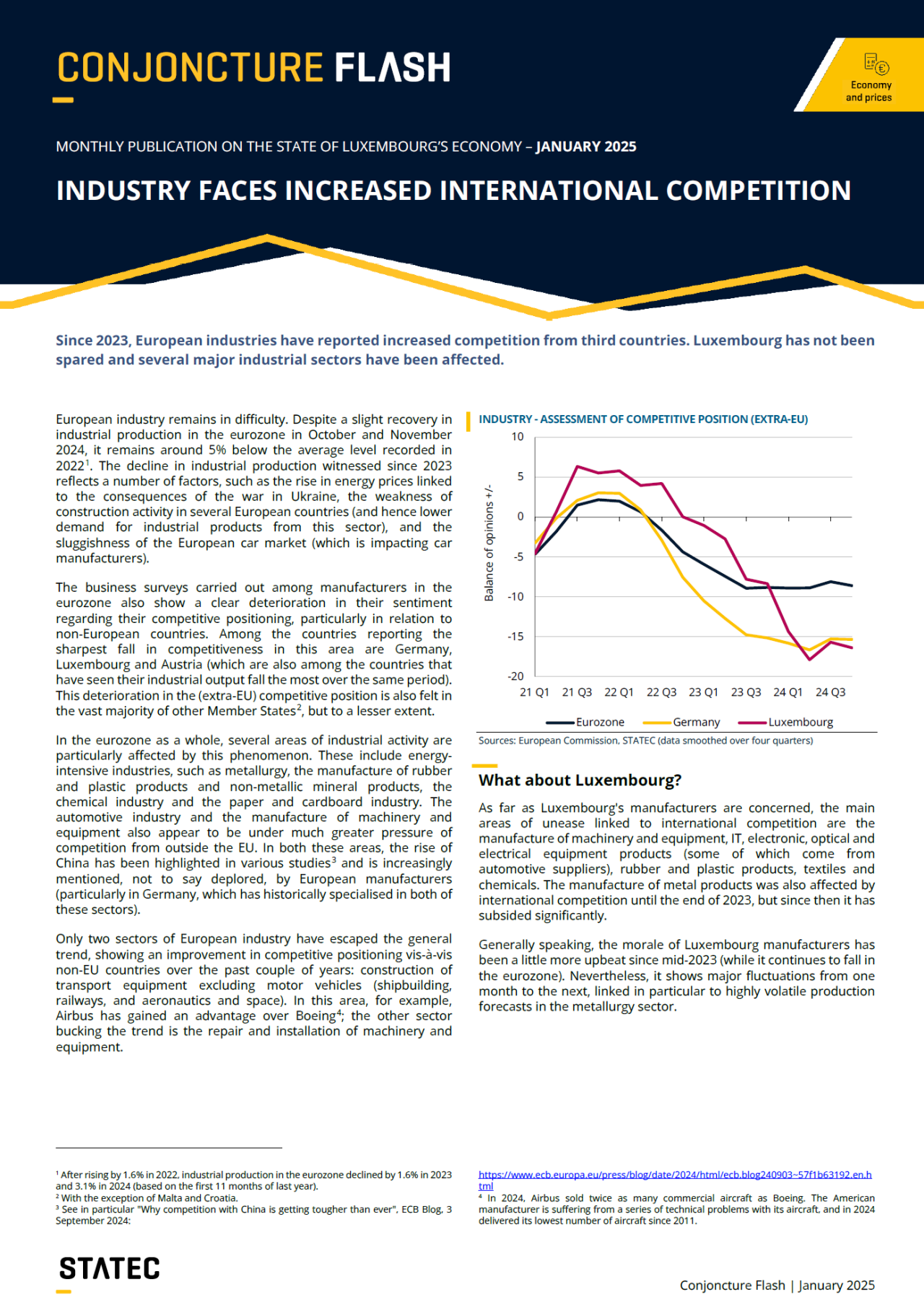

The business surveys carried out among manufacturers in the eurozone also show a clear deterioration in their sentiment regarding their competitive positioning, particularly in relation to non-European countries. Among the countries reporting the sharpest fall in competitiveness in this area are Germany, Luxembourg and Austria (which are also among the countries that have seen their industrial output fall the most over the same period). This deterioration in the (extra-EU) competitive position is also felt in the vast majority of other Member States[2], but to a lesser extent.

In the eurozone as a whole, several areas of industrial activity are particularly affected by this phenomenon. These include energy-intensive industries, such as metallurgy, the manufacture of rubber and plastic products and non-metallic mineral products, the chemical industry and the paper and cardboard industry. The automotive industry and the manufacture of machinery and equipment also appear to be under much greater pressure of competition from outside the EU. In both these areas, the rise of China has been highlighted in various studies[3] and is increasingly mentioned, not to say deplored, by European manufacturers (particularly in Germany, which has historically specialised in both of these sectors).

Only two sectors of European industry have escaped the general trend, showing an improvement in competitive positioning vis-à-vis non-EU countries over the past couple of years: construction of transport equipment excluding motor vehicles (shipbuilding, railways, and aeronautics and space). In this area, for example, Airbus has gained an advantage over Boeing[4]; the other sector bucking the trend is the repair and installation of machinery and equipment.

Industry - assessment of competitive position (extra-EU)

What about Luxembourg?

As far as Luxembourg's manufacturers are concerned, the main areas of unease linked to international competition are the manufacture of machinery and equipment, IT, electronic, optical and electrical equipment products (some of which come from automotive suppliers), rubber and plastic products, textiles and chemicals. The manufacture of metal products was also affected by international competition until the end of 2023, but since then it has subsided significantly.

Generally speaking, the morale of Luxembourg manufacturers has been a little more upbeat since mid-2023 (while it continues to fall in the eurozone). Nevertheless, it shows major fluctuations from one month to the next, linked in particular to highly volatile production forecasts in the metallurgy sector.

[1] After rising by 1.6% in 2022, industrial production in the eurozone declined by 1.6% in 2023 and 3.1% in 2024 (based on the first 11 months of last year).

[2] With the exception of Malta and Croatia.

[3] See in particular "Why competition with China is getting tougher than ever", ECB Blog, 3 September 2024:

https://www.ecb.europa.eu/press/blog/date/2024/html/ecb.blog240903~57f1b63192.en.html

[4] In 2024, Airbus sold twice as many commercial aircraft as Boeing. The American manufacturer is suffering from a series of technical problems with its aircraft, and in 2024 delivered its lowest number of aircraft since 2011.

International

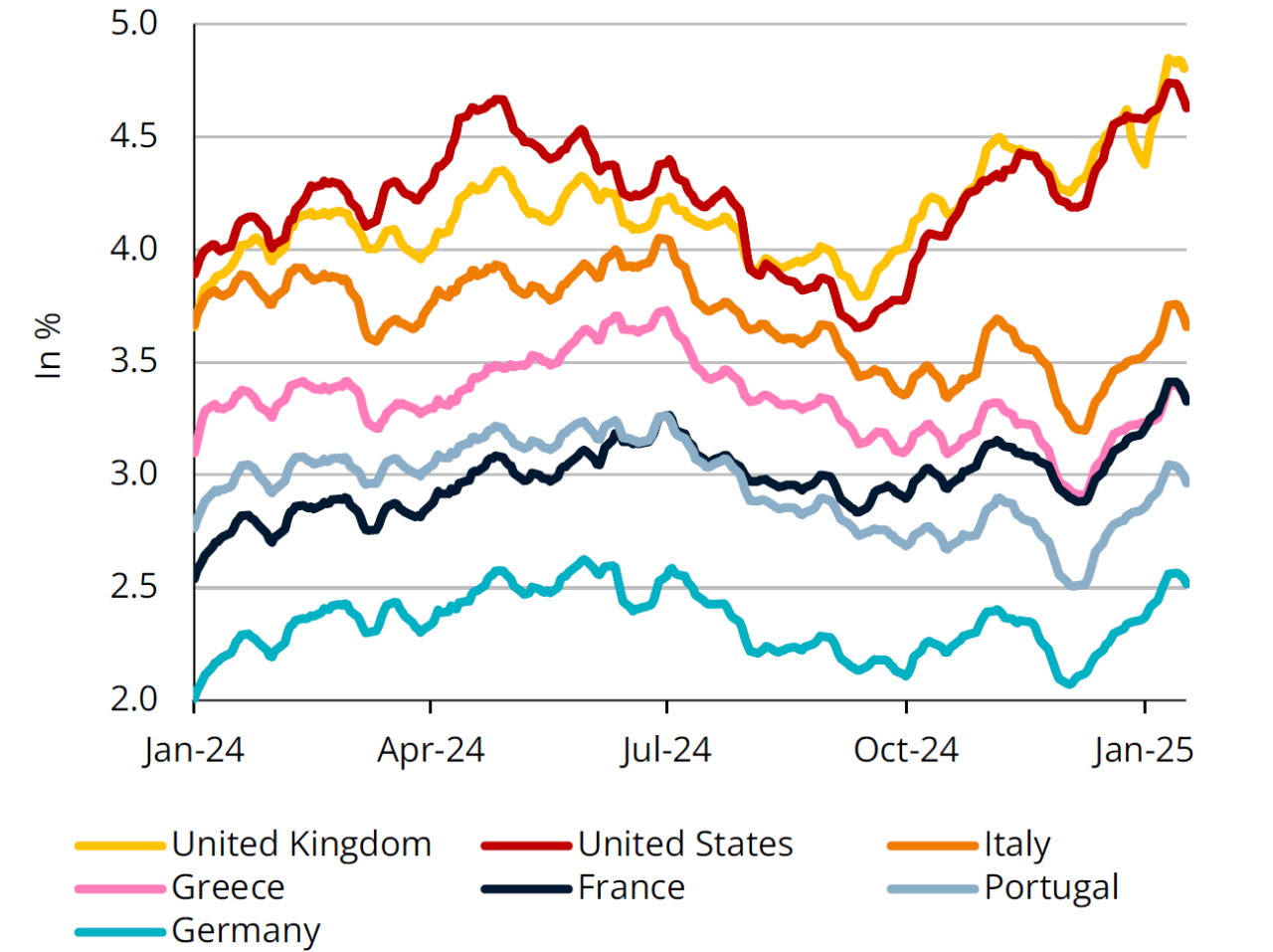

10-year government bond yields

Source: Macrobond (five-day centred moving averages)

Sovereign yields torn between political risks and inflation expectations

Government bond yields and the outlook for inflation reveal no clear trend. Inflation has slowed sharply in recent months, but the measures planned by the new US and UK governments have increased expectations of an upturn in prices. Since mid-2024, two countries have stood out from the others - France and the United Kingdom. In France, yields and spreads against German Bunds rose by 30 basis points following the legislative elections in the summer of 2024, and subsequently by a further 15 basis points when the Barnier government collapsed in December. The markets are also concerned about the UK government's spending and tax plans, which include a number of potentially inflationary measures (notably a rise in the minimum wage and employers' national insurance contributions). As a result, the yield on the UK bond reached its highest level since the 2008 financial crisis.

In mid-January, sovereign yields started to fall again, buoyed by weaker-than-expected inflation figures in the United States and the United Kingdom. Following a fall in US sovereign yields, European yields followed suit. On the futures markets, projections point towards a rate cut by the Fed in July 2025

Financial environment

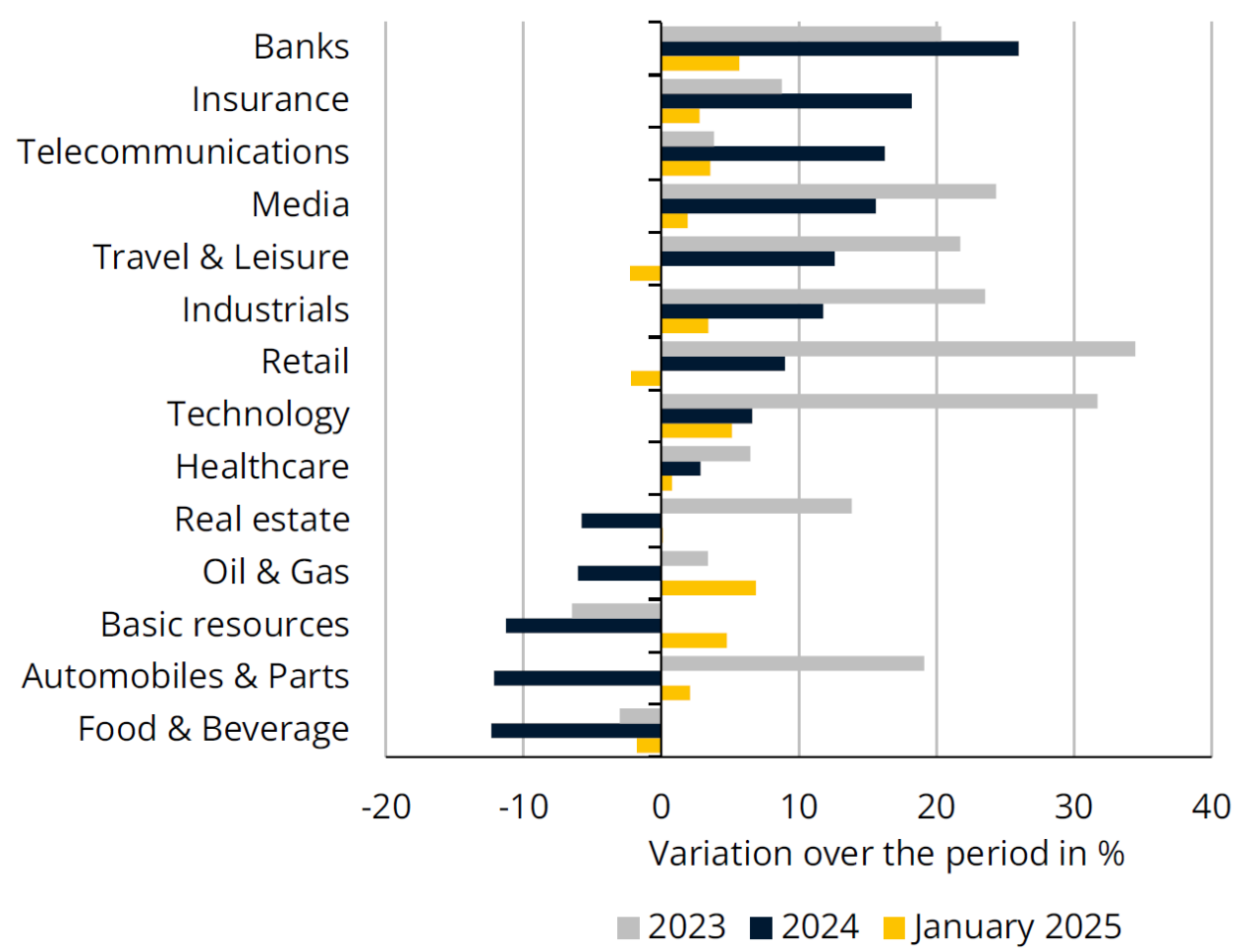

Euro Stoxx 600 sectors

Source: Macrobond

Contrasting stock market trends by sector

In the wake of a 13% increase in 2023, the Euro Stoxx 600 European stock market index rose by 6% in 2024. It was boosted by encouraging earnings in banking, insurance and telecommunications, three sectors that continue to rise at the start of 2025. Valuations in the industrial, retail and technology sectors slowed sharply in 2024 and early 2025, while real estate has been on a downward trend since autumn 2024. Stocks linked to the oil, gas, basic resources and automotive sectors, which had fallen dramatically in 2024, are back on the rise at the start of 2025.

Budgetary and monetary policy decisions in Europe and the United States will have a major impact on European equities. Lower key rates should support the economic recovery and share prices in the real estate, construction, consumer staples and commodities sectors, amongst others. On the other hand, it could have a negative impact on the revenues and valuations of banks and insurance companies. Fears about US tariffs on imports from the EU could continue to weigh on the automotive sector.

Activity

Confidence indicator in non-financial services

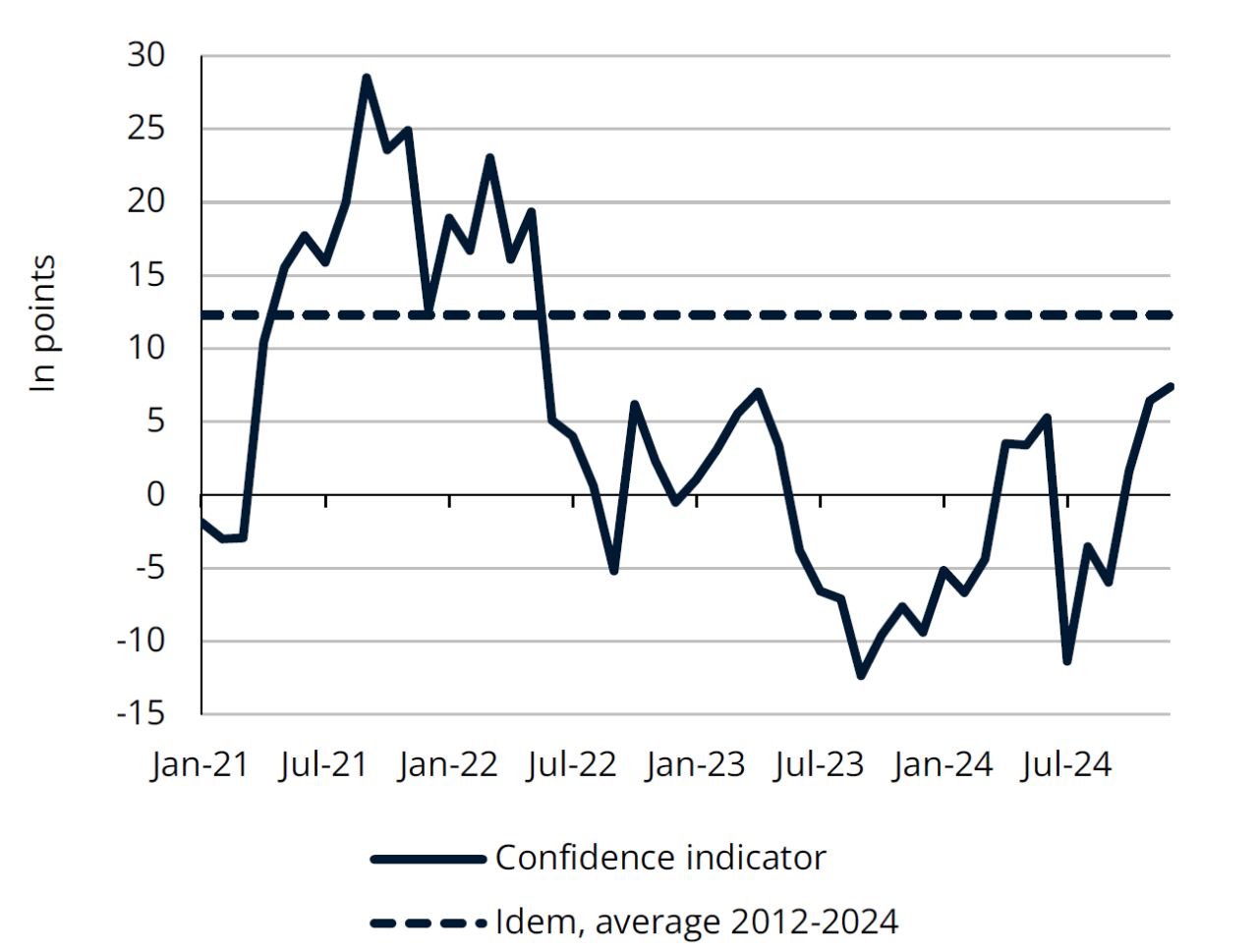

Source: STATEC (latest point: December 2024)

Confidence in services back on track

The morale of Luxembourg's non-financial services companies has been affected by considerable volatility over the past year. It recovered significantly in the first half of 2024 and fell back slightly in Q3. Subsequently, it has resumed its upward trend. In December 2024, the corresponding confidence indicator reached 7.4 points, the best result since May 2022 (but still below its long-term average).

This recent upturn in confidence in services in the Grand Duchy is, above all, linked to the improvement in the perception of demand (both in terms of recent developments and expectations). In the eurozone, confidence in services tended to decline towards the end of 2024. This phenomenon benefits several types of service activities, including legal and accounting services, rental services, air transport, postal and courier services and catering. For other categories, however, the end of 2024 was marked by a deterioration in earnings, particularly in land transport, warehousing and auxiliary transport services, accommodation and computer programming and consultancy services.

Real estate

Building permits for residential buildings

Source: Eurostat (seasonally adjusted data m2 of floor space)

Building permits remain very low

In Q3 2024, building permits (measured in m2 of floor space) rose by 13% year-on-year. Approvals for residential buildings, which were clearly on a downward trend in 2022 and 2023, still tend to retract slightly in recent quarters. They remain historically low, at levels last seen in the early 2000s (and less than half their average over the 2015-2022 period), echoing the current weakness in new housing transactions. The increase of total building permits, following substantial decreases in previous quarters, came mainly from the non-residential sector (up 36% year-on-year in Q3). These results are particularly volatile (they posting declines of almost 30% year-on-year in the first three quarters of 2024).

Mirroring the situation in Luxembourg, building permits in the eurozone began to fall at the start of 2022 and have yet to show any signs of recovery. Across the eurozone as a whole (including Germany and France) permits for non-residential buildings held up better than those for residential buildings, while in Luxembourg both categories were hit hard. The low levels of building permits in recent quarters suggest that the situation will remain challenging for investment and activity in construction in 2025.

Inflation

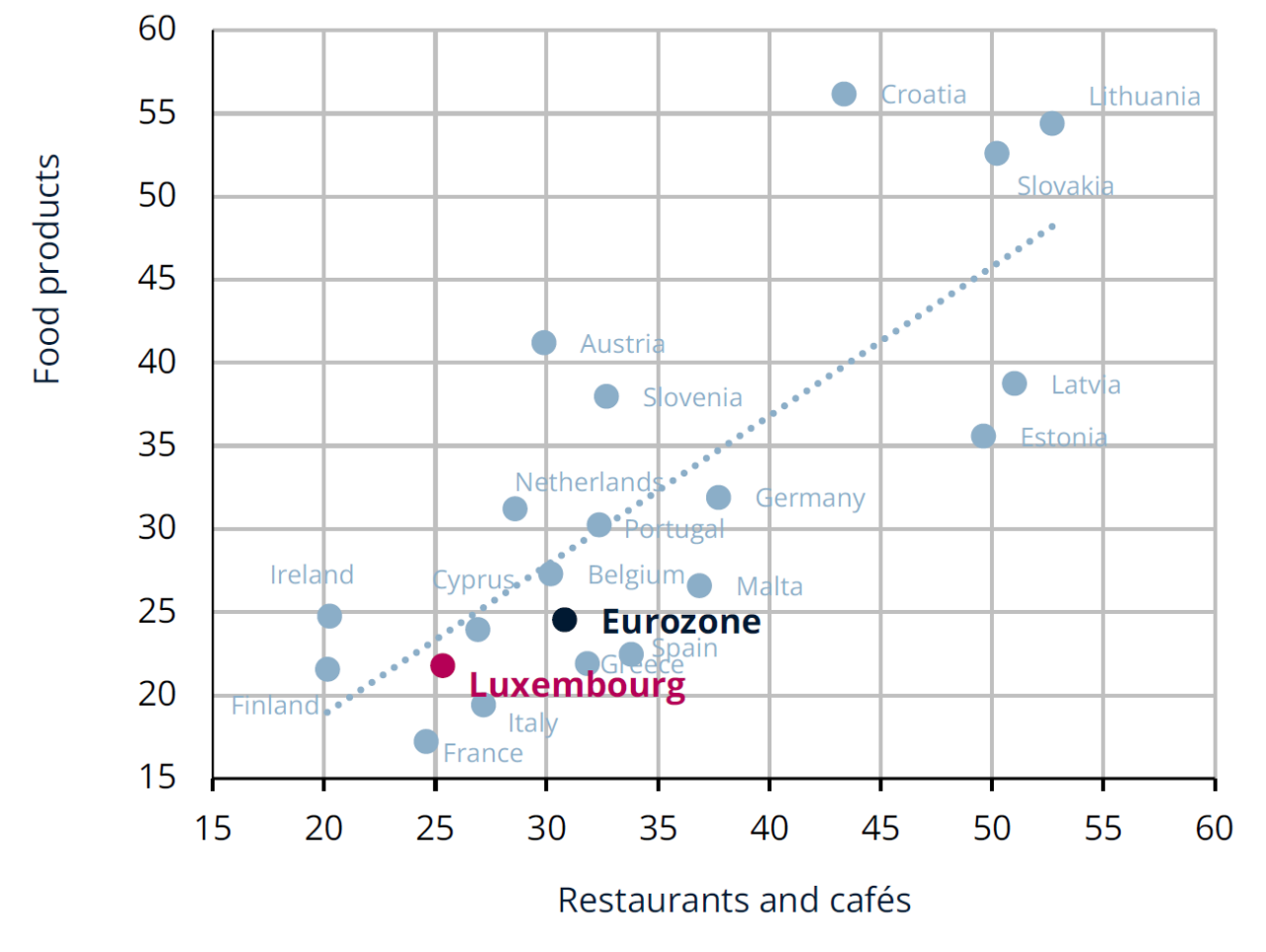

Price rises between December 2019 and December 2024 (in %)

Source: Eurostat, STATEC (Consumer prices)

Restaurant prices affected by multiple crises

The Covid crisis, the explosion in energy prices and, in turn, food prices have led to a significant rise in restaurant and café prices: +25% in the eurozone in December 2024 compared with December 2019. At +22%, Luxembourg was among the countries with the lowest increases over this period, while the Eastern European countries recorded the highest increases (over 50% over the past five years).

In 2024, restaurants and cafés were one of the sectors that most reflect the divergence between inflation in services in Luxembourg and in the eurozone. This trend could be partly explained by lower food inflation in Luxembourg (+25% since Dec 2019, compared with +31% in the eurozone), but also by energy prices. While Luxembourg has seen the highest rise in gas prices for small businesses in the eurozone since the second half of 2019 (+130% until the first half of 2024, compared with +73% in the eurozone), the rise in electricity prices has been among the lowest for businesses consuming less than 20 Mwh (+10% compared with +32% in the eurozone).

It is worth noting that in Luxembourg, it is the small caterers (+25% since Dec 2019) that have posted the highest increases in prices, followed by drinks in restaurants (+24%) and non-alcoholic drinks in cafés (+22%), with meals in restaurants (+21%) and, lastly, alcoholic drinks in cafés (+19%).

Labour market

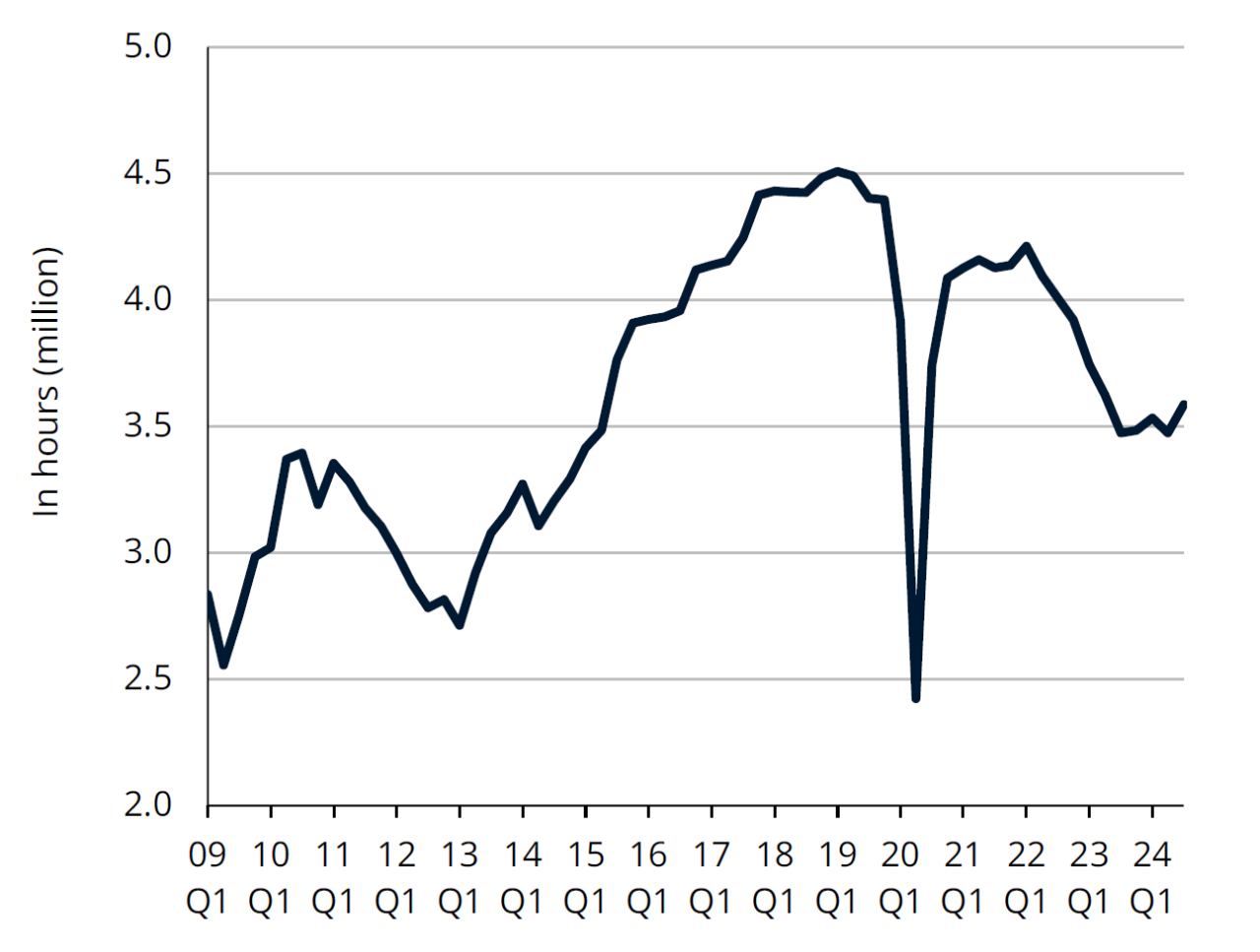

Hours worked by temporary staff

Sources: IGSS, STATEC (seasonally adjusted data)

Temporary work still a long way from pre-crisis levels

Hours worked by temporary staff rose by 3.3% over the quarter in Q3 2024, the strongest increase since Q3 2020 (or since Q4 2017 excluding the Covid crisis). This upturn came mainly from construction (+4.0% over a quarter in Q3 2024), but also from transport (+6.3%) and industry (+1.8%). The number of temporary workers stabilised at just over 7 000 for the first three quarters of 2024 - around 20% below its pre-pandemic level (a fall equivalent to around 1 800 persons).

The proportion of hours worked by temporary staff peaked in 2018 at 2.3% of the total, compared with just 1.6% at present. Construction remains the branch using this flexible form of labor the most (5.6% of hours in 2024 based on the first 9 months), followed by industry (3.8%), transport (2.2%) and Horeca (1.8%). Since 2019, the main sectors which have reduced the use of temporary workers are construction (-27% in terms of hours), industry (-37%) and the financial sector (-46%). Conversely, transport (+35%), business services (+26%) and Horeca (+15%) used it more.

Energy

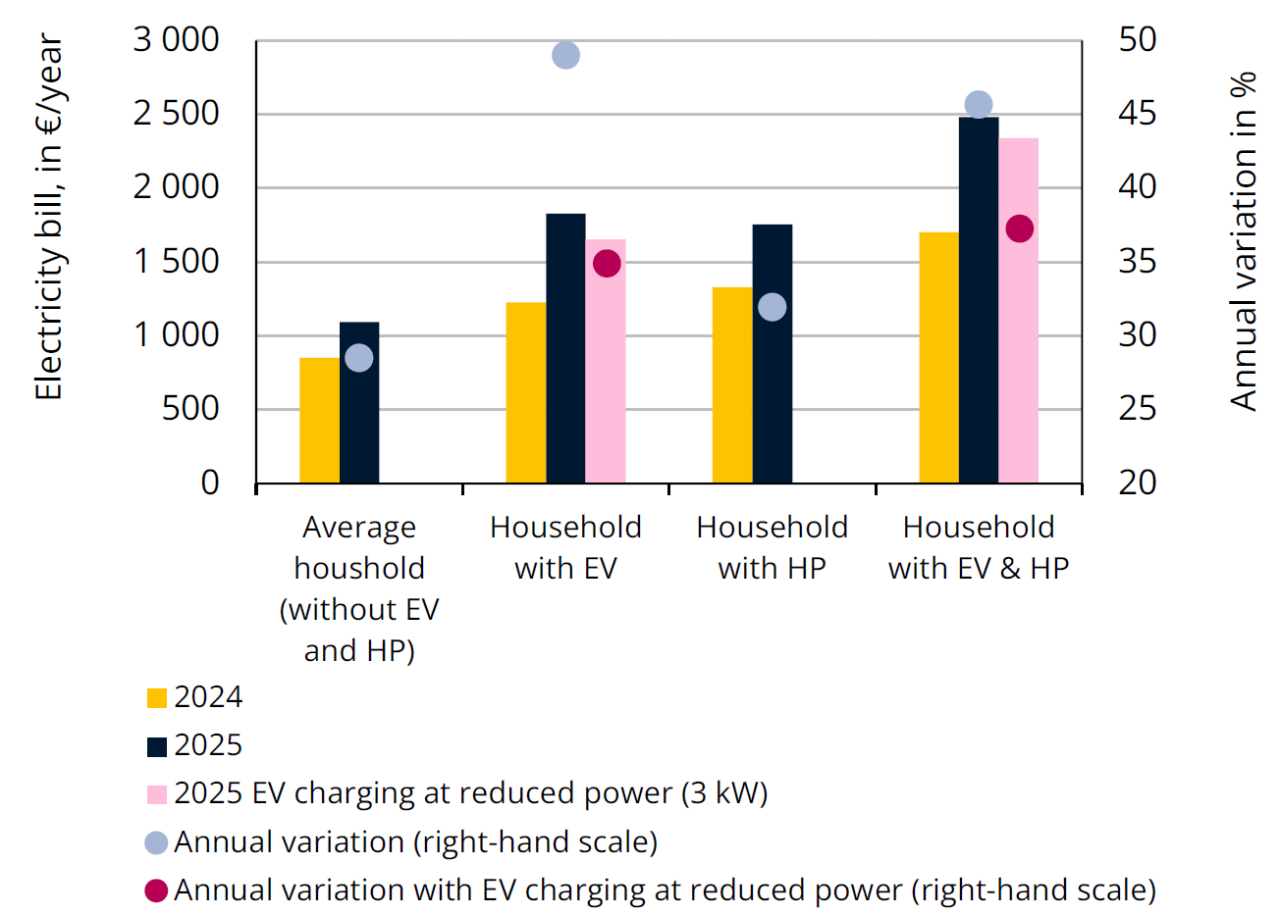

Impact of the new electricity tariffs

Sources: STATEC (EV: Electric vehicle; HP: Heat pump)

Electricity prices set to rise by an average of 30% in 2025

In 2025, electricity prices for private customers are set to rise by an average of 30% as a result of the partial lifting of the tariff shield (introduced at the end of 2022). If the shield had been removed in full at the beginning of this year, prices would have risen by 60%. The price increase includes the impact of the reform of network charges. From now on, these charges will take account not only of the amount of energy consumed, but also of the power used. This reform aims to reduce the need to expand electricity grid capacity as part of the energy transition, by trying to discourage high-capacity peaks.

The impact of these changes varies from household to household, depending in particular on their electrical equipment. For an average household with an annual consumption of around 3,900 kWh, without an electric vehicle (EV) or heat pump (HP), the increase will be just under 30%. A household with a heat pump will see an increase of just over 30%. For a household using an electric vehicle, if charging is carried out using an 11 kW domestic charging point, the increase could be almost 50%. On the other hand, by reducing the charging power to 3 kW, the increase would be limited to around 35%.

Dashboard

Indicators

Last update