Note de conjoncture 1-25

Trapped between military conflicts and trade warsAn uncertain global environment and the faltering pace of activity in Luxembourg at the start of 2025 suggest that growth will remain weak this year, with a slight improvement forecast in 2026.

International environment - stumped by Trump on trade

Inflationary pressures have eased worldwide, giving way to less restrictive monetary policies, particularly in the eurozone. However, other factors linked to the global climate have moved in a less favourable direction in recent months, in particular the massive increases in customs duties emanating from a change in US trade policy. There is still a great deal of uncertainty about the decisions that will actually be taken in this field, whether by the United States or other countries. This lack of visibility is already disrupting the workings of the economy. However, all the forecasters have significantly downgraded their outlook for global activity this year and next.

In the eurozone, growth is likely to remain weak in 2025, at just under 1%, in line with the figure for 2024. It is predicted to pick up only marginally in 2026. A correction on financial markets amid concerns about US economic policy could further reduce growth in the eurozone to a trickle next year. Moreover, the downside risks surrounding these forecasts are predominant, notably given the recent escalation of tensions in the Middle East.

Growth in Luxembourg to remain low in 2025 and 2026

In Luxembourg, the economic recovery displayed signs of faltering at the start of the year. After recovering sharply in Q4 2024, real GDP fell again in Q1 2025, mainly due to a downturn in the financial sector, whose results have been highly volatile in recent quarters. There are slightly more positive signs in industry and construction, but the improvement is still very modest and the level of activity in these two sectors remains well below the level which prevailed at the end of the pandemic (and before the energy crisis). Furthermore, while business confidence in non-financial services has picked up since mid-2024, it is showing more hesitant progress in the first few months of 2025.

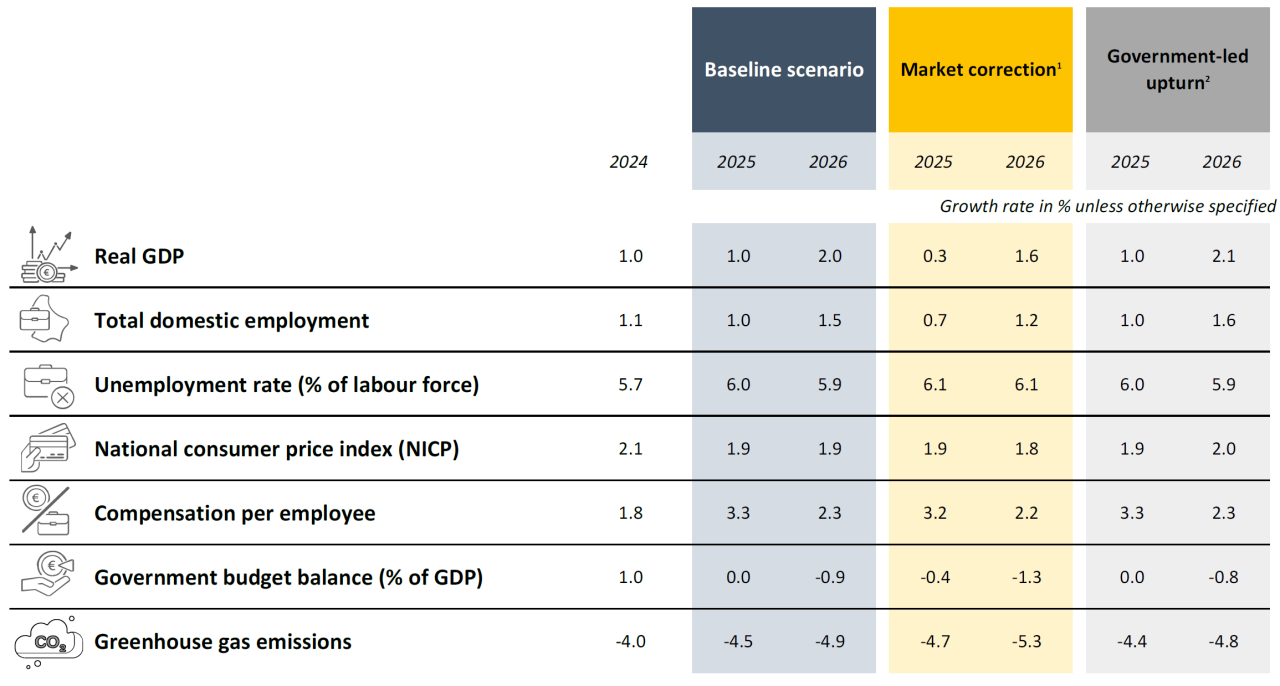

These developments, together with the worsening outlook for the international economic climate, point to a much less pronounced expansion of activity in Luxembourg than forecast last autumn, with GDP growth revised to 1.0% in 2025 and 2.0% in 2026. This trajectory is based in particular on a gradual improvement in the performance of market-based activities, which could be weakened if the uncertainties relating to the international climate were to further destabilise the financial markets.

Limited pressure on prices and wages

Inflation has risen slightly in Luxembourg over the early part of 2025, but this increase is mainly due to isolated events such as the partial lifting of energy price caps and the index bracket of May. Overall, however, consumer price pressures remain stable in the Grand Duchy, in line with eurozone data. Furthermore, as already observed in 2024, Luxembourg continues to show relatively low inflation in services and food compared with other European countries.

Price stability should not be jeopardised in Luxembourg over the next two years. On the one hand, increased trade tensions would not translate into additional inflationary pressures. On the other hand, the worsening economic outlook, both in the eurozone and in Luxembourg, will tend to put the brakes on price rises.

STATEC is forecasting inflation of just under 2% in both 2025 and 2026, meaning that the next wage indexation will be in Q3 2026.

Against a backdrop of contained inflationary pressures, wage inflation slowed across the eurozone in late 2024 and early 2025. In Luxembourg, this slowdown is associated in particular with the frequency of index brackets. Moreover, the temporary reduction in employers' contributions has limited the growth in labour costs in 2024, but their normalisation will support growth in 2025. Thus, for this year, an increase in wage costs of 3.3% is anticipated, followed by +2.3% in 2026.

Job creation at a record low, with a slight improvement expected by 2026

The labour market remains sluggish in the eurozone, except in the southern countries, notably Spain. In Luxembourg, employment growth has slowed markedly since 2022 and appears to be stabilising at a historically low level at the turn of 2024 and 2025, particularly in market sectors. The unemployment rate continued to rise at the start of the year, but to a slightly lesser extent than at the end of 2024, due in particular to a smaller fall in the number of construction workers. Some leading employment indicators are sending out slightly more positive signals.

In line with the improvement in economic activity, STATEC forecasts a moderate increase in employment growth and a fall in unemployment, but only from 2026 onwards. Workforce growth in Luxembourg will continue to be characterised by a significant contribution from the public sector, with better support from the market sector next year.

Budget surplus in 2024, balanced in 2025, deficit in 2026

Public revenues show strong growth of 10% in 2024 (a similar rate to 2023), boosted mainly by corporation tax and the increase in VAT rates. On the contrary, spending has slowed sharply (from +12% in 2023 to +6% in 2024), in particular subsidies and transfers linked to the energy crisis. This much stronger growth in revenue than expenditure has resulted in a budget surplus of 1% of GDP in 2024.

The public balance should slip back into negative territory by 2026 (0% of GDP in 2025, -0.9% in 2026), due to a significant slowdown in revenue growth, while expenditure should accelerate slightly in 2025 before slowing in 2026. Public revenues are expected to slow as a result of tax cuts for households and the assumption that corporate taxes will lose momentum. Spending would be stimulated by welfare benefits, wages, investment and transfers.

Lower fossil fuel consumption puts emissions on the right track

The global economy remains largely dependent on fossil fuels, which still account for 80% of global energy consumption. The oil market is marked by uncertainty, with the price of Brent crude at its lowest level since 2021. To compensate for the decline in Russian gas, Europe is relying heavily on liquefied natural gas (LNG), which reaches record import levels in spring 2025.

In Luxembourg, fossil fuel consumption has been contracting for several years, mainly due to the fall in sales of petroleum products. STATEC anticipates further falls in sales of motor fuels and deliveries of heating oil of 3.5% and 6.5% respectively in 2025, followed by further falls of the same magnitude in 2026. The rebound in gas and electricity consumption, observed in 2024, eased off at the start of 2025.

In line with these trends in energy consumption, greenhouse gas emissions will continue to decline. STATEC estimates that they will have fallen by 4% by 2024, and forecasts further reductions of 4.5% in 2025 and 5% in 2026. This trend would enable Luxembourg to remain in line with the objectives of the National Integrated Energy and Climate Plan (PNEC).

Thematic studies in this Note

- A trade war clouded by uncertainty

- Is the fall in labour productivity in Luxembourg influenced by labour hoarding?

- New equations for forecasting quarterly inflation in Luxembourg

Macroeconomic forecasts

(Source: STATEC (2025-2026: forecasts)

- In this unfavorable scenario, investor concerns over US policy credibility lead to tighter financial conditions, as higher yields push up lending rates and weigh on stock markets.

- In this favourable scenario, the global economy strengthens amid stimulus and reform in China, and greater defence spending in the EU.

Bureau de presse | Tél 247-84219 | Fax +352 26 20 19 0 | info@statec.etat.lu

Total or partial reproduction of this newsletter is authorized provided that the source is cited.

Last update