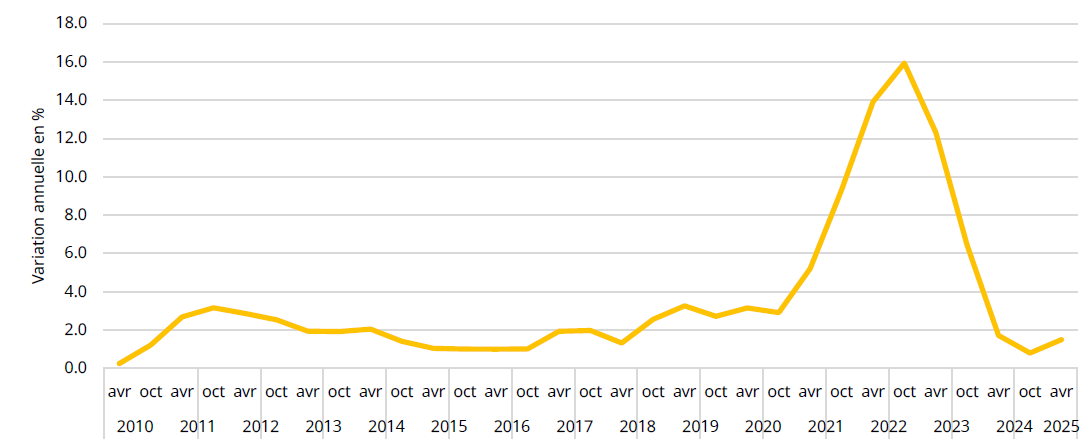

Rebound in residential construction prices

After two quarters of weak growth, residential construction prices rose by 1.3% between October 2024 and April 2025. After the surge in 2021 and 2022, price changes are gradually returning to their long-term average (1.0%) observed between 2010 and 2019. This recovery affects all trades. Over one year, prices in residential construction rose by 1.5%.

Graph 1: EVOLUTION OF THE CONSTRUCTION PRICE INDEX, 2010–2025

Source: STATEC, construction price survey

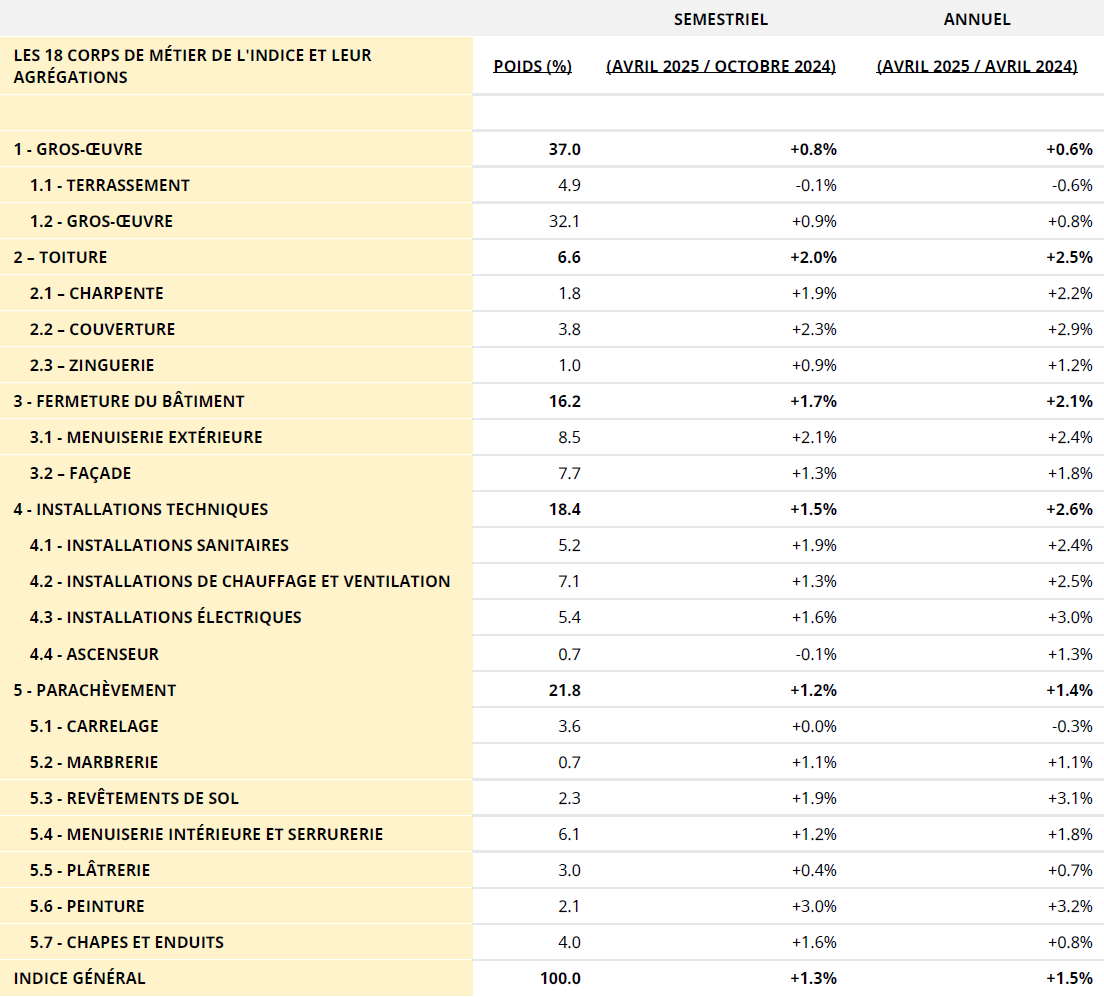

The decline in prices for structural work observed in 2024 has come to a halt, and prices for masonry work (+0.9%) are once again on the rise. Prices for certain materials (iron reinforcements, sand), which rose slightly at the beginning of the year, are being passed on to contractors.

However, structural work remains the trade with the weakest half-yearly growth. Prices for earthworks remain virtually stable (-0.1%). Roofing prices (+2.0%) are seeing the sharpest rebound, influencing the overall trend.

These price variations are partly attributable to increases in the price of wood, insulation materials and other supplies (roof windows, tiles, etc.). As a result, prices for timber frames (+1.7%), insulation work (+2.1%) and roofing (+2.3%) are once again on an upward trend. Overall, roofing remains the trade that has seen the biggest price increases since the materials crisis and the surge in inflation (+45.5% between 2020 and April 2025).

In the building enclosure sector, which includes windows with sun protection devices, garage doors and facades, prices rose by 1.7% between October 2024 and April 2025. Builders will have to pay 2.1% more for exterior carpentry in residential construction and 1.3% more for facade work.

Technical installations, which were particularly dynamic in the last two half-years (+2.5% between October 2023 and April 2024 and +1.1% between April 2024 and October 2024) despite a tense environment, continue to grow at a steady pace (+1.5%). This momentum is being driven by all trades, including sanitary installations (+1.9%), heating and ventilation installations (+1.3%) and electrical installations (+1.6%). This sustained growth is mainly due to higher supply prices, which are being passed on to project owners.

The rebound in prices is also evident in the finishing sector, albeit to a lesser extent. Only painting (3.0%), floor coverings (+1.9%) and screeds and plasters (+1.6%) are growing faster than the general index (+1.3%). Other finishing services, such as tiling (+0.0%) and plastering (+0.4%), tended to stagnate or increase only slightly. Apart from structural work, the finishing of residential construction saw the smallest change over the year (+1.4%).

Table 1: RATES OF CHANGE IN APRIL 2025

Source: STATEC, construction price survey

The general composite index for April 2025, expressed on a base of 100 in 1970, stands at 1164.15 points. This index is used to index almost all fire insurance contracts, as well as for many other applications such as updating estimates or contracts for sale of property under construction.

The construction price index measures price changes (excluding VAT) for services provided in residential construction, excluding land costs. It takes into account changes in material and labour prices, as well as changes in productivity and margins for contractors. Indices and rates of change are calculated every six months for construction as a whole, but also for different trades and service groups.

This index is published twice a year, in January for data from October of the previous year and in July for data from April. It is available on the statistics portal under ‘Short-term indicators, series A2’.

The results of the October 2025 index will be published on 14 January 2026, following the half-yearly meeting of the Technical Advisory Committee on the Construction Price Index.

Contact

Bureau de presse| +352 247-88 455 | press@statec.etat.lu

This publication was produced by Marc Ferring / Lucien May.

STATEC would like to thank all the collaborators who contributed to the production of this publication.

Reproduction in whole or in part of this press release is authorized provided the source is acknowledged.

Last update