Medium-term projections (2025-2029)

At the end of August, STATEC submitted an update of its medium-term projections to the Ministry of Finance. These data feed into the process of drawing up the State Budget.

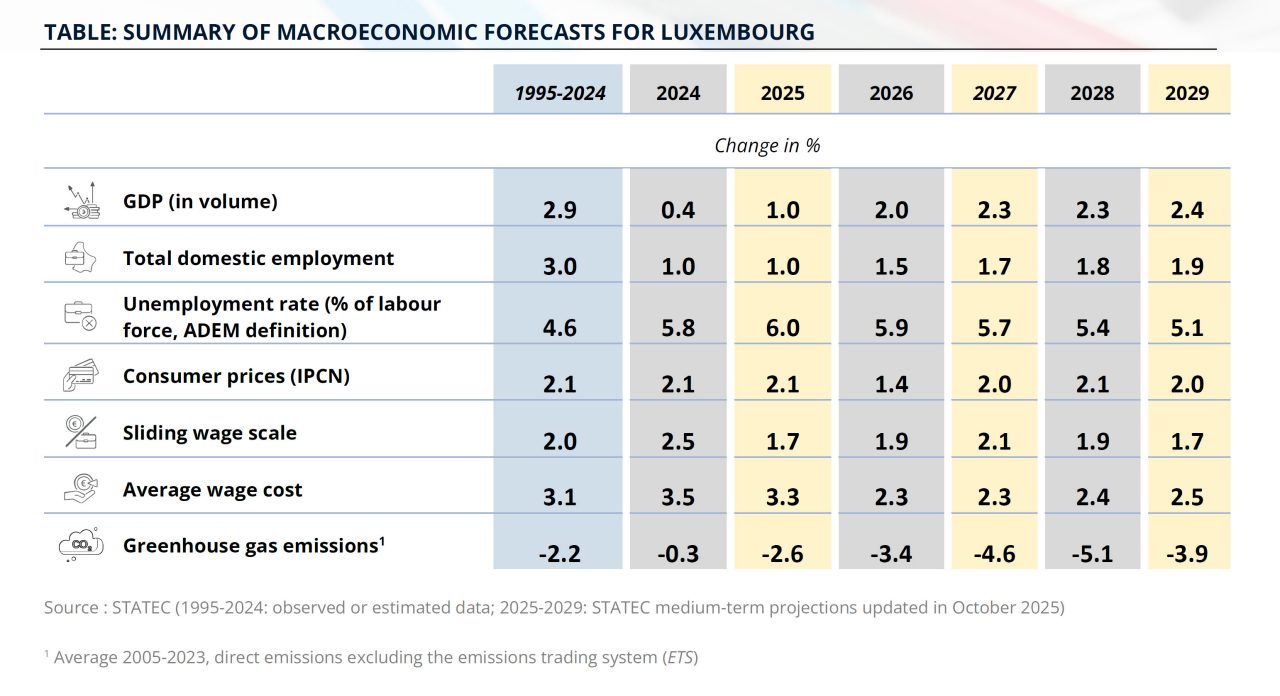

Luxembourg’s economy is gradually recovering, with GDP growth estimated at +1% in 2025. From 2026 onwards, this dynamic is expected to gradually strengthen, reaching around 2.5% by 2029. However, as for employment, the medium-term economic growth outlook is less favourable than in the previous version of the projections (published in September 2024). Employment growth would struggle to reach 2%, while the unemployment rate would only decline significantly from 2027 onwards, against a backdrop of slowing growth of the labour force. Inflation, meanwhile, is expected to fall rapidly, despite a slight rebound in 2025, linked in particular to the partial lifting of tariff caps on energy prices.

1. International context: forecasts

The trade agreement between the European Union and the United States, announced on 27 July, has helped to alleviate some economic uncertainties, particularly the risk of an escalation into a trade war. It has thus brought an element of stability to the forecasts published in Note de Conjoncture (NDC) 1-25. Despite this progress, the international context remains marked by strong tensions, both commercially and geopolitically.

STATEC's forecasts for Luxembourg's 2026 draft budget act are based on the international assumptions used in Note de Conjoncture 1-25. These forecasts were updated in August (with regard to inflation/wages) following the government's announcements concerning the stabilisation of electricity prices. The short-term effects of these announcements on economic activity, employment, public finances, etc. will be quantified by STATEC in Economic Outlook 2-25, which will be published in December.

The international assumptions of Oxford Economics (OE) predict GDP growth in the eurozone of 0.8% in 2025 and 1.0% in 2026. For 2025, the economic outlook for the eurozone could prove better than anticipated in April by OE, buoyed by more favourable economic momentum in the first two quarters, thanks in particular to strong exports and robust domestic consumption. Over the period 2026-2029, OE anticipates a gradual improvement in growth to 1.8% in 2028, followed by a slowdown to 1.5% in 2029.

Regarding consumer prices, the considered assumptions anticipate inflation in the euro area of 1.9% in 2025. In 2026, it is expected to be 1.5%. From 2027 onwards, annual consumer price inflation is expected to stabilise slightly above 2%, with an average of 2.2% over the period 2027-2029.

In terms of monetary policy, the forecasts assume an interest rate of 2.2% in 2025, which should stabilise at 2.1% from 2026 onwards. For the stock markets in Europe, which are particularly important for Luxembourg's financial activities, the Euro Stoxx is expected to grow by 4.6% in 2025, pause in 2026, and then resume an average pace of 2.7% over the period 2027-2029. However, market evolution indicates a better performance than expected in 2025. Indeed, since the beginning of the year, the index has risen by 8.6% compared to 2024.

Finally, forecasts for energy markets and exchange rate trends reflect a more cautious outlook for the global economy. The price of Brent crude is expected to fall below USD 70 per barrel from 2026 onwards, reflecting a deterioration in the short-term global outlook. Furthermore, in line with the Trump administration's economic policy, OE forecasts a relatively strong euro against the dollar, with an exchange rate of USD 1.13/EUR in 2025 and USD 1.16/EUR over the period 2026-2029. This appreciation of the euro would contribute to accentuating the decline in oil prices in Europe.

Risks

Uncertainty surrounding economic forecasts remains particularly high. At the time of the forecast, the main uncertainty was related to US customs duties, compounded by geopolitical tensions (which are still present). In this context, STATEC presented two alternative scenarios in its Note de Conjoncture 1-2025 to illustrate possible trajectories depending on international budgetary orientations.

The unfavourable scenario, entitled ‘Market correction’, assumes a loss of credibility for US fiscal policy, leading to a fall in stock market valuations and a rise in long-term interest rates from 2025 onwards. This financial shock would weigh heavily on global demand and GDP growth in the euro area, with an estimated negative gap of -0.8 percentage points in 2026 compared to the baseline scenario.

Conversely, the favourable scenario, ‘Government-led upturn’, is based on an intensification of stimulus measures, particularly in China and the European Union, as well as an increase in defence spending. This momentum would stimulate intra-European trade and boost growth, with an estimated positive impact of +0.2 percentage points in 2025 and +0.4 percentage points in 2026 compared to the baseline scenario.

2. Economic outlook for Luxembourg

The revised annual national accounts, published by STATEC on 5 September 2025, show a slight upward revision of cumulative growth over the period 2023-2024, by +0.2 percentage points. Growth for 2023 is now estimated at +0.1%, compared with -0.7% in previous estimates. However, the forecast for 2024, initially based on quarterly accounts, has been revised downwards to +0.4%, compared with +1.0% previously.

Activity

Once the forecasts were finalised, the revised quarterly national accounts for 2024 and the first quarter of 2025, as well as the first estimate for the second quarter, were published. They reveal, on one side, less dynamic GDP growth in the second half of 2024, but on the other side a better first quarter of 2025 than that considered in the NDC 1-25 (0.7% instead of -1% quarter-on-quarter). The growth carry-over for 2025 is therefore revised to 0.2% (compared with -0.5% previously).

The 1% growth forecast for 2025, as set out in NDC 1-25, could therefore be confirmed, provided that the second half of the year shows average quarterly growth of 1%.

For 2026, an improvement in the performance of the financial sector would allow to achieve GDP growth at 2.0%. Over the period 2027-2029, STATEC anticipates average growth of 2.4%, mainly driven by the private sector. Although this evolution is stronger than that forecast for 2025-2026, it represents a downward revision from previous projections, which predicted growth of 2.7% between 2025 and 2027.

This revision reflects the new trajectory of potential growth. For around six years, the potential GDP of Luxembourg’s economy has been regularly revised downwards. It is expected to be below 2% for the years 2025-2026, but should gradually adjust upwards to reach 2.1% at the end of the forecast period. The negative output gap is expected to close only very slowly over the forecast period.

Labour market

Since 2022, employment growth in Luxembourg has slowed significantly and stabilised at a historically low level between 2024 and 2025, particularly in the market sectors. Although the outlook improved slightly in industry and construction in the second quarter of 2025, employment growth for the year as a whole is expected to be moderate at 1%, driven mainly by the public sector. The unemployment rate is expected to remain high, at around 6%.

From 2026 onwards, in line with the expected economic recovery, STATEC anticipates a moderate strengthening of employment growth (+1.5%) accompanied by a slight decline in the unemployment rate (from 6% to 5.9%), with increased support from the market sector.

At the end of the forecast period, employment growth is expected to reach 1.9%, while the unemployment rate is expected to fall gradually to 5.1%.

Inflation/wages

The automatic indexation of wages in May 2025 contributed to a sharp rise in service prices. Inflation is expected to continue to rise in the coming months, driven by the strengthening of positive base effects related to energy at the end of the year. Higher-than-expected inflation in the second quarter of 2025 has led STATEC to raise its annual forecast to 2.1%, up from 1.9% previously.

In 2026, the expected fall in oil prices, combined with government measures on electricity tariffs (corresponding to a 9% reduction over the year as a whole), should lead to a decrease in energy prices of nearly 7%. This development would help bring overall inflation down to 1.4%. Services inflation is estimated at 2.3% in 2025 and 2.5% in 2026, while food inflation is expected to rise from 2.0% in 2025 to 2.3% in 2026. The next wage indexation is scheduled for the third quarter of 2026.

In the medium term, inflation is expected to stabilise at around 2%, in line with the trend observed in the eurozone. The spacing of index brackets would limit wage increases directly linked to price developments (as was the case in 2023 with three triggered index brackets), thereby reducing potential second-round effects on inflation.

In addition, the temporary reduction in employer contributions helped to contain compensation per employee growth in 2024. However, their normalisation in 2025 is expected to support an increase, with an anticipated rise of 3.3% this year.

From 2026 onwards, compensation per employee is expected to grow at a more moderate pace of around +2.3% per year, before rising slightly to +2.5% at the end of the forecast period.

Fuel sales / CO2 emissions

CO₂ emissions have been falling for several years, mainly due to declining fuel sales. This trend has accelerated during recent crises (COVID-19, soaring energy prices) before easing slightly in 2023 and 2024.

After a 2% decrease in 2023 and 3% in 2024 (compared to an average annual decrease of 8% between 2019 and 2023), fuel sales are expected to decline further by 4% in 2025 and 5% in 2026. These forecasts are based on an unchanged policy assumption and take into account, in particular, the gradual increase of the CO₂ tax in Luxembourg. The transition to electric and hybrid vehicles is expected to accentuate this trend, also leading to a decline in tax revenues from fuel excise duties.

In this context, greenhouse gas emissions are expected to follow a similar trajectory, with an estimated decline of 2.6% in 2025 and 3.4% in 2026. However, the introduction of the ETS2 emissions trading system, scheduled for 2027, introduces uncertainties regarding the evolution of fossil fuel prices, both in Luxembourg and abroad, and therefore the future trajectory of CO₂ emissions.

Bureau de presse | Tél 247-88455 | press@statec.etat.lu

La reproduction totale ou partielle du présent bulletin d’information est autorisée à condition d’en citer la source.

Last update