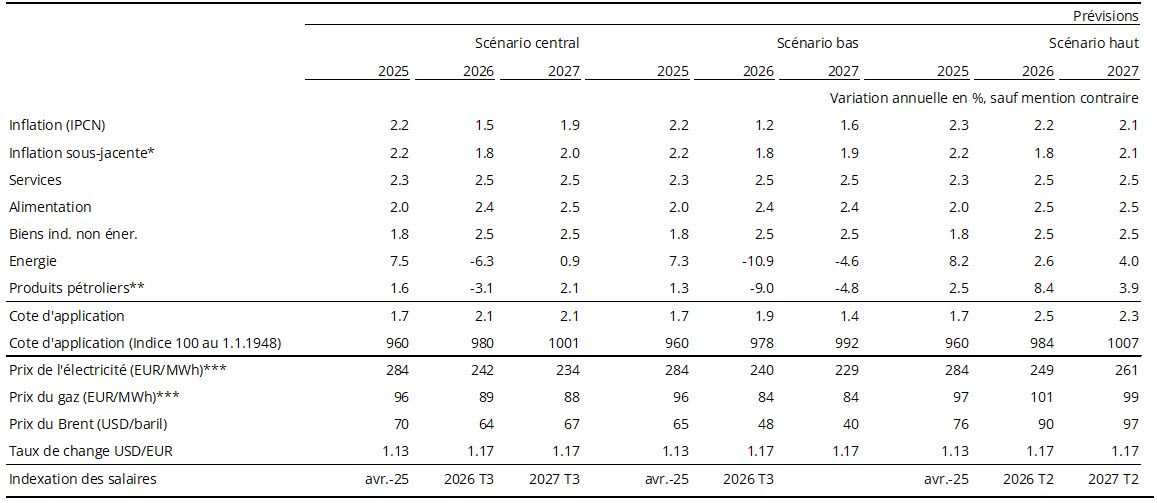

Inflation forecast : 2.2% for 2025 and 1.5% for 2026

Annual inflation in Luxembourg remained strong in the third quarter of 2025. STATEC now forecasts inflation of 2.2% in 2025, while in 2026 it is expected to fall to 1.5%, reflecting the expected stabilisation of energy prices, particularly electricity prices. A gradual return to an inflation rate close to the ECB's target is expected in 2027, with inflation estimated at 1.9%. The next indexation tranche is scheduled for the third quarter of 2026, followed by a new tranche in the third quarter of 2027.

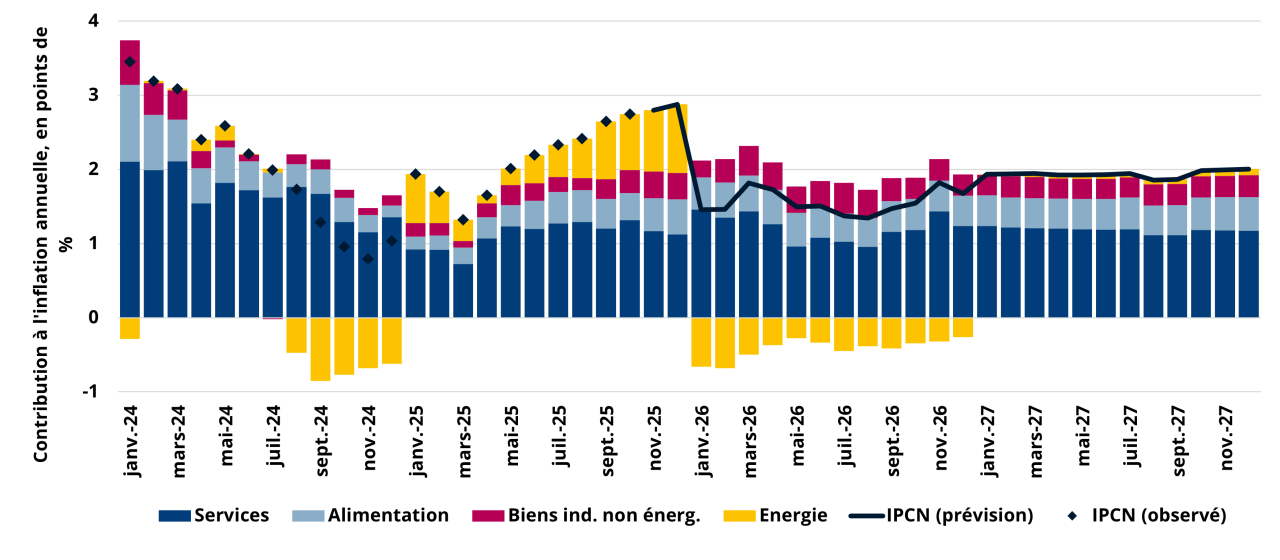

Annual inflation rate and contributions

Source: STATEC (forecasts as of 05/11/2025)

Over the past few months, inflation has been largely fuelled by positive base effects on energy prices, which had fallen a year earlier. It reached 2.7% year-on-year in October, with energy prices rising 11.7% over one year (compared with -10.8% a year ago). These prices thus accounted for more than a quarter of total inflation in October (0.8 percentage points, half of which was attributable to electricity, which had risen substantially in January).

Averaging around USD 65 per barrel in October, the price of Brent crude has recovered in recent months after peaking at USD 80 per barrel in June under the influence of geopolitical tensions in the Middle East. Despite a year-on-year decline of around 18% in the price of Brent crude in euros in October, annual inflation for petroleum products remains high in Luxembourg (at +7.0% year-on-year). This is because refining margins are significantly higher than last year[1], meaning that this decline has not been directly reflected in an equivalent decrease in fuel prices.

Annual inflation for services in Luxembourg also rose in October (+2.6% year-on-year), while pressure on food prices eased (+2.0% year-on-year in October, compared with +2.5% in August 2025). Annual core inflation[2] thus remained relatively stable at +2.5% in October (after +2.4% in September).

In the euro area, inflation fell slightly from 2.2% in September to 2.1% in October (according to a preliminary estimate), indicating a gradual convergence towards the ECB's 2% target. As in Luxembourg, inflation in services remains buoyant (+3.4% in October, compared with +3.2% in September), while food inflation is slowing (from 3.0% in September to 2.5% in October). On the other hand, energy prices continued to fall (-1.0% year-on-year in October), extending the persistent decline observed since March.

[1] In its latest report on the oil market, the International Energy Agency (IEA) confirms a general increase in refining margins. Indeed, refining margin indicators such as the Brent Crack Spread and the European Refining Margin (ERM) rose significantly in the third quarter of 2025. This reflects increased profitability, boosting the downstream results of refining companies.

[2] In Luxembourg, the underlying index is a sub-aggregate of the general price index excluding petroleum products and other products whose prices are directly linked to international markets. Electricity, on the other hand, is included in the index.

Inflation is expected to fall below 2% in the eurozone in 2026...

The main international institutions are consolidating their inflation forecasts for the eurozone at around 2.1% in 2025. For 2026, inflation is expected to range from 1.5% (Oxford Economics) to 2% (OECD), with forecasts factoring in the expected dissipation of energy shocks. For 2027, forecasts converge at 2%.

Oxford Economics' October 2025 projections, which feed into STATEC's current forecast, maintain the assumption of unchanged Brent prices at USD 70/barrel in 2025 and USD 64/barrel in 2026. However, the price of oil could fall faster than anticipated, as the current context points to a global supply glut[1]. Furthermore, reflecting the Trump administration's economic policy, Oxford Economics forecasts a continued appreciation of the euro against the US dollar, from USD 1.13/EUR in 2025 to USD 1.17/EUR in 2026 (compared with USD 1.16/EUR previously). This appreciation would contribute to a decline in oil prices in Europe in 2026. They would remain moderate throughout 2027, with Brent crude at USD 67 per barrel (EUR 57).

[1] The US Energy Information Administration (EIA) even predicts that the price of Brent will fall to an average of USD 52 per barrel in 2026.

…as well as in Luxembourg

Inflation in Luxembourg is expected to rise in the last two months of the year, reflecting the strengthening of positive base effects on energy. The smaller-than-expected decline in fuel prices in the third quarter of 2025 has led STATEC to revise its inflation forecast for this year to 2.2% and to 1.5% in 2026[1] (compared with 2.1% and 1.4% previously).

The price of electricity in 2026 is expected to fall by 15% (compared with -9% previously), reflecting the state contribution[2] to electricity network usage tariffs. In addition, anticipated declines in gas and Brent prices (by 7% and 8% respectively in 2026) are expected to push energy inflation down to -6.3% in 2026. Inflation in services is expected to be 2.3% in 2025 and 2.5% in 2026, while food inflation is expected to be 2.0% in 2025 before rising to 2.4% in 2026. Assuming that government measures are extended[3] until 2027 and that the general economic situation gradually improves in Luxembourg and the euro area, inflation is expected to be close to the 2% target in 2027, with annual inflation estimated at 1.9%.

According to these forecasts (which constitute STATEC's central scenario), the next wage indexation would apply in the third quarter of 2026, with the next tranche in the third quarter of 2027.

[1] Without measures on electricity prices, inflation for 2026 would be +0.3 percentage points higher, at 1.9% – the level forecast by STATEC in its Economic Note 1-2025 published last June.

[2] The measures include a state contribution of €150 million to network usage costs and a contribution of €120 million to the compensation mechanism system for 2026.

[3] The government's contribution of €150 million is also included in the official multi-year budget for 2027, but the exact effects on 2027 pricing for electricity network usage can only be assessed next year, once the regulatory procedure for determining tariffs for 2027 has been completed.

Forecasts based on alternative energy price assumptions

Source: STATEC (forecasts as of 05/11/2025)

* In Luxembourg, core inflation includes the price of electricity.

** These forecasts include a CO2 tax increase of EUR 5/tCO2e in 2026.

*** Average prices including VAT for a residential customer in Luxembourg with an annual consumption of 2,426 m3 of gas and 3,901 kWh of electricity. These prices are calculated assuming i) for gas: network usage tariffs increasing in 2026 at the same rate as in 2025, ii) based on assumptions by the Ministry of Economy, for electricity: from 2026, a return of the contribution to the compensation mechanism to EUR 0/kWh and a 35% reduction in network usage tariffs in 2026 compared to 2025.

Two alternative scenarios for energy prices

Two alternative scenarios have been established based on historical deviations in the electricity, gas and Brent crude oil markets (the latter affecting fuel and heating oil prices). Taking into account the measures in place (and in particular an identical price in the different scenarios for electricity in 2025), the high and low scenarios for electricity only diverge for the years 2026 and 2027.

The high scenario assumes that the price of gas will increase in 2026 (+5%) and decrease in 2027 (-2%), that the price of Brent crude oil will rise in 2026 and 2027 (+19% and +9% respectively) and that the price of electricity will fall in 2026 (-12%) and rise in 2027 (+5%). The low scenario anticipates a decline in electricity prices comparable to the central scenario (-15% in 2026 and -4% in 2027) and a more pronounced decline in gas (-12% in 2026 and -0.2% in 2027) and Brent crude (-26% in 2026 and -16% in 2027).

In the high scenario, the next index-linked tranche would be paid as early as the second quarter of 2026, with a new tranche in the third quarter of 2027. The low scenario anticipates only one indexation, in the third quarter of 2026.

Press office| Tél 247-88455 | press@statec.etat.lu

This publication was produced by Jill Schaul and Gabriel Gomes.

STATEC would like to thank all contributors who helped make this publication possible.

The total or partial reproduction of this publication is authorised provided that the source is acknowledged.

Last update