Conjoncture Flash November 2024: A deceptive recovery in eurozone activity?

Eurozone GDP grew strongly in the third quarter, but this was partly due to technical or non-recurring factors. As the year draws to a close, the economic environment in Europe is unlikely to bring much festive cheer and Luxembourg’s economy will have to come to terms with this.

In Q3 2024, eurozone GDP rose by 0.4% quarter-on-quarter. This figure was better than expected as economists had forecast growth of 0.2% given Q3 business surveys showed activity in services and industry losing momentum.

This increase in eurozone growth in Q3 (following a +0.2% rise in Q2) was caused by various factors. In particular, the data from Ireland (+2.0% over a quarter in Q3, after declining by 1.0% in Q2), where GDP growth is extremely volatile as it is largely influenced by income transfers from multinational companies. Excluding Ireland, eurozone growth was just 0.3% in Q3. Germany saw its GDP rise by 0.2%, whereas forecasters had feared the economy would enter a technical recession[1], due in particular to the negative signals emanating from German manufacturers in Q3 business surveys. This recovery, driven mainly by public and private consumer spending, nonetheless comes on the back of data that has been significantly revised to the downside for the previous quarter (for Q2, GDP growth has been revised from -0.1% initially to -0.3% now). The Paris Summer Olympics provided a major boost to economic growth in France, contributing more than half of the +0.4% recorded in Q3 (according to INSEE estimates). The impact of this event boosted confidence in France's services sector over the summer, but sentiment among French businesses turned very gloomy as autumn started, particularly in industry and construction. In the eurozone's two largest economies, the situation remains lacklustre on balance, while in Italy - the third largest economy in the eurozone - activity stagnated in Q3 (after +0.3% in Q1 and +0.2% in Q2).

As in previous quarters, Spain significantly outperformed the European average, with GDP up by 0.8% over the quarter. The Iberian economy continues to benefit from rising tourist numbers and relatively dynamic household consumption, against a backdrop of buoyant employment, largely supported by immigration. Since the start of 2024, Spain has contributed a third of the increase in activity recorded in the eurozone - even though it only accounts for around 10% of its GDP. The Netherlands also saw a significant rise in activity over the last two quarters (+1.1% in Q2 and +0.8% in Q3). However, the October surveys delivered more negative signals for these two countries[2]. Ultimately, growth for the eurozone as a whole is expected to settle at around +0.2% in the final quarter (according to forecasts by Oxford Economics and the European Commission).

The November PMI survey confirms the worsening trend in the eurozone, with the activity index for services joining the one for industry in the contraction zone.

Contributions to the quarterly change in GDP in the eurozone

What about Luxembourg?

For Luxembourg, Q3 results for GDP and its components are not yet known (they will be available on 6 December). The signals provided by the business surveys of companies in Luxembourg over this period are, on the whole, less favourable than in Q2 (with the exception of construction[3]), but the high volatility of the corresponding monthly data makes this finding uncertain (the response rate to the surveys was also relatively low for services).

Trends in production data in non-financial services (sales in real terms), available up to August, are fairly mixed. They are more favourable[4] in hotels and restaurants, information and communication services, real estate activities and business support activities, but lower in transport and professional, scientific and technical activities. In terms of financial activities, Q3 saw lending to households continue its recovery (business lending remains sluggish), while investment fund assets rose (modestly) only as a result of price effects (see below).

[1] A so-called "technical" recession is defined as a fall in GDP over at least two consecutive quarters.

[2] In particular, confidence of manufacturers in Spain and the Netherlands plummeted in October (to an 11-month low in Spain and a 7-month low in the Netherlands).

[3] The confidence indicator for construction contractors rose slightly in Q3, although it remains at a historically low level.

[4] Compared with Q2 results.

International

Household savings rate

Source: Eurostat

Savings remain high in the eurozone

In the eurozone, the household savings rate is on the rise again and is diverging from its long-term average since mid-2022, reaching 15.6% of household disposable income in Q2 2024 (compared with an average of 13% before the health crisis). Soaring inflation and tighter monetary conditions in 2022 and 2023 have limited household consumption, although real disposable income has been rising since the beginning of 2023. Over the first half of 2024, real disposable income per capita rose more than real consumption (+0.4% and +0.1% respectively over one quarter in Q2, after +1.1% and +0.4% in Q1). The household investment rate has also been falling since mid-2022, dropping from 10.3% of disposable income to 9.2% in Q2 2024.

The household saving rate is on the rise in most eurozone Member States. Among the countries with the highest rates are Germany (20% in Q2 2024, compared with 18% in 2019), Austria (19%, compared with 13% in 2019) and France (18%, compared with 15% in 2019). Spain has one of the lowest savings rates in the eurozone, but one of the strongest growth rates (rising from 9% in 2019 to 13% in Q2 2024).

Activity

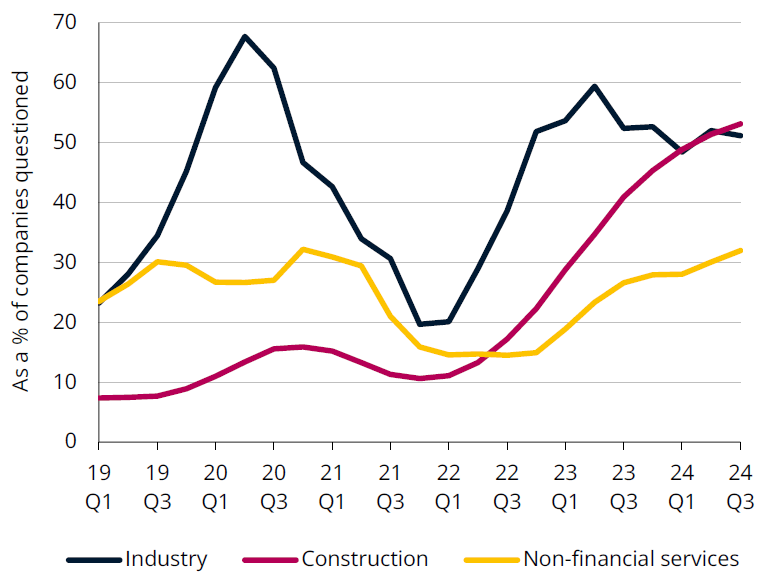

Percentage of companies reporting insufficient demand

Source: STATEC (business surveys - three-quarter centred moving averages)

Lacklustre demand

A large number of Luxembourg companies are still reporting lacklustre demand as 2024 draws to a close. This is particularly the case in industry and construction, where just over half of the companies surveyed voiced concerns. However, October surveys show that this proportion is no longer increasing as we enter Q4. In the services sector, around a third of companies reported weak demand, twice as many as in 2022.

Recruitment difficulties are still one of the factors weighing on companies. Although they have fallen sharply since mid-2022 - in line with the slowdown in employment - they remain significant. Over the first three quarters of 2024 approximately 40% of construction contractors are still complaining about this issue (despite the significant fall in activity and employment in this sector, indicating a marked mismatch between the profiles available and those sought). This proportion rises to 20% in industry and 15% in services.

Financial difficulties have been less prevalent in industry and construction in recent quarters, but they are affecting a growing proportion of service companies (around 15%, compared with barely 10% in 2023).

Real estate

Source: Eurostat

Sales prices of housing

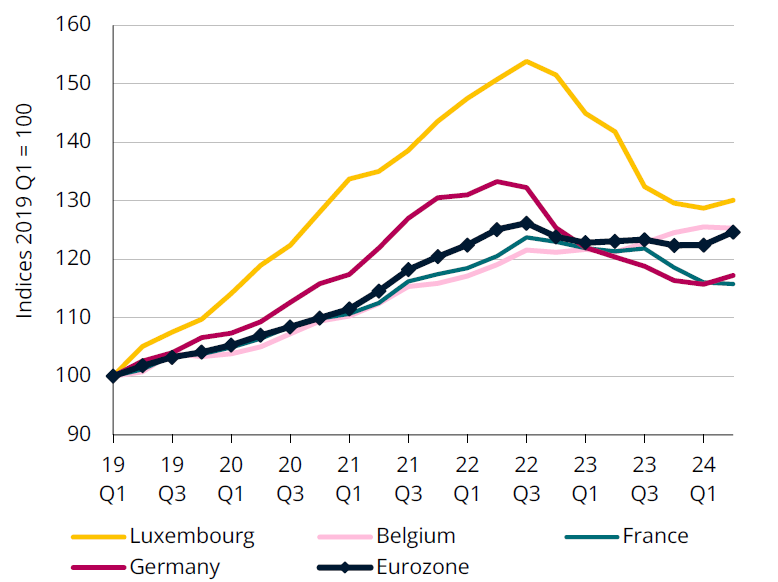

Are property prices on the rise again?

The fall in house prices that began in the eurozone at the end of 2022 seems to have come to an end. This decrease occurred against a backdrop of rising interest rates aimed at combating high inflation. The gradual easing of rates (with the ECB making its initial cut in June and the most recent in October) seems to have favoured the current turnaround.

In Luxembourg, after six consecutive quarters of decline, housing prices rose again in Q2 of 2024 (+1% over a quarter, see September Flash). Like in the Grand Duchy, housing prices rose in the eurozone (+1.8%) and in Germany (+1.3%). France is one of the only European countries to record a fall in housing prices in Q2 2024 (albeit much less pronounced than in previous quarters). This is also the case in Belgium, where the situation is however very different, as it has not known a downward trend in property prices. Less than half of European countries, mainly in Western and Northern Europe, experienced prolonged falls (of three consecutive quarters or more). In most of these countries, current house prices are still well below the peaks reached in 2022.

Financial sector

Net assets of Luxembourg undertakings for collective investment

Source: CSSF (end-of-quarter figures)

Investment funds witness slow down

In Q3, growth in the net assets of undertakings for collective investment (UCIs) in Luxembourg fell to +1.4% over the quarter (after +3.8% and +1.8% in Q1 and Q2 respectively). The rise in assets in Q3 was mainly due to valuations linked to the financial markets, particularly on fixed-income assets (bond and money markets, thanks to the cut in key interest rates) and on Asian equities owing to the stimulus plan announced in China in September. Net asset issuance fell in September, after four positive months. Most fund categories recorded negative capital investment in September, with the largest outflows from Latin American and Eastern European equities and global market bonds.

Fixed-income assets should continue to appreciate in Q4, driven by lower interest rates. On the equity markets, data suggests that valuations of European, Japanese and Chinese stocks are falling, while US equities are rising as a result of the presidential election.

Inflation

Services inflation

Source: STATEC

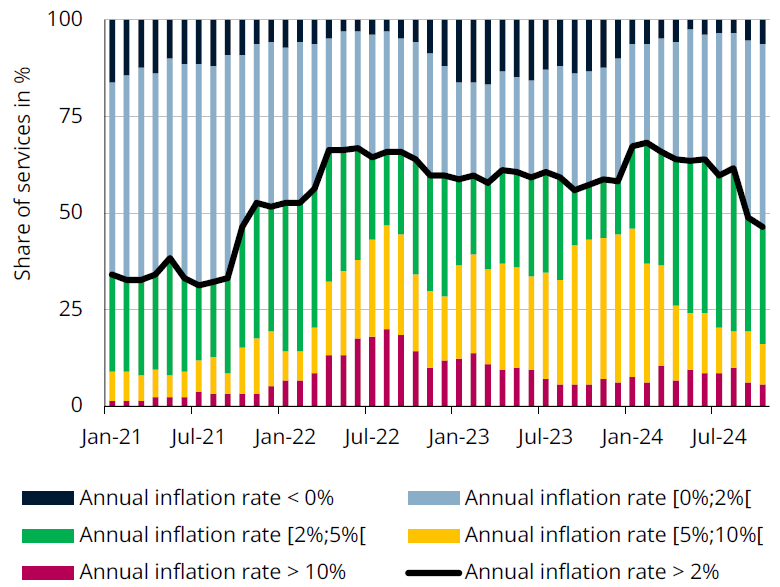

Less pressure on service prices

In October 2024, annual inflation in Luxembourg reached its lowest level since the beginning of 2021, at just 1.0%. The fall in oil prices was a major factor in pulling inflation down (contributing -0.8 percentage points to overall inflation in October, compared with +0.2 percentage points in April and May). The prices of services, largely stimulated in Luxembourg by the three successive index brackets in 2023, have also seen a marked slowdown in recent months (their contribution falling from 1.8 points in August to 1.3 points in October). Luxembourg and France (+2.9% year-on-year) both have the lowest inflation in services in the eurozone in October 2024 (compared with 4.0% in the eurozone, 4.8% in Germany, 3.9% in Belgium and 5.1% in the Netherlands).

The weak growth in services in Luxembourg in October was largely due to package holidays and crèches and day-care centres for children, two highly volatile items since 2022 (change in methodology for holidays and removal of the weekly ceiling of EUR 100 per child per week for childcare costs during holiday periods) and highly weighted in the price index. However, the proportion of services with inflation above 2% has also fallen considerably, to less than 50% since September.

Labour market

Unemployment rate

Sources: IGSS, ADEM, STATEC (seasonally adjusted data)

Contrasting trends in unemployment in the eurozone

Unemployment in the eurozone has continued to fall in recent months, reaching a new all-time low of 6.3% of the labour force in August and September (compared with 6.5% at the start of the year). This favourable trend continues to be driven by the steady falls seen in Italy (6.1% in September following 7.1% in Q1), Spain (11.2% following 11.8%) and Greece (9.3% following 11.0%). In half the Member States (including Luxembourg), unemployment is tending to increase. The slight rise in unemployment since the spring of 2023 in the two heavyweights, Germany (3.5% in September after a low of 2.9%) and France (7.6% following 7.1%), is putting the brakes on the fall recorded across the eurozone.

The deterioration in the labour market in these two countries is also reflected in the employment figures for Q3, which show the first slight fall in headcount since the COVID crisis. Employment for the eurozone as a whole (as in Luxembourg) has strengthened very modestly, from +0.15% in Q2 to +0.18% in Q3. According to the European Commission's autumn forecasts, employment in the eurozone is set to slow further in 2025 (+0.6% for 2025 after +0.9% for 2024 and +1.4% in 2023). This would stabilise unemployment in the eurozone at its current level (6.3% forecast for 2025).

Energy

Gas stock level in Europe

Source: Macrobond (weekly data)

Gas storage well stocked for winter

Since the outbreak of war in Ukraine, Europe has redoubled its efforts to diversify its gas supplies, relying in particular on increased use of liquefied natural gas (LNG). Since the end of 2021, the EU has increased its regasification capacity by around 60 billion cubic metres per year (+40%). However, LNG imports peaked in 2023, before declining by 20% in the first three quarters of 2024. This fall can be explained by a 3% fall in gas consumption in Europe over the same period, as well as by an increase in flows via gas pipelines, both from Norway and Russia.

In terms of the security of its gas supply, Europe is well prepared for the coming winter. Despite market prices rising throughout the year (although well below the levels witnessed during the crisis of 2022), the EU once again achieved its target of filling its gas stocks to over 90% by 1 November. However, stocks began to run down earlier than in the last two years, due to lower temperatures in late autumn.

Dashboard

Indicators

Last update