Note de conjoncture 2-24

Slow growthEven though Luxembourg’s economy returned to growth this year, the ongoing recovery remains lacklustre. It should strengthen in 2025 and 2026, driven by a combined improvement in domestic and foreign demand.

A low-consumption recovery in the eurozone

Global activity is expected to grow by around 3% per year between 2024 and 2026. A slowdown, taking the form of a soft landing, is foreseen in the United States and China over this period, although major downside risks in these two countries could lead to a stronger slowdown. The eurozone, as a whole, should experience a strengthening in growth until 2026, thus continuing the upturn in momentum observed this year. However, this recovery is very uneven across the different Member States, and appears to be running out of steam as 2024 draws to a close.

Despite the fall in inflation and the rise in real wages, European household consumption continues to be held back by a level of savings that not only remains very high (compared to pre-pandemic levels), but has also been rising since mid-2022. A great deal of uncertainty remains regarding the future trajectory of inflation. If it were to rise again above the ECB's 2% target, the planned rate cuts would be reduced and/or postponed, which would have a negative impact on activity in the eurozone.

Moderate growth in Luxembourg in 2024, but it should increase thereafter

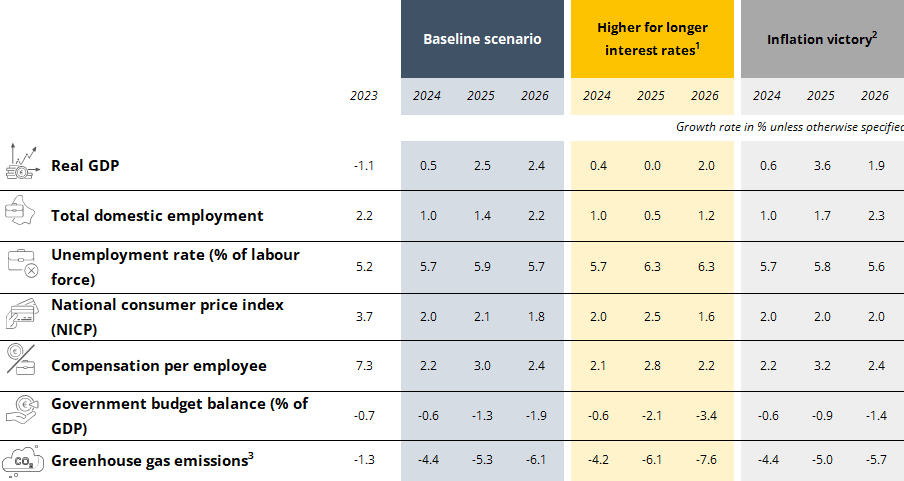

After a contraction in real GDP in 2023, Luxembourg’s economy has returned to growth. However, the upturn in activity has been sluggish and unevenly spread across the various sectors. Growth in 2024 will most likely be modest at 0.5%. The economy should return to a higher growth path thereafter, with +2.5% in 2025 and +2.4% in 2026. Under the impact of the interest rate cuts initiated in the eurozone, residential investment should gradually recover in 2025 and 2026. In addition, the expected upturn in economic activity in the eurozone should support economic growth in the Grand Duchy through stronger external demand. Household consumption should also improve, against a backdrop of a slight fall in savings.

Nevertheless, these forecasts are shrouded by risks. There is a great deal of uncertainty surrounding inflation trends and the subsequent reactions of monetary policy. On the negative side, higher-than-expected key interest rates in the eurozone could undermine the expected recovery in 2025. On the positive side, a faster-than-expected fall in interest rates would add around 1 percentage point to the growth forecast for next year.

Inflation normalises and indexation has weaker impact on wages

By the end of 2024, inflation in the eurozone will have reached the 2% target, while inflation in Luxembourg will be below 1%, notably due to low inflation in services. It should gradually increase over the course of 2025, mainly as a result of the easing of energy price caps. Nevertheless, over 2025 as a whole, inflation is expected to rise to 2.1%, very close to the 2.0% recorded in 2024. The next index bracket is forecast for Q2 2025.

Compensation per employee has also slowed considerably since 2023, rising by just 1.2% year-on-year in Q3 2024. The reduced impact of indexation, linked to the fall in inflation, and the temporary reduction in employers' contributions contributed most to this slowdown. After +2.2% for this year, compensation per employee growth is expected to rebound in 2025 (+3.0%) with the expiry of the measure on social contributions. Subsequently, it should settle at 2.4% in 2026.

Expected job creations will not enable a decline in the unemployment rate before 2026

In Luxembourg, employment has continued to slow, and is expected to grow by just 1.0% this year (on the back of +2.2% in 2023), a rate close to that forecast for the eurozone as a whole. For Luxembourg, this represents the lowest level of growth since 2009, while for the eurozone it is above the historical average.

The fall in employment in the construction sector continues to weigh heavily on Luxembourg's results, but it is in the process of moderating, and should have much less of an impact in 2025. The modest upturn in economic activity in general since the start of the year should also help to boost employment. STATEC forecasts growth of +1.4% for 2025 and +2.2% for 2026, which are still well below the average of the last twenty years (close to 3%).

There are notably uncertainties surrounding the anticipated recovery in cross-border employment, where the current slowdown may not only be cyclical but also structural in nature.

Unemployment in Luxembourg started taking a significant hit from the slowdown in activity in the spring of 2023, but its increase has slowed since the end of 2023. The unemployment rate is expected to rise to 5.7% of the labour force this year and increase slightly further to 5.9% next year, before falling back to 5.7% in 2026 as the labour market strengthens.

Towards a slowdown in public revenues and expenditure

STATEC forecasts a fall in public revenues between 2024 and 2026, owing to the adjustment of tax scales, a decline in fuel sales, a drop in excise duty on tobacco and subscription tax, and under the assumption that corporate tax balances return to normal.

Spending growth will also fall sharply in 2024 and continue at a more or less similar pace in 2025 and 2026. Items that have been boosted by crisis measures are likely to decline, pulling down overall expenditure. Growth in public sector employment is expected to slow, limiting growth in the wage bill. However, the ratio of public spending to GDP would reach historically high levels (almost 50% in 2026).

The public balance has been revised upwards in the recent past thanks to two exceptional effects: the recalculation of VAT receipts and the particularly high tax balances of some companies. Nevertheless, the future trend will remain downward, with the deficit deteriorating from -0.6% of GDP in 2024 to -1.9% in 2026.

Significant reduction in greenhouse gas emissions

Despite the continuing unrest in the Middle East, oil prices remain on a downward trend, due to a sharp increase in production capacity and lower-than-expected global demand. In Luxembourg, demand for petroleum products is falling, with STATEC anticipating a decline in sales of motor fuels and deliveries of heating oil of around 4% and 12% respectively in 2024, followed by further falls of 4.5% and 3.5% in 2025.

Conversely, gas and electricity consumption has recovered sharply from the low seen during the energy crisis in 2023, recording increases of 4% to 5% over the first ten months of 2024. Consumer prices for these two energy sources are set to rise from 1 January 2025, with the gradual scaling back of the tariff shields.

Given the downward trend in fossil fuel consumption in Luxembourg, STATEC expects greenhouse gas emissions in the Grand Duchy to fall by around 4.5% in 2024 and 5% in 2025. This favourable trend would place emissions below the trajectory set out in the integrated national energy and climate plan (PNEC).

Thematic studies in this Note

- Impact of economic policy measures on STATEC’s forecasts

- Evolution of purchasing power and saving rate by standard of living

Macroeconomic forecasts

- In this unfavorable scenario, inflation proves more stubborn than expected due to the rise in energy prices linked to concerns about the situation in the Middle East. Monetary policy is tightened again in the United States and key rate cuts are delayed in the euro zone. Credit conditions are tightening, which is weighing on the financial and real estate markets.

- In this favourable scenario, inflation is reduced more than expected and converges quickly towards the 2% target, encouraging central banks to considerably lower their key rates. This greater easing will further stimulate investments, the real estate market, consumption and financial markets..

- Trend 2005-2023.

Total or partial reproduction of this newsletter is authorized provided that the source is cited.

Last update