Conjoncture Flash February 2025: Two-speed recovery of services'confidence

The morale of service companies in Luxembourg has gained ground over recent months, following a decline in Q3 2024. However, this improvement in sentiment is not shared by all actors in the sector.

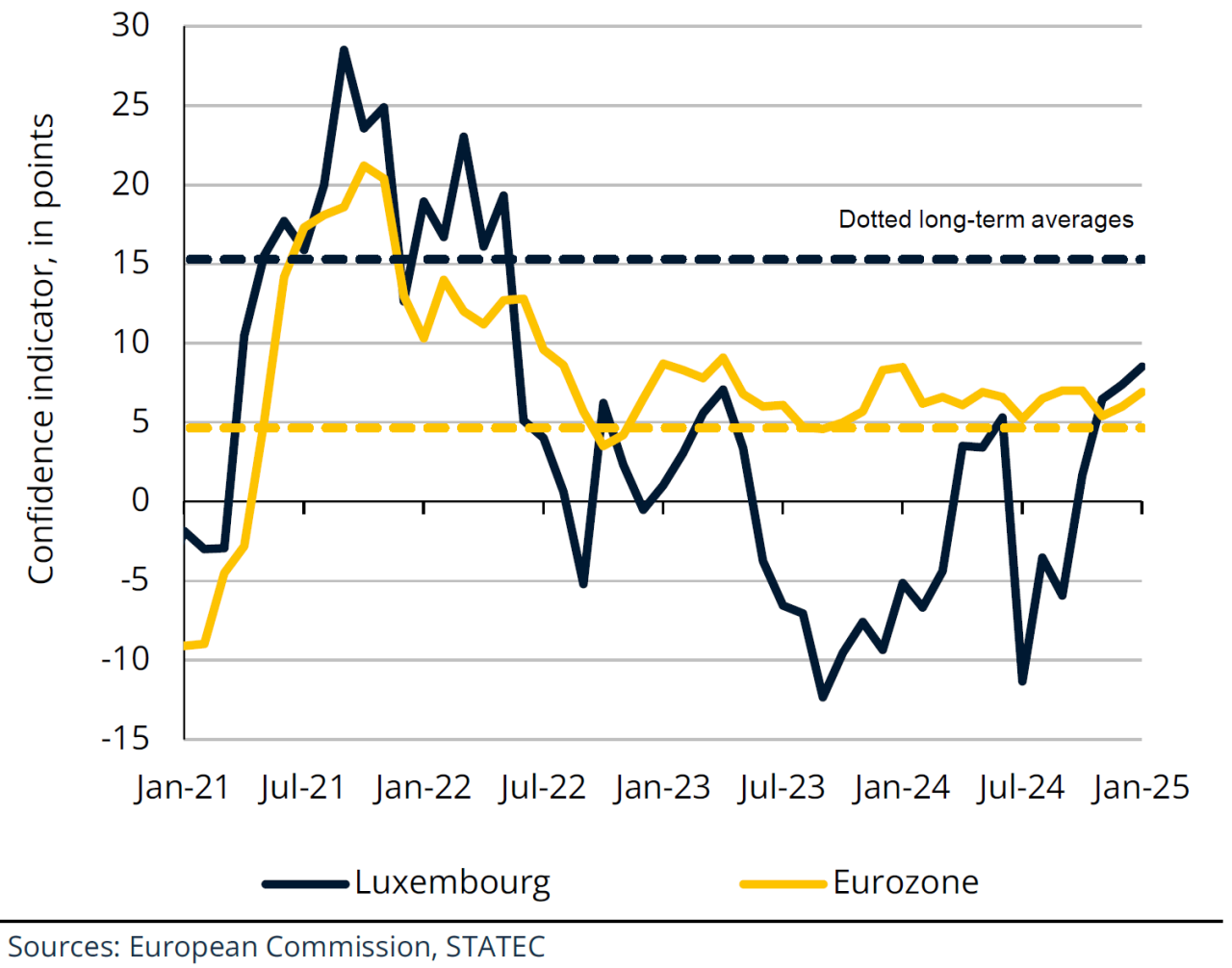

After falling sharply in Q3 last year, morale among service companies[1] in Luxembourg has since recovered. This trend was confirmed in the last survey in January. The confidence indicator[2] rose for the fourth consecutive month and reached a level not seen for the past two and a half years.

This recovery is evident in all three components of the indicator (evolution in the company's situation, recent demand and anticipated demand), particularly in legal and accounting activities, air transport, catering, postal and courier services, leasing and administrative and business support. However, no improvement has been observed for land transport companies, warehousing companies, housing, IT programming and consulting, or head office and management consultancy services. The upturn in morale in services in Luxembourg is thus not generalized for the moment, and the current level of confidence remains below its historic average. Other significant findings from the survey over the past few months include an improvement in employment trends (both recent and anticipated), and a fall in the proportion of companies pointing to financial constraints.

In the eurozone, confidence in services has fluctuated slightly above its long-term average since the start of 2024, without any clear direction. It rose marginally in December and January[3], mainly due to an improvement in results in Italy.

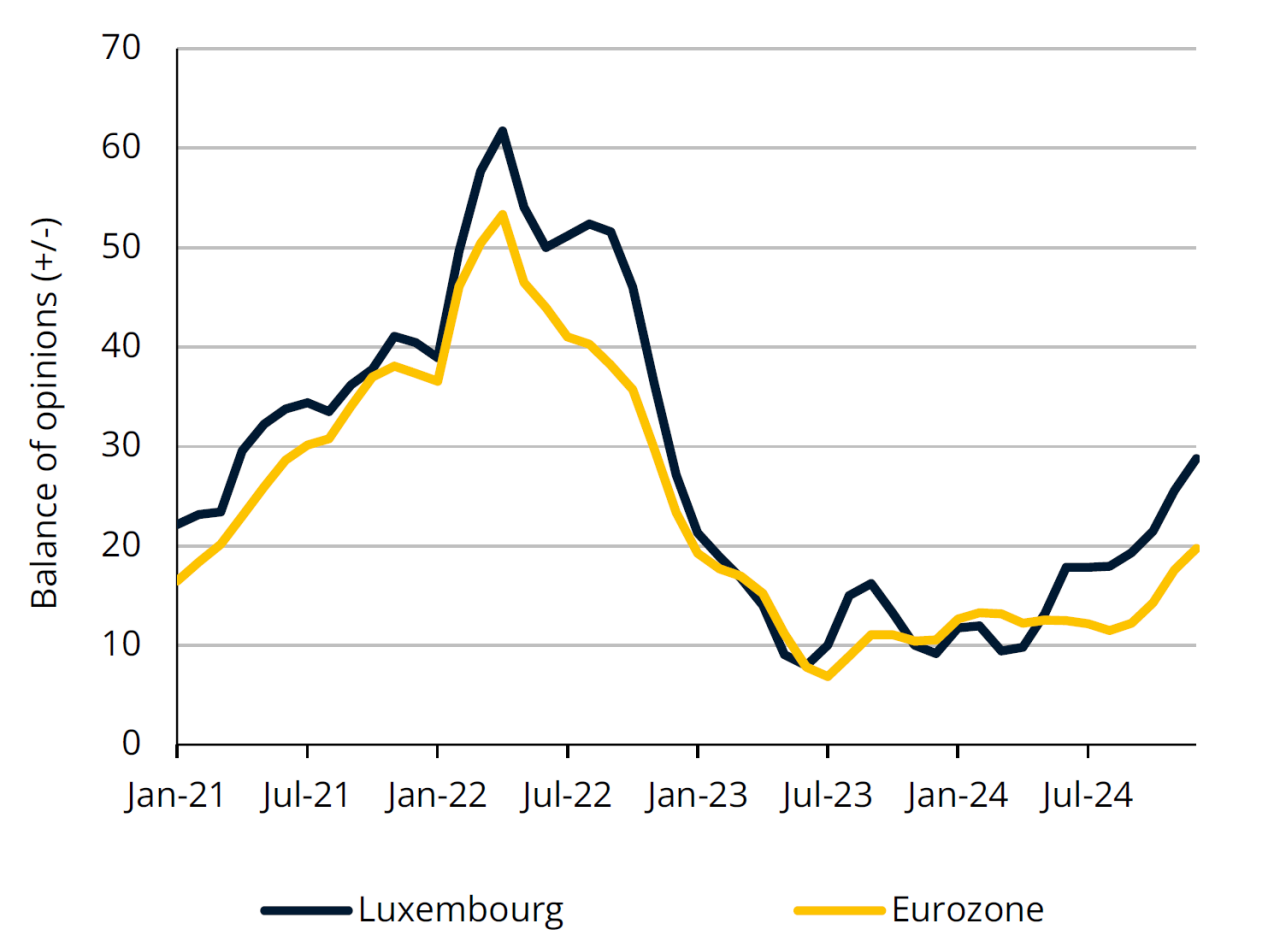

In the retail sector, which is the subject of a specific business survey, the trends noted in Luxembourg are fairly similar to those for other services: a relatively marked fall in confidence among retailers in Q3 2024, followed by a recovery. This recent improvement is reflected in the three components of the confidence indicator: sales trends (both recent and expected are on the rise) and inventory levels (which are down, which is positive from a cyclical perspective). However, this sentiment has not been accompanied by a more favourable employment outlook. In the eurozone, retail confidence has also been trending upwards since Q4, but this growing optimism is not widespread (this change has not been observed in the three countries bordering Luxembourg).

Confidence indicator in non-financial services

What about industry and construction?

Industrial companies in Luxembourg have experienced a minor upturn in their morale since mid-2023 (slightly bucking the trend in Europe, which remains on a downward spiral). However, the figures continue to fluctuate sharply from one month to the next. The general climate for industry in Europe remains gloomy, undermined by weak demand for investment and capital goods, high energy costs and the pressure of international competition (see January's Conjoncture flash).

Business confidence in Luxembourg's construction industry continues to drop, even though it has already been rising for several months across the eurozone. At the start of 2025, it reached a level not seen since the 2009 financial crisis. Around 60% of companies in the sector are currently reporting insufficient demand, in comparison to 10% at the start of 2022.

[1] Non-financial services (excluding retail).

[2] This confidence indicator is an arithmetic average of the balances of opinion relating to three questions in the monthly business survey: evolution in the company's situation over the last three months, evolution in demand over the last three months, and outlook for demand over the next three months.

[3] A similar trend has been observed in the PMI services activity indices for the eurozone over the same period.

International

Contributions to the quarterly change in GDP in the eurozone

Sources: Eurostat, STATEC calculations

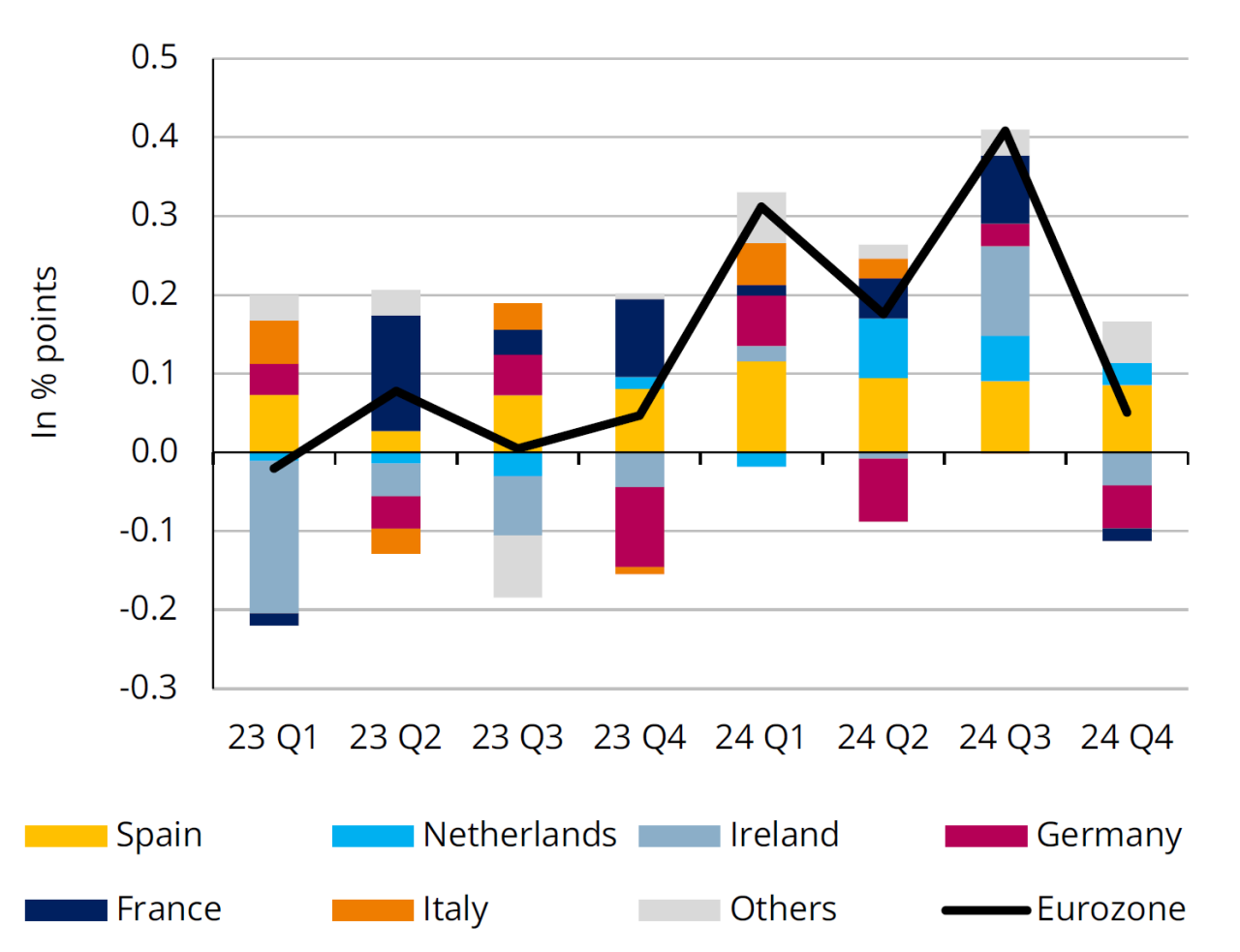

Another year of weak growth in the eurozone

In Q4 2024, eurozone GDP rose by 0.1% over one quarter. This figure, even though it was widely forecast, reveals a marked slowdown compared with the Q3 result (+0.4%). Q3 was characterised by one-off positive contributions from France (owing to the ‘Summer Olympics’ effect) and Ireland (whose GDP figures are extremely volatile). Spain has maintained its role as a driving force in Europe, with growth of 0.8% (the same figure as in the previous two quarters). Meanwhile, Germany is still lagging behind, with a decline of 0.2%. The European powerhouse has avoided a technical recession (two consecutive quarters of decline) but did not avoid a recession for 2024 as a whole (-0.2%), in similar fashion to 2023

(-0.1%).

The eurozone displayed weak growth of 0.7% in 2024 (after +0.5% in 2023). This figure is about half the average annual rate recorded over the last decade with the average for 2010-2019 at 1.4%. It will clearly be difficult to reach this level in 2025.

Financial sector

Rates on new loans in Luxembourg

Sources: BCL, BCE (seasonally adjusted data)

Interest rates continue to fall

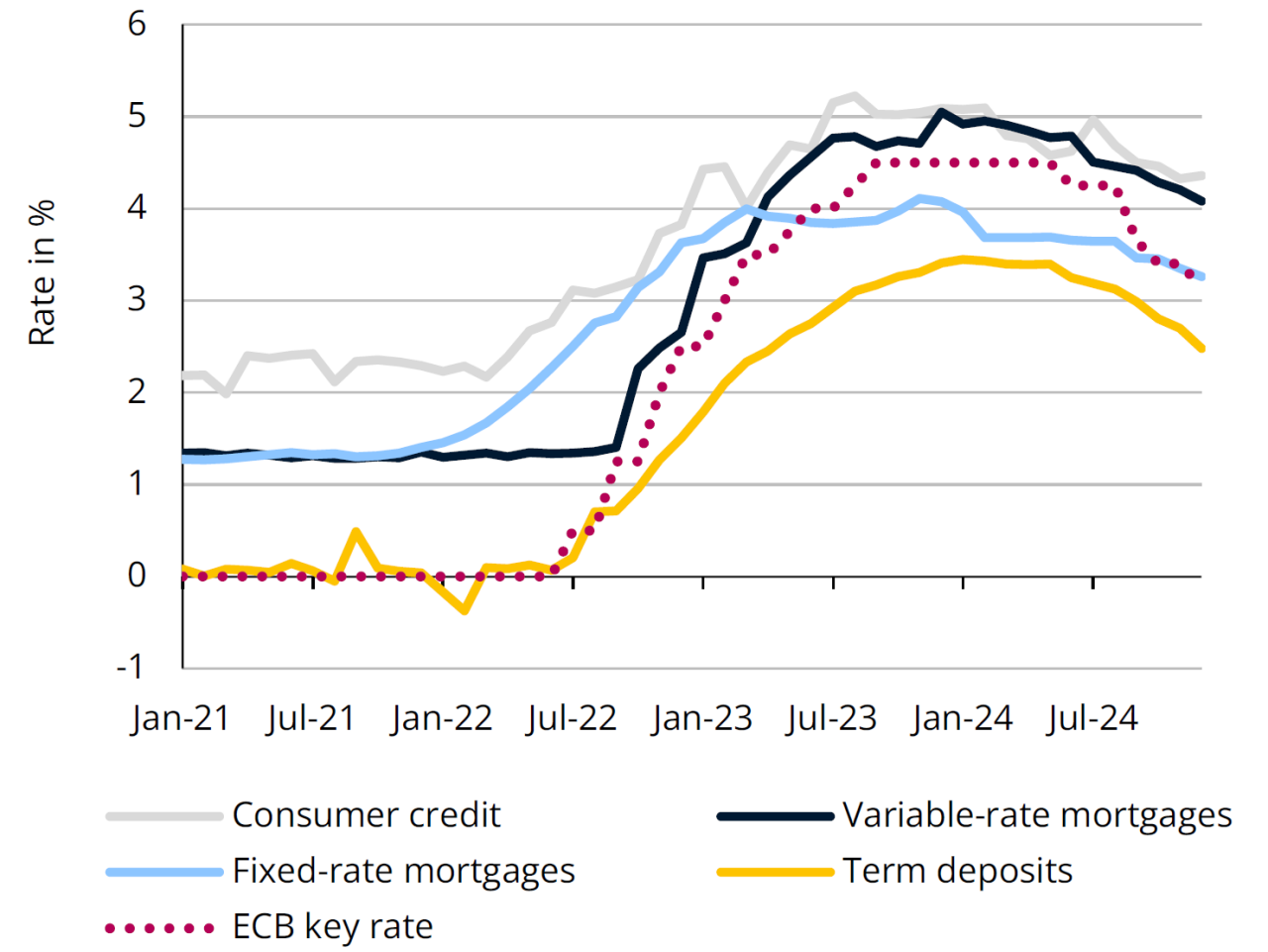

Interest rates on loans and deposits have been falling since the summer of 2024, after hitting record highs. In 2024, rates declined by approximately 1 percentage point due to the fall in inflation. This allowed the European Central Bank (ECB) to cut key rates on five separate occasions.

In December 2024, the average variable rate on mortgages in Luxembourg was 4.0%, well above the level for fixed-rate mortgages (3.3%), and well below the rate for consumer loans (4.7%). The interest rate for household deposits was 2.5%. The fall in interest rates, combined with rising consumer confidence and a better outlook on the real estate market, have driven demand for new fixed-rate mortgages in Luxembourg (up 25% in 2024), while variable-rate mortgages and consumer loans remain lacklustre. Household term deposits continued to rise (+21% year-on-year, following two years of strong growth).

Interest rates on loans continue to fall in Q1 2025 due to ECB’s cut on key rates (once at the end of January, another cut forecast for early March).

Inflation

Inflation expectations

Sources: Eurostat, STATEC, business surveys* (smoothed series)

*Consumers' expectations of price trends over the next 12 months

Consumers revise their inflation expectations upwards

Consumer inflation expectations for the next 12 months have risen sharply. In Luxembourg, the anticipation of the partial lifting of the price cap on 1 January 2025 has probably contributed to this change. In January 2025, annual inflation rose to 1.9% (it was 0.8% in November 2024), mainly due to the aforementioned effect (accounting for +1 percentage point).

In the eurozone, inflation is also on the rise at the start of 2025 (around 2.5% in December and January, after hitting 1.7% in September), primarily caused by a hike in energy prices (+0.8 percentage points over this period).

Sales price forecasts for the next three months are creeping upwards according to eurozone entrepreneurs. However, the trend for Luxembourg companies is less clear, with the exception of the retail sector, where price expectations are clearly rising over the same period, and the construction sector, where they are falling.

Labour market 1/2

Employment in the construction sector

Sources: IGSS, STATEC (seasonally adjusted data)

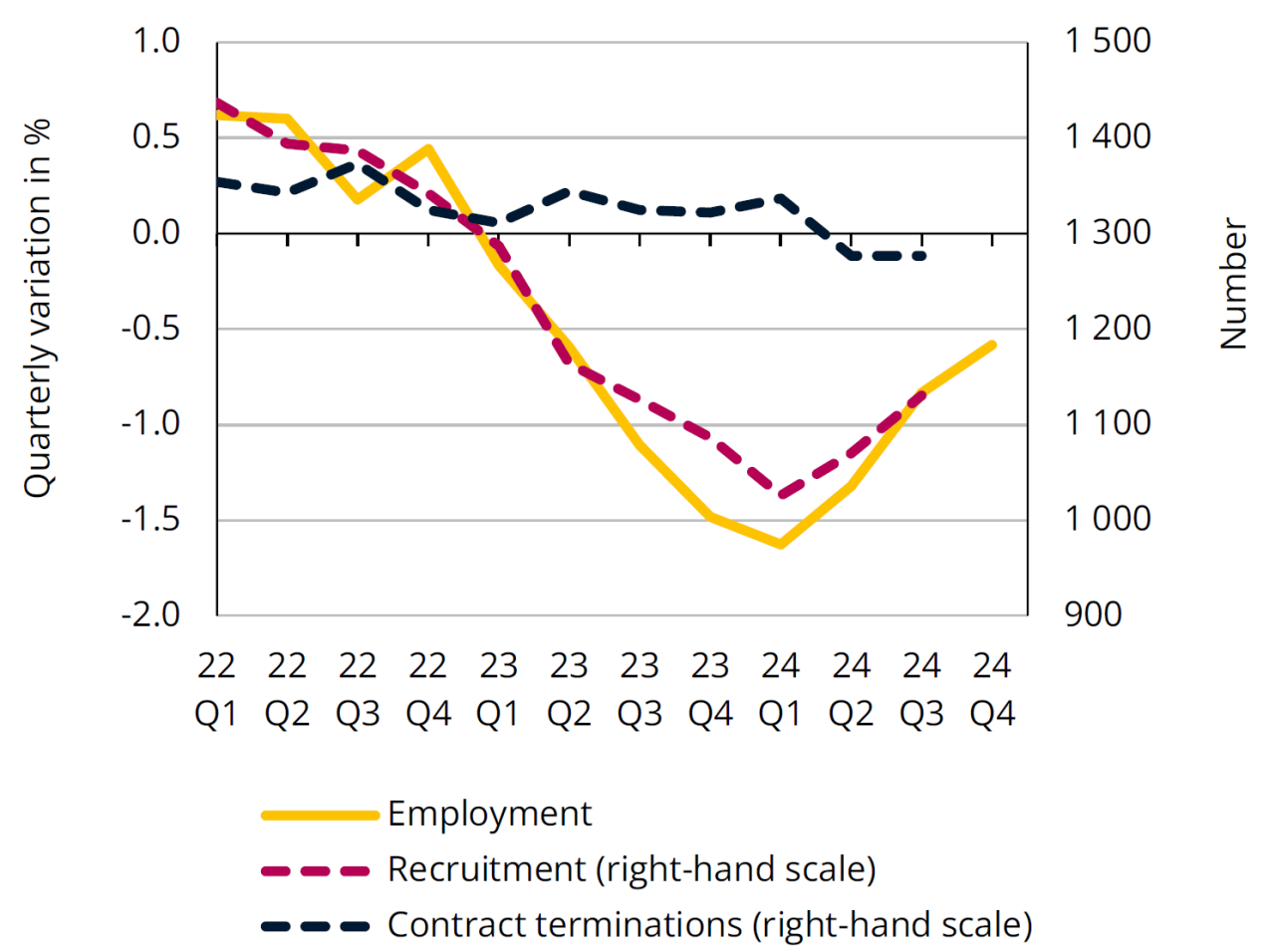

Recruitments on the rise in the construction industry

After falling by 1% in 2023, employment in the construction industry dropped by another 5% in 2024. This sector experienced the largest decline in employment in 2024, ahead of activities of households as employers (-2.2%), industry and real estate (-1% each). However, job losses in the construction sector are beginning to ease, passing from -1.6% over one quarter at the start of 2024 to -0.6% in Q4. This positive trend has been observed in specialised construction work and building construction.

Data on job flows (the most recent data is from Q3 2024), indicate that it is primarily in the field of recruitment that trends are becoming more favourable again. In Q2 2024, the number of persons hired in the construction industry increased for the first time since the start of 2022; this rise strengthened further in Q3. It is important to note that these increases do not correspond to a parallel movement in contract terminations, which on the contrary fell over these quarters; this reinforces the start of an upturn in the sector.

Labour market 2/2

Rate of job vacancies

Sources: ADEM, STATEC (seasonally adjusted figures)

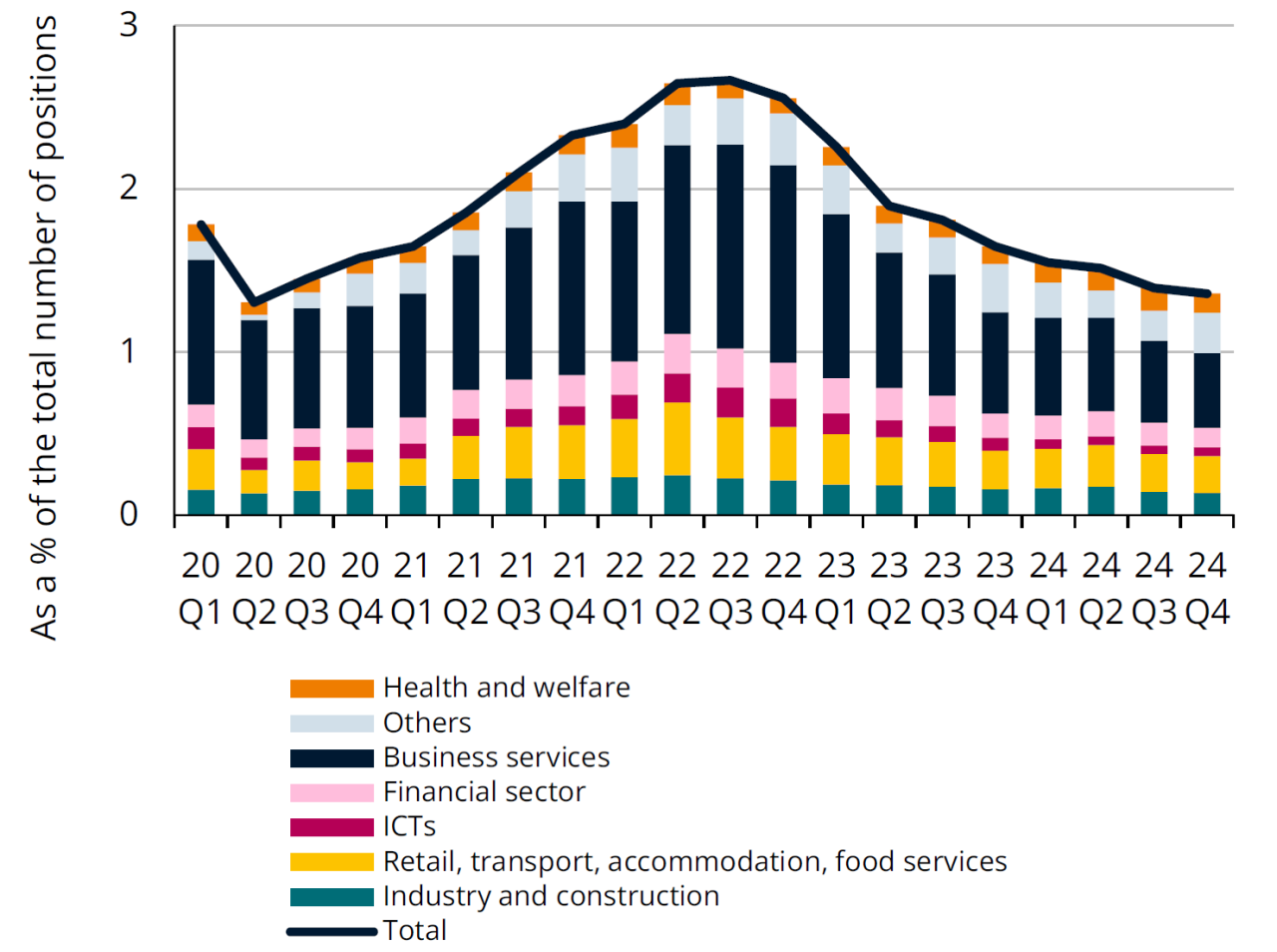

Is the job vacancy rate about to bottom out?

Since its peak in mid-2022, the job vacancy rate, which measures open positions (declared to ADEM) in relation to all open and occupied positions, has almost halved. It is mainly business services (in particular accounting activities and temporary employment agencies) that have contributed to this downward trend (with the rate falling from 7.0% in mid-2022 to 2.6% at the end of 2024), followed by information and communication technologies - ICTs (from 4.0% to 1.2%), the financial sector (from 2.2% to 1.1%) as well as accommodation and food service activities (from 3.3% to 1.4%). The trend is similar across the eurozone, where the job vacancy rate declined from 3.3% in Q2 2022 to 2.5% in Q3 2024, in line with the slowdown in employment observed since the end of 2021.

Even though job vacancies have fallen sharply in the Grand Duchy since September 2022, the drop has been much less pronounced in recent months. A stabilisation has been observed in several sectors, such as ICT (especially programming, consulting and other IT activities), business services, trade and transport. Employment rose particularly in the public sector and for accommodation and food service activities in 2024.

Energy

Market share of electric cars in Europe

Sources: Eurostat, ACEA

Electro-mobility stalls across Europe

The European car market remained relatively stable in 2024, with a 0.8% increase in new registrations, reaching a total of 10.6 million new cars. However, this level is still well below the pre-COVID level when over 13 million new registrations were recorded. The market share of electric vehicles fell by one percentage point to 13.6%. This decline is mainly due to Germany (Europe's largest car market) where electric car registrations have fallen by 27% compared to 2023. This fall is largely due to the removal of State subsidies in December 2023.

In Luxembourg, on the other hand, the number of electric cars on the roads has continued to grow, accounting for almost 30% of registrations in 2024, well above the European average. This increase was mainly driven by registrations made in the name of legal entities (companies and leasing companies). The share of the electric car market is similar in Belgium, with over 80% of registered electric cars belonging to companies. Of the countries close to Luxembourg, the Netherlands remains the leader of the pack with the largest market share of electric vehicles. However, with regard to future trends in the Netherlands, a sense of uncertainty reigns due to the reduction in subsidies scheduled for 2025.

Public finances

Change in revenue collected (excluding contributions)

Sources: Tax authorities, STATEC

*Energy and conjoncture Tax Credit

Public revenues boosted by one-off effects

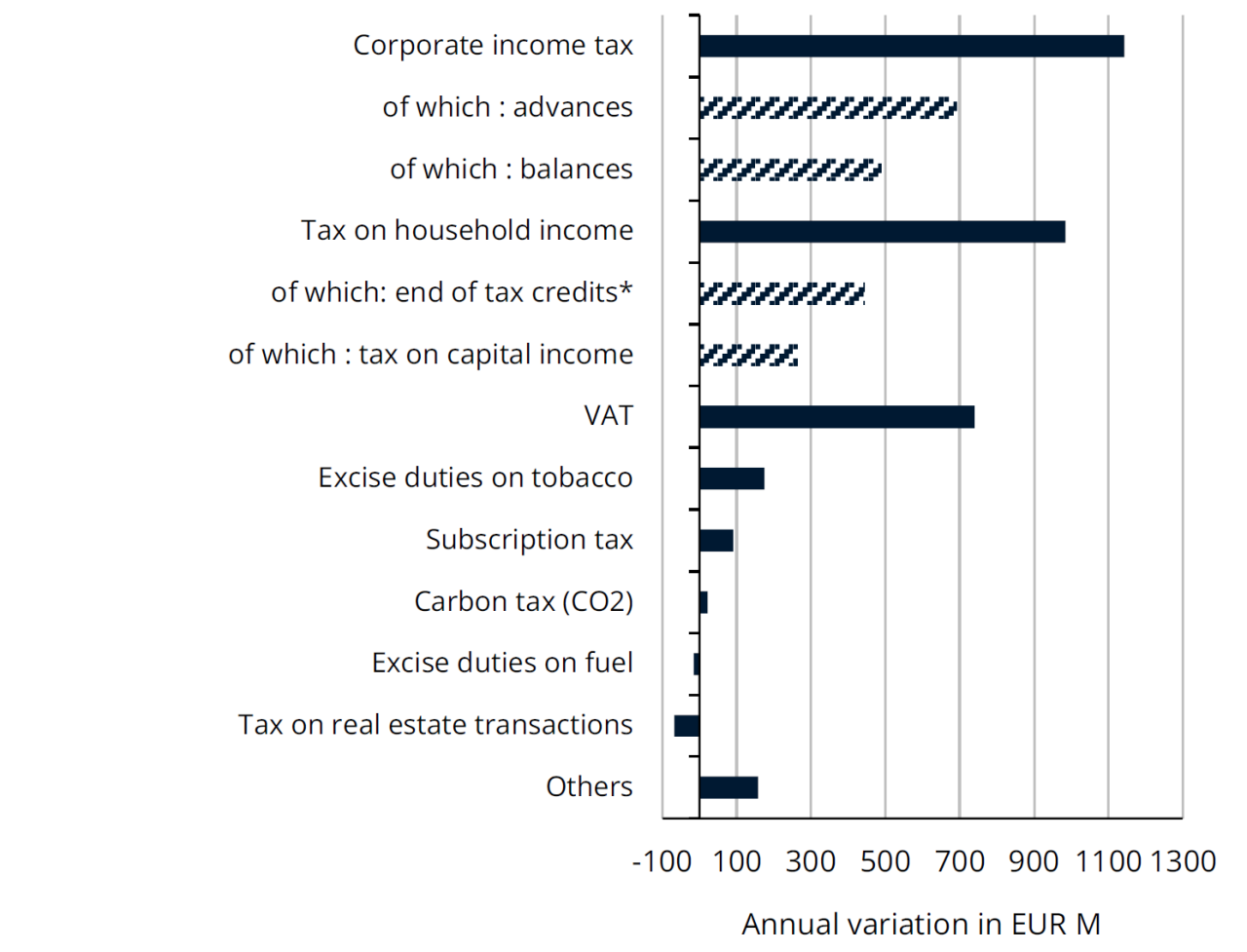

Revenue collected by the State in 2024 rose by 13.4% year-on-year (excluding social security contributions). This increase is due to a number of one-off effects: high tax balances refunded by some companies, the expiry of energy and conjoncture credits, and the increase in VAT rates (temporarily lowered in 2023). Corporate tax balances and tax credits contributed to approximately one-third of the increase in revenues collected in 2024.

Income from household capital and excise duties on tobacco also rose sharply, accounting for almost 15% of revenue growth. The fall in excise duty collected on fuel sales was offset by the rise in revenue from the carbon tax. This tax has been subject to a EUR 5 increase per year from 2022. It now stands at EUR 40 per tonne of CO2 in 2025. Revenues linked to the real estate transaction tax rose again in the 4th quarter of 2024, without however making up for the losses over the rest of the year.

In January, tax receipts rose by 12.9% year-on-year, primarily boosted again by the tax balances of a few isolated companies and by excise duties on tobacco, while VAT receipts and taxes on household income fell.

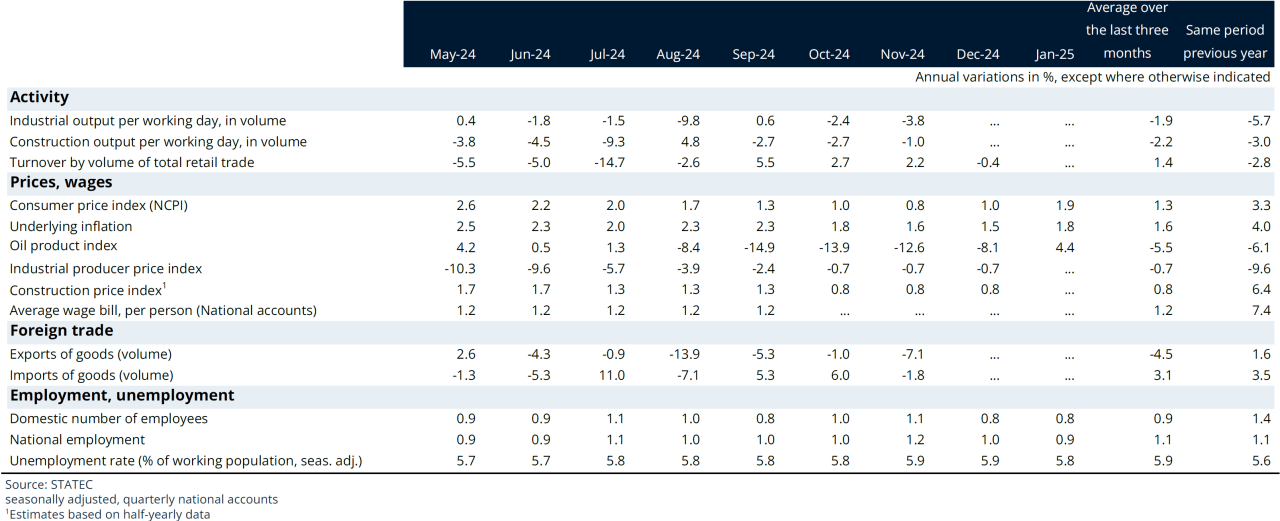

Dashboard

Indicators

Last update