Conjoncture Flash March 2025: US policy casts a cloud of uncertainty

Update of the Conjoncture flash on 1 April 2025 at 7:00 pm

(see bottom of page)*

The decisions taken by the new US administration, particularly with regard to raising tariffs, have added to the uncertainty surrounding the global economic outlook. Even though Luxembourg's exposure in terms of goods exported to the United States is relatively low, indirect effects linked to the deterioration in the international economic climate cannot be ruled out.

The Trump administration took office on 20 January. Since then, it has announced a series of reforms, some of which have already been implemented. In economic terms, the main change concerns the increase in US customs duties (tariffs), primarily against China and its North American neighbours (Canada and Mexico), but also against Europe and the rest of the world. In addition, certain products, notably steel and aluminium, are also subject to increases across the board. The stated aim is to reduce the US trade deficit, protect the US economy from unfair competition and encourage companies to produce more domestically. However, these protectionist measures generally lead to retaliatory measures of a similar nature from the countries targeted.

Several simulations and studies of the impact of these tariffs have been carried out recently[1], with assumptions that vary considerably due to the uncertainties surrounding their scale and scope. However, their conclusions converge, in line with the teachings of economic theory: this type of measure tends to weigh on world trade and economic activity, and to increase inflationary pressures. Moreover, the United States would be among the worst affected, alongside China, Mexico and Canada. Europe would be less affected, but some of its products would suffer from higher US tariffs (in particular steel, automobiles and chemicals, wines and spirits). In its latest forecasts[2], the OECD points to a less favourable general economic climate: "Global GDP growth is expected to moderate from 3.2% in 2024 to 3.1% in 2025 and 3.0% in 2026, with higher trade barriers in several G20 economies and increased policy uncertainty weighing on investment and household spending” . Other major risks stem from the direction taken by US international policy and, in particular, its desire to disengage from international institutions and agreements, breaking away from the multilateralism that previously prevailed. In Europe, this is reflected - among other issues - in a new geopolitical configuration concerning the future of Ukraine and the role of European defence[3].

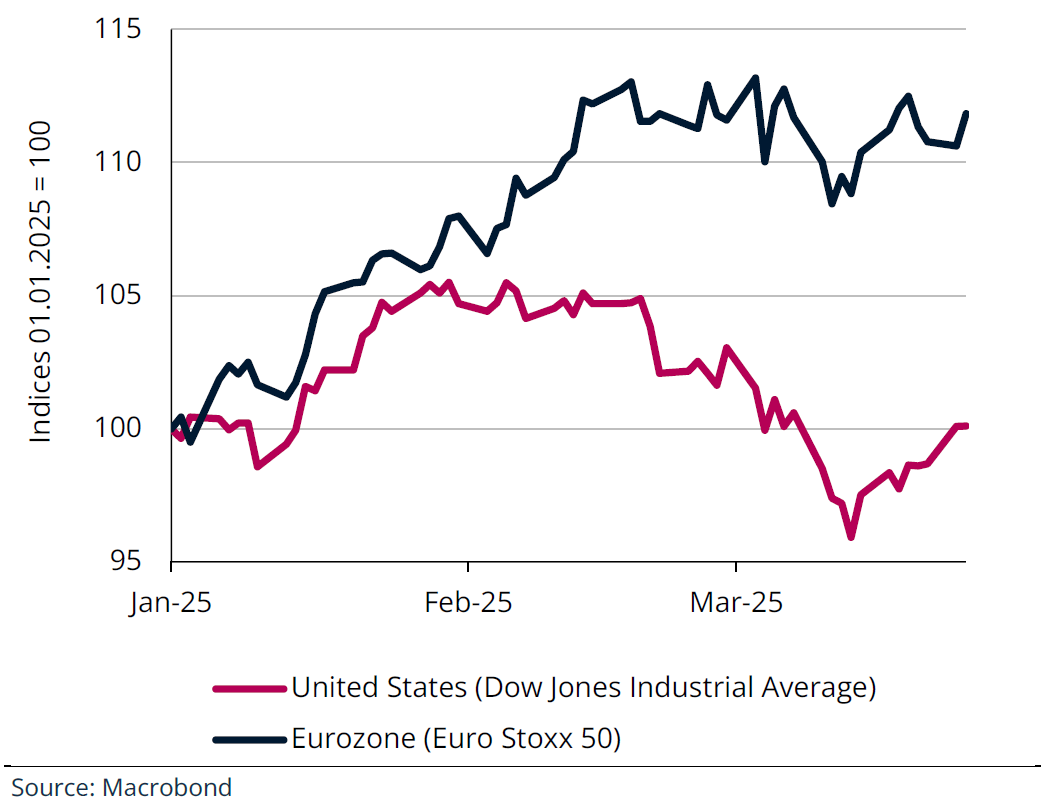

The rise in uncertainty is also reflected in a number of recent economic indicators. The financial markets, particularly the US stock markets, have fallen significantly since the end of February (see below). US consumer sentiment also seems to be taking a hit, with inflation expectations rising. The dollar has also deteriorated sharply against the euro in recent weeks.

Stock market indices

Luxembourg's direct exposure to the United States is relatively low

In terms of trade in goods, the United States accounted for around 3% of Luxembourg's exports in recent years (the proportion is the same for imports). This share is higher (around 6-7%) for metals and metal products (which account for 30-40% of all goods exported to the United States) and textile industry products (around 10% of goods exported to the United States). In terms of trade in services, the United States accounts for some 4-5% of Luxembourg's total exports (with an equivalent proportion and almost similar amounts for financial and non-financial services).

Despite this low direct exposure, Luxembourg could suffer from negative indirect effects linked to lower demand from the United States vis-à-vis its European partners. German car exports, for example, are being targeted by the Americans, and Germany is Luxembourg's biggest trading partner. This risk of contagion spreading through the financial markets is also a potential threat.

[1] These include:

"The economic impacts of Trump's tariff proposals on Europe", Policy insight, London School of Economics, October 2024

"Le prix du protectionnisme de Donald Trump", La lettre du CEPII, n° 450, November 2024

[2] OECD Economic Outlook, Interim Report March 2025

[3] On 4 March, the European Commission presented a massive EU rearmament plan worth EUR 800 billion.

Activity

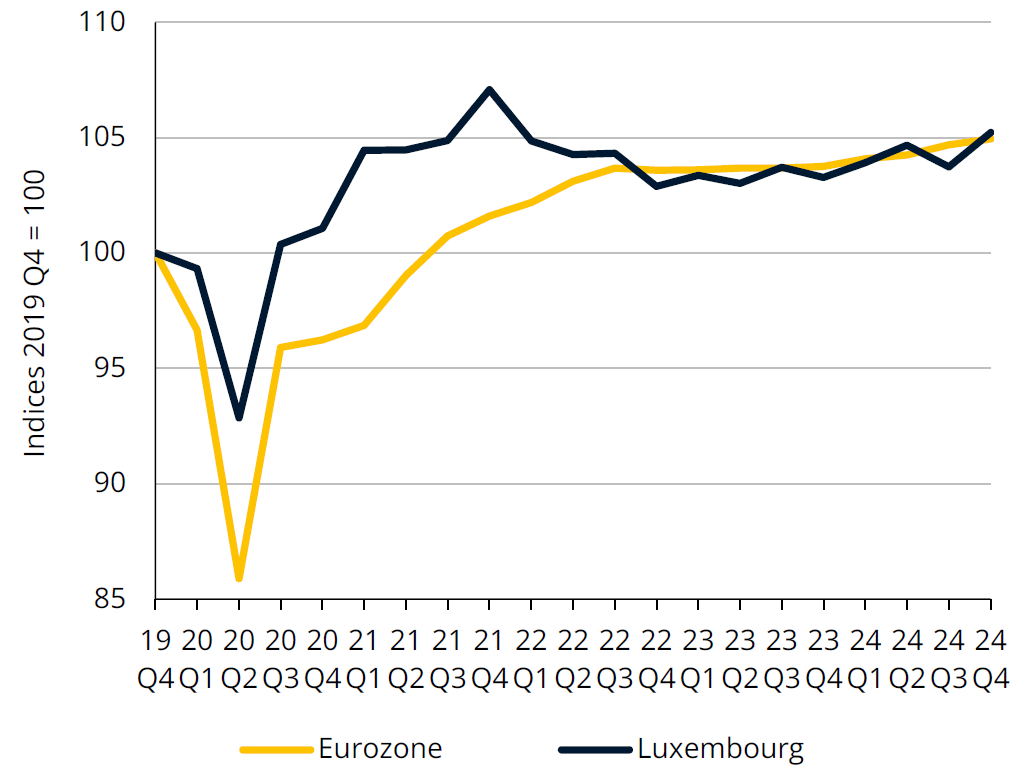

Real GDP in Luxembourg compared to the euro area

Sources: Eurostat, STATEC (seasonally adjusted data)

GDP growth in Q4 2024, +1.0% for the year as a whole

Real Luxembourg GDP grew by 1.4% over one quarter in Q4 2024. This growth was mainly driven by the financial sector, industry and non-market services. On the other hand, market services - with the exception of accommodation and food service activities - recorded a decline, particularly in the trade and ICT sectors (whose respective Q3 figures have been revised downwards). All in all, GDP rose by 1.0% in 2024 (compared with the 0.5% anticipated in STATEC's December forecasts).

The annual national accounts have also been revised. While real GDP for 2023 (-0.7%) fell by slightly less than previously estimated (-1.1%), the figure for 2022 is now also down (-1.1%, compared with +1.4% in the previous version of the accounts): this revision for 2022 is mainly due to significantly more negative results in the construction industry (especially property development) and trade sector (especially wholesale trade). The trend in real GDP has also been revised for 2018 to 2021, but only marginally.

Financial sector

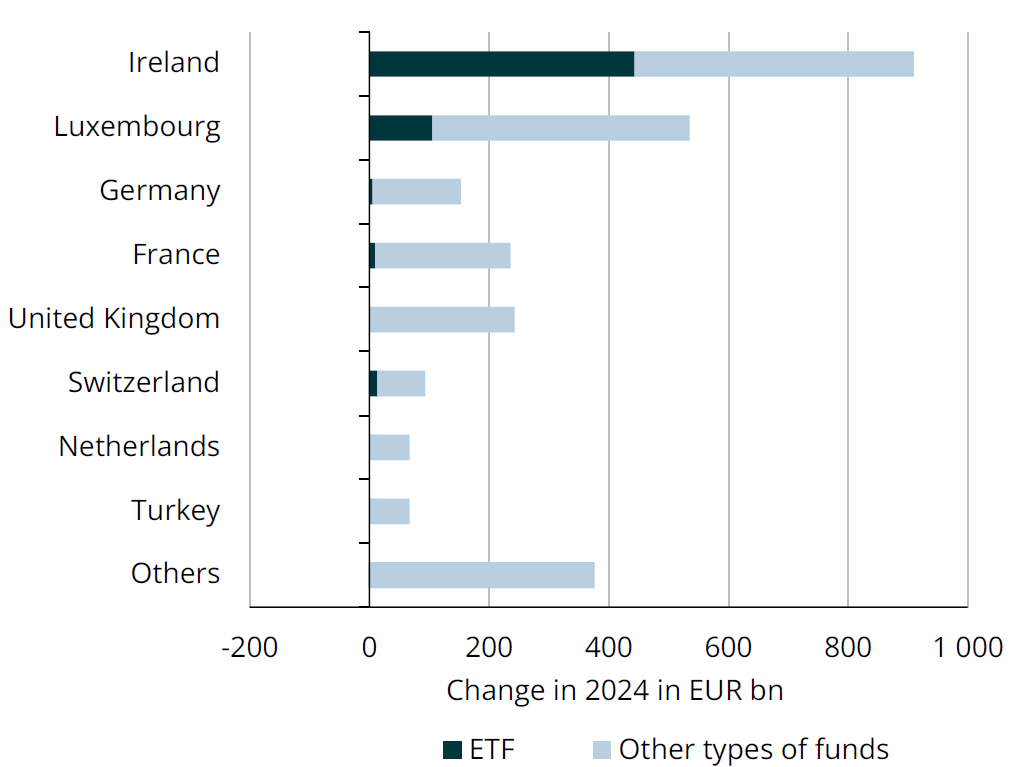

Changes to net assets of European investment funds

Source: EFAMA

Ireland gains further market share in funds

In 2024, the net assets of European investment funds rose by 13% (+10% in Luxembourg), driven by growth in equity prices and an upturn in net issues, particularly in Q4. While valuations account for three-quarters of fund growth, net issuance has more than doubled in Europe. Almost 40% of these issues involve exchange-traded funds (ETFs), which are less expensive than traditional funds. These funds are predominant in Ireland because of its agreement with the United States, which halves the withholding tax on dividends for ETFs linked to US equities. Ireland has attracted 85% of net ETF issuance in Europe over the last three years, and has gained three percentage points of market share in the fund sector. It now accounts for 21% of total European assets, compared with 25% for Luxembourg (-2 percentage points). To capitalise on this growth, Luxembourg abolished the subscription tax on active ETFs in January.

Q1 2025 was marked by a recovery in eurozone long-term interest rates and a decline in share prices of US technology and automotive companies. Net issuance should therefore remain positive for money market and bond funds, but could fall for ETFs and other funds investing in US equities.

Financial environment

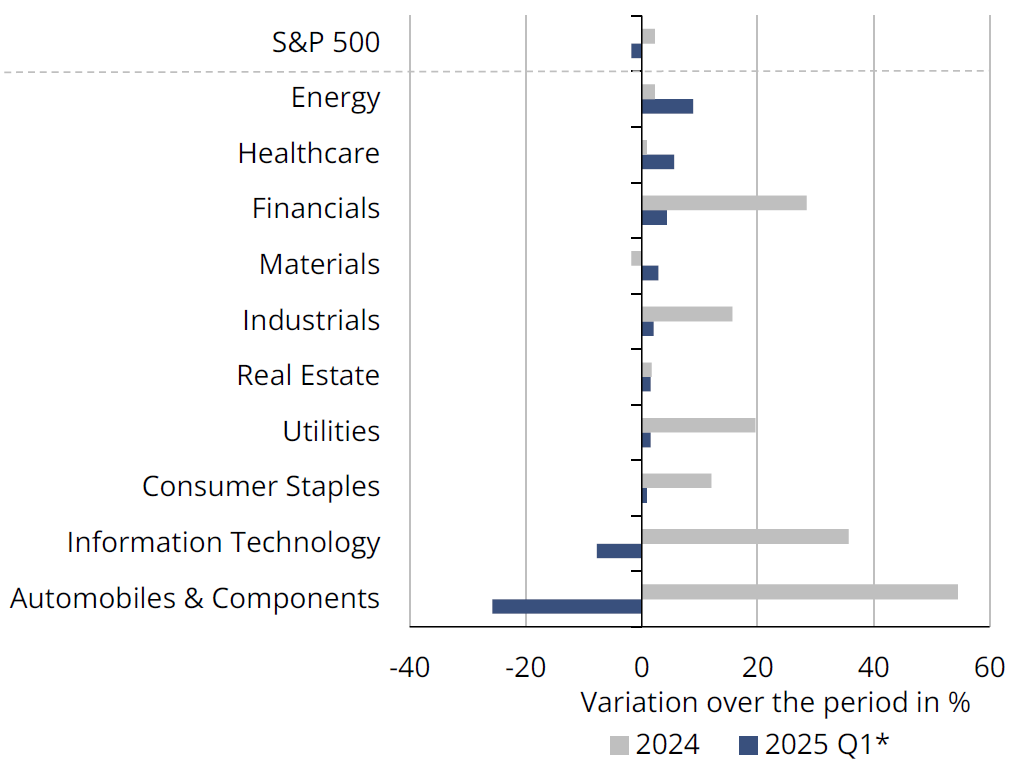

Sectors in the US S&P 500 index

Source: Macrobond

* Data observed up to 25 March 2025

Turbulence on Wall Street

Volatility on Wall Street has risen sharply since the end of February, against a backdrop of concerns about the US economy and international trade, as well as a wave of profit-taking following the strong rise in share prices in 2024. Over the last 35 days, the NASDAQ has fallen by 9%, the S&P 500 by 6% and the Dow Jones industrial average by 4%. These benchmarks were dragged down by technology and automotive companies, the two sectors that posted the best performance in 2024.

The major technology companies in the so-called "Magnificent Seven" (Apple, Nvidia, Microsoft, Meta, Amazon, Alphabet, Tesla) have plunged on the stock market after two years of strong gains. The carmaker Tesla, whose share price soared following the election of Donald Trump and the prominent role given to the company's CEO, is now suffering from a collapse in sales in Europe and China (down by around 50% year-on-year in early 2025). Sales are falling due to competition from new electric models coming out of Europe and Asia, and probably also because of dissatisfaction with Elon Musk following his controversial public announcements. Tesla's significant rise on the stock market over the last two months of 2024 have since been completely wiped out.

Real estate

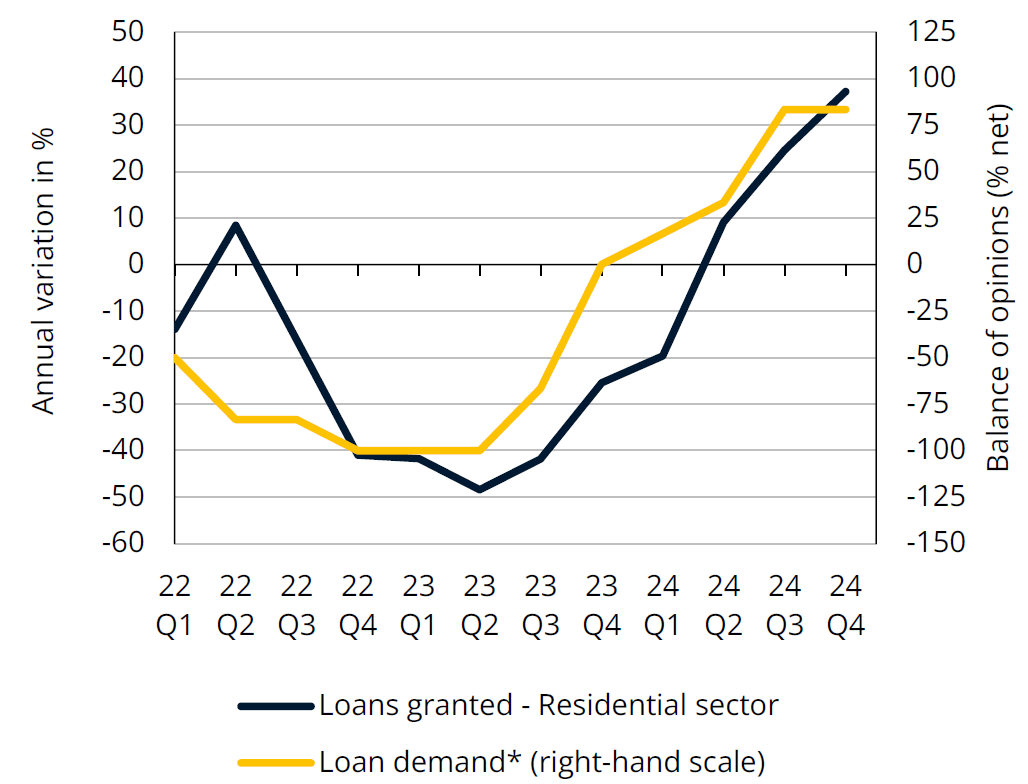

Mortages

Sources: BCL, BCE

*Result of the bank lending survey.

Sharp rise in mortgages at the end of 2024

The rise in lending for residential property in Luxembourg, which began in spring 2024, accelerated in Q4 2024 (+37% year-on-year, following on from +25% and +9%). This increase is largely attributable to the growth in approved loans (with selling prices remaining rather stable over the period). This is due to loans to non-property developers (which account for an average of 90% of residential loans), which were very buoyant at the end of the year, increasing by around 75% over the past 12 months. Conversely, loans to property developers, which are more volatile and account for a smaller share of the total, continued to fall and reached very low levels in Q4.

The banks are also reporting a rise in mortgage applications, which they say has been helped by an improved outlook for the real estate market and increased consumer confidence. In fact, intentions to buy a home have been on the rise since mid-2024, a trend that has continued into 2025. The increase in lending at the end of 2024, which should be reflected in the number of housing transactions, must be seen against the backdrop of falling mortgage rates and the government measures, which were due to expire at the end of the year, but have been extended.

Inflation

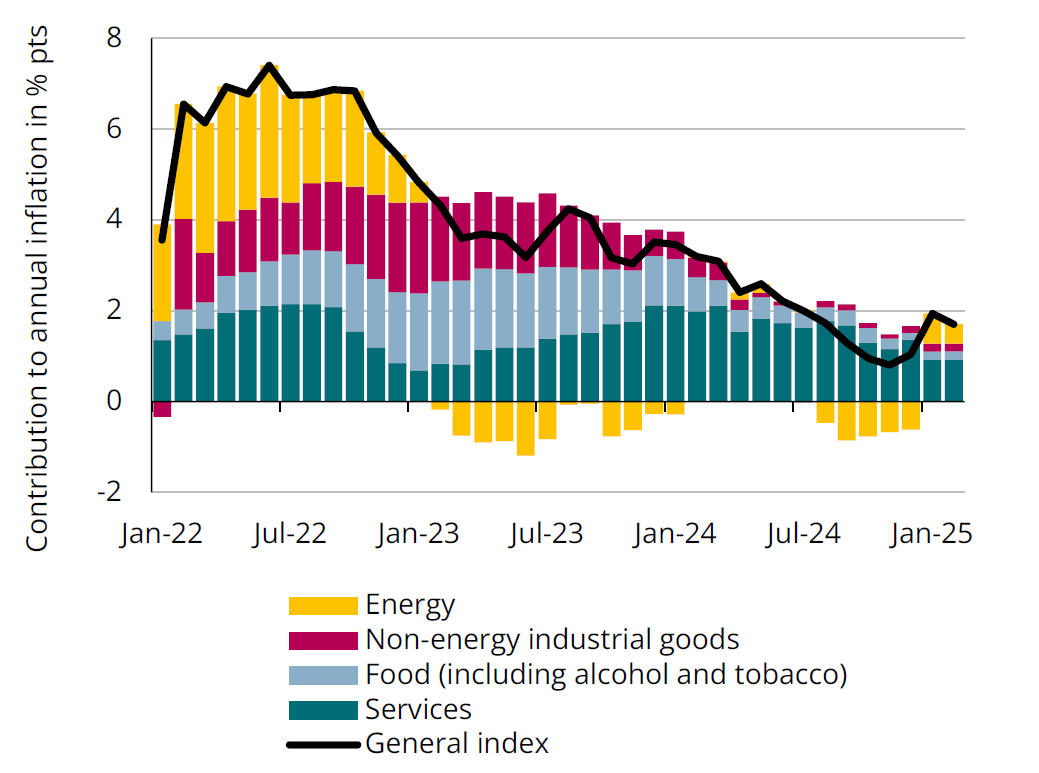

Breakdown of inflation in Luxembourg

Source: STATEC

Inflation remains moderate

In February, inflation stood at 1.7% in Luxembourg, after 1.9% in January and 1.0% in December. Services continue to make the biggest contribution to price rises in the Grand Duchy, although this contribution tends to fall (+0.9 percentage points in February, after peaking at 2.1 percentage points a year ago). However, this trend could be reversed with the next wage indexation scheduled for Q2. Since the partial lifting of the price cap on

1 January 2025, energy has once again made a positive contribution to inflation (+0.5 percentage points on average over the first two months of the year, with 0.4 percentage points from electricity). The prices of food and non-energy industrial goods, which had risen sharply in 2022 and 2023 as a result of the sharp rise in energy prices, have almost no impact on inflation at the start of 2025 (each contributing +0.2 points).

In the eurozone, inflation remained restrained at 2.3% in February. However, tensions are slightly higher than in Luxembourg for services and food prices. As far as energy prices are concerned, at present, they barely contribute to inflation in the eurozone, as the majority of the price caps ended more than a year ago.

Labour market

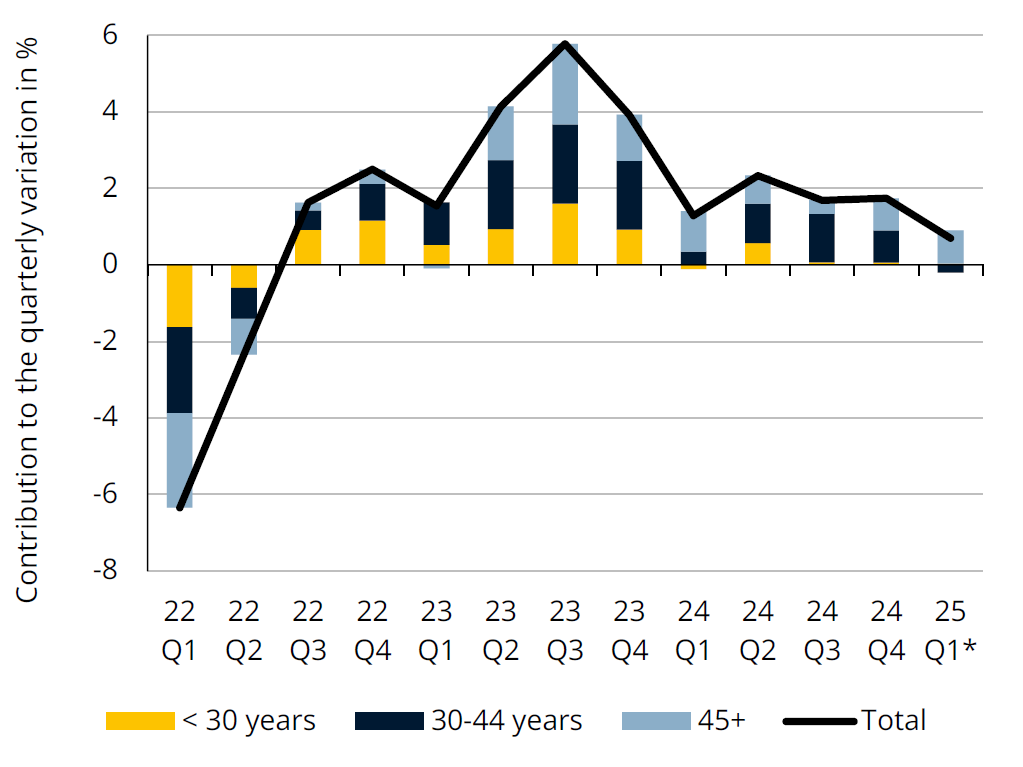

Unemployment by age group

Sources: ADEM, STATEC - seasonally adjusted data (*2 months)

The rise in unemployment seems to be tailing off

The rise in unemployment has eased considerably in recent quarters, and the unemployment rate has tended to stabilise, settling at 5.9% of the labour force since November 2024. On the one hand, there have been fewer new registrations in recent months and, on the other, more case files have been closed.

The under 30s, who account for around one in five of the unemployed registered with ADEM, have made virtually no contribution to the rise in unemployment since mid-2024, thus pointing to a slight recovery in the labour market. Young people entering the labour market are traditionally the first to suffer during a downturn (less recruitment), but they are also the first to be hired during an upturn. In recent months, there has also been a fall in the number of unemployed in the construction trades.

The unemployment rate in the eurozone continues to fall, reaching 6.2% of the labour force in January 2025, almost the same level as in the Grand Duchy, which historically had some of the lowest rates in the zone.

Energy

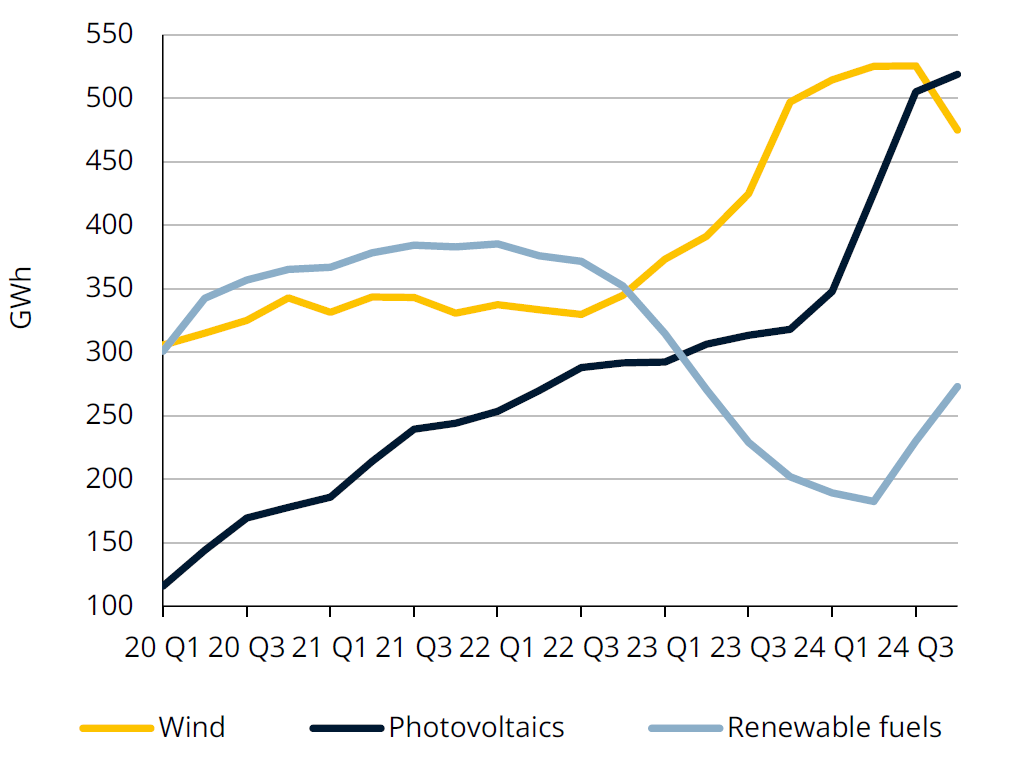

Production of renewable electricity

Source: Eurostat (sum of the last four quarters; 2024 estimated)

Photovoltaics would outstrip wind power in Luxembourg

In 2024, renewable energies in Luxembourg experienced contrasting trends. After a modest increase in photovoltaic production in 2023 (+9%), it surged in 2024 (+63%), overtaking wind generation for the first time. This growth is due partly to a record expansion in capacity, with the number of installations rising from 14,000 to almost

23,000, and by more favourable weather conditions, with a 7% increase in the number of hours of sunshine compared with 2023.

Conversely, wind generation slowed. After a sharp increase in 2023 (+44%), it fell slightly in 2024 (-4%). This fall is explained by a relative stability in capacity (+3%) and a reduction in average wind speed

(-10%). However, with future wind farm projects already authorised, capacity growth is set to increase once more. Electricity generation using renewable fuels recovered in 2024 (35%) after a sharp fall in 2023 (-43%), mainly due to the production of electricity from scrap wood

* Update on 1 April 2025 at 7:00 pm

Clarifications following the publication of the Flash Economic Survey of 27 March 2025.

The statistics relating to electricity production in 2024, released by Eurostat, are based, in part, on estimated data that needs to be confirmed.

According to these estimates, photovoltaic electricity production will exceed wind power production in 2024. The final figures, which may confirm this observation, will not be available until June 2025.

Another clarification: the graph shows annual production calculated on a rolling basis, corresponding to the sum of production for the last four quarters for each given quarter.

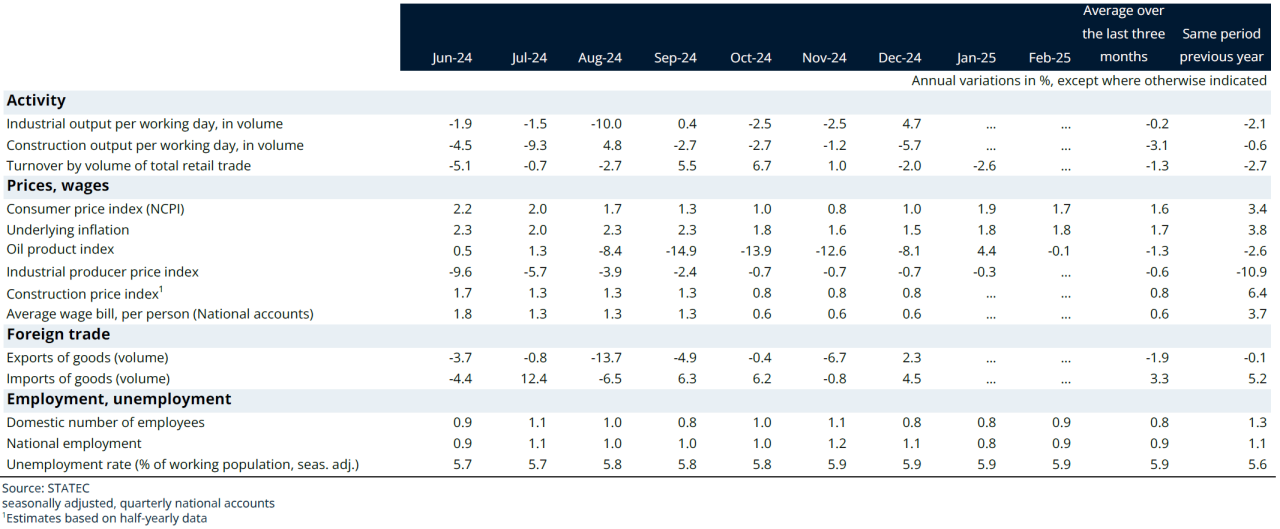

Dashboard

Indicators

Last update