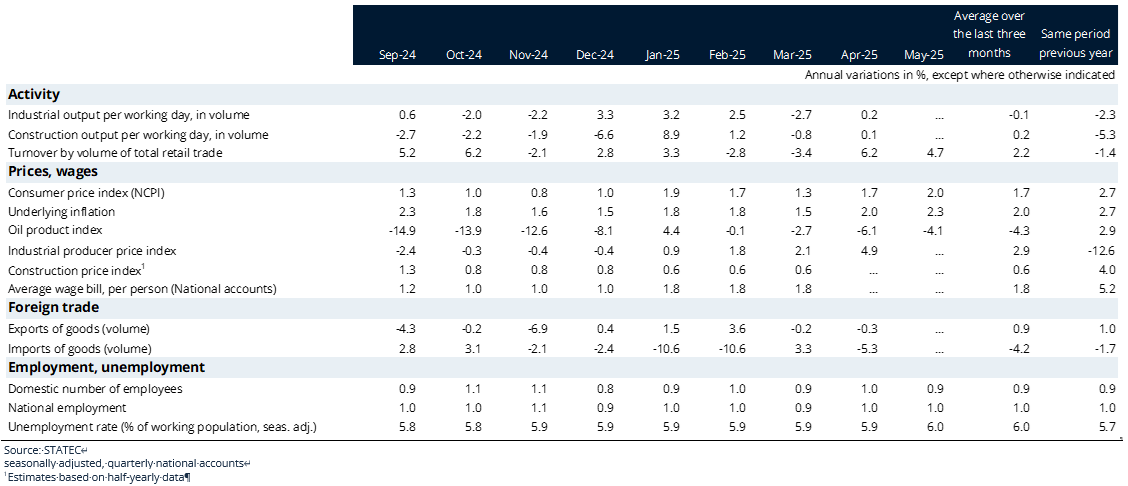

Conjoncture Flash June 2025:Low growth in Luxembourg in 2025 & 2026

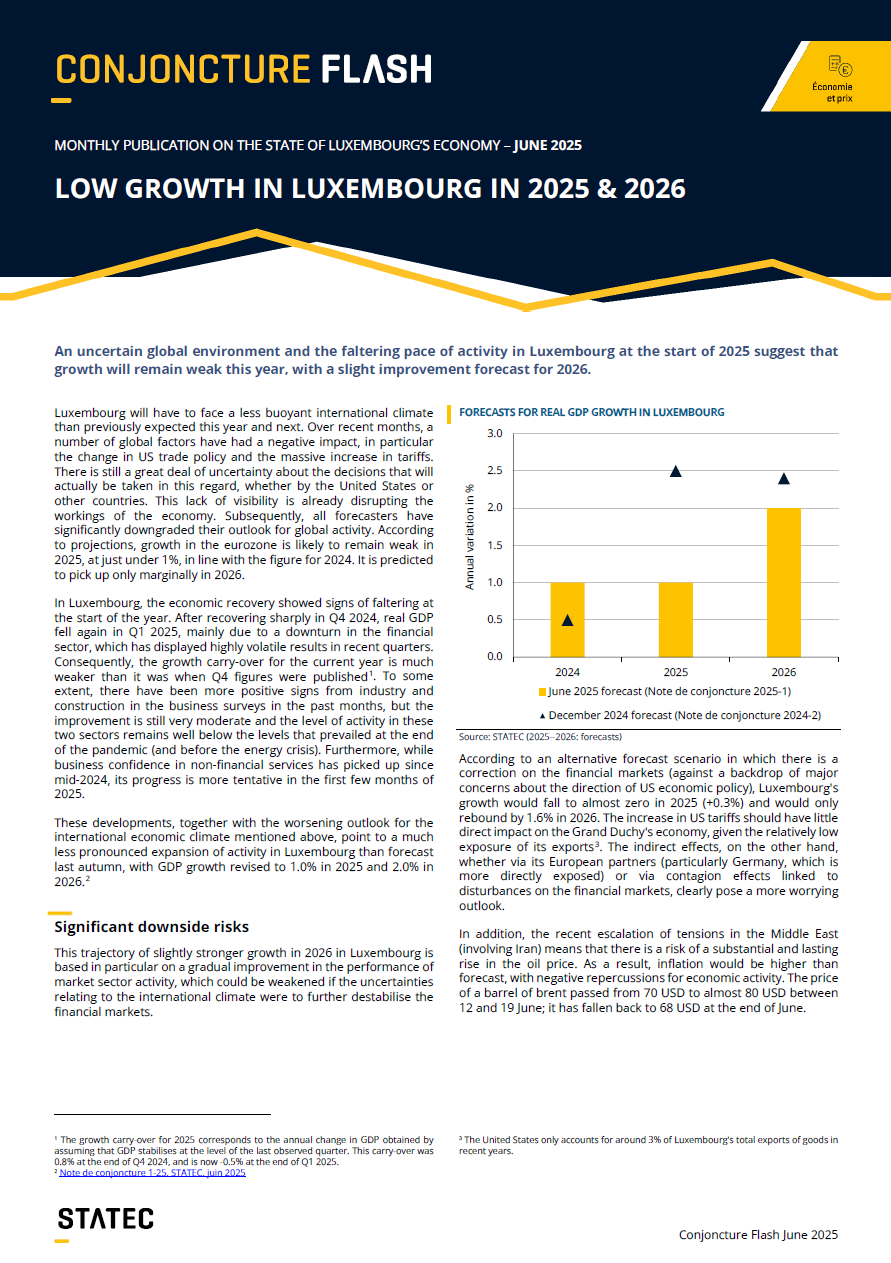

An uncertain global environment and the faltering pace of activity in Luxembourg at the start of 2025 suggest that growth will remain weak this year, with a slight improvement forecast for 2026.

Luxembourg will have to face a less buoyant international climate than previously expected this year and next. Over recent months, a number of global factors have had a negative impact, in particular the change in US trade policy and the massive increase in tariffs. There is still a great deal of uncertainty about the decisions that will actually be taken in this regard, whether by the United States or other countries. This lack of visibility is already disrupting the workings of the economy. Subsequently, all forecasters have significantly downgraded their outlook for global activity. According to projections, growth in the eurozone is likely to remain weak in 2025, at just under 1%, in line with the figure for 2024. It is predicted to pick up only marginally in 2026.

In Luxembourg, the economic recovery showed signs of faltering at the start of the year. After recovering sharply in Q4 2024, real GDP fell again in Q1 2025, mainly due to a downturn in the financial sector, which has displayed highly volatile results in recent quarters. Consequently, the growth carry-over for the current year is much weaker than it was when Q4 figures were published[1]. To some extent, there have been more positive signs from industry and construction in the business surveys in the past months, but the improvement is still very moderate and the level of activity in these two sectors remains well below the levels that prevailed at the end of the pandemic (and before the energy crisis). Furthermore, while business confidence in non-financial services has picked up since mid-2024, its progress is more tentative in the first few months of 2025.

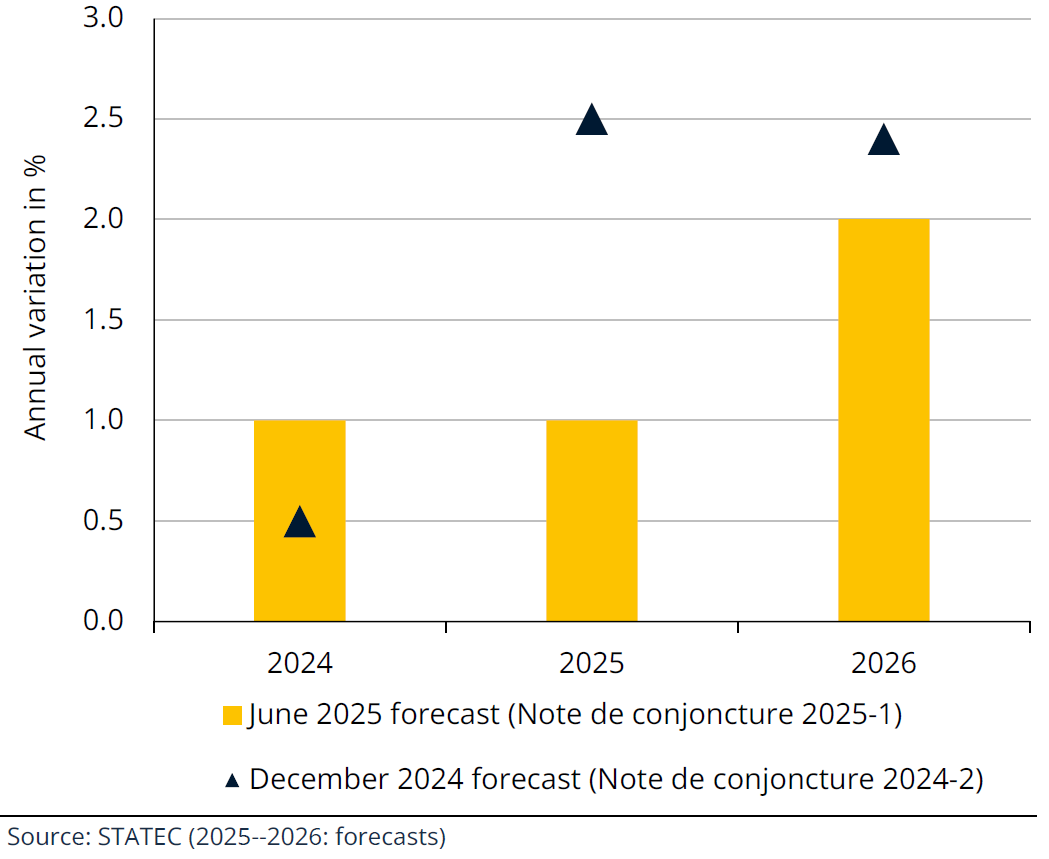

These developments, together with the worsening outlook for the international economic climate mentioned above, point to a much less pronounced expansion of activity in Luxembourg than forecast last autumn, with GDP growth revised to 1.0% in 2025 and 2.0% in 2026.[2]

Significant downside risks

This trajectory of slightly stronger growth in 2026 in Luxembourg is based in particular on a gradual improvement in the performance of market sector activity, which could be weakened if the uncertainties relating to the international climate were to further destabilise the financial markets.

Forecasts for real GDP growth in Luxembourg

According to an alternative forecast scenario in which there is a correction on the financial markets (against a backdrop of major concerns about the direction of US economic policy), Luxembourg's growth would fall to almost zero in 2025 (+0.3%) and would only rebound by 1.6% in 2026. The increase in US tariffs should have little direct impact on the Grand Duchy's economy, given the relatively low exposure of its exports[3]. The indirect effects, on the other hand, whether via its European partners (particularly Germany, which is more directly exposed) or via contagion effects linked to disturbances on the financial markets, clearly pose a more worrying outlook.

In addition, the recent escalation of tensions in the Middle East (involving Iran) means that there is a risk of a substantial and lasting rise in the oil price. As a result, inflation would be higher than forecast, with negative repercussions for economic activity. The price of a barrel of brent passed from 70 USD to almost 80 USD between 12 and 19 June; it has fallen back to 68 USD at the end of June.

[1] The growth carry-over for 2025 corresponds to the annual change in GDP obtained by assuming that GDP stabilises at the level of the last observed quarter. This carry-over was 0.8% at the end of Q4 2024, and is now -0.5% at the end of Q1 2025.

[2] Note de conjoncture 1-25, STATEC, juin 2025

[3] The United States only accounts for around 3% of Luxembourg's total exports of goods in recent years.

Real estate

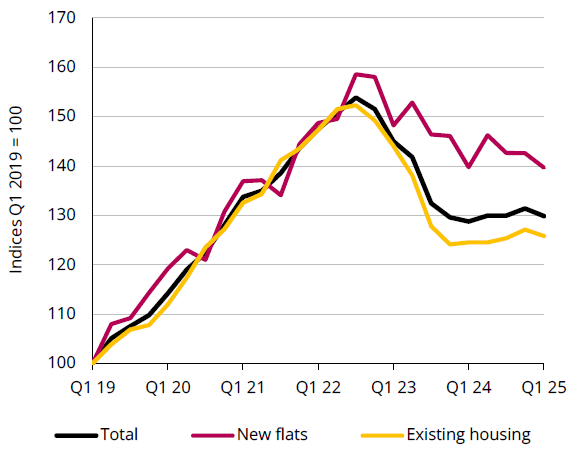

Sales prices of housing

Source: STATEC

(Temporary?) hiatus in the real estate recovery in Q1

Housing transactions fell in Q1 2025 across all property segments (between -9% and -18% over a quarter, seasonally adjusted data). Nonetheless, this current decline should be viewed in the context of the particularly high number of transactions in Q4 2024. It is likely that real estate transactions were boosted by the expected expiry of State aid at the end of 2024. However, the government decided to extend the support measures until the end of June (with greater flexibility for completing the procedures). Thus, despite the recent decline, the underlying trend remains one of gradual improvement (the number of transactions being 27% higher than in Q1 2024, while still remaining lower than before the crisis).

The sales price of housing fell by 1.2% over the quarter, bringing to a halt the slight rise witnessed over the past year (particularly in the case of existing properties). This change may be linked to that seen in transactions over the same period (strong demand in Q4 followed by a contraction in Q1), so it would be premature to talk of a trend reversal.

Financial environment

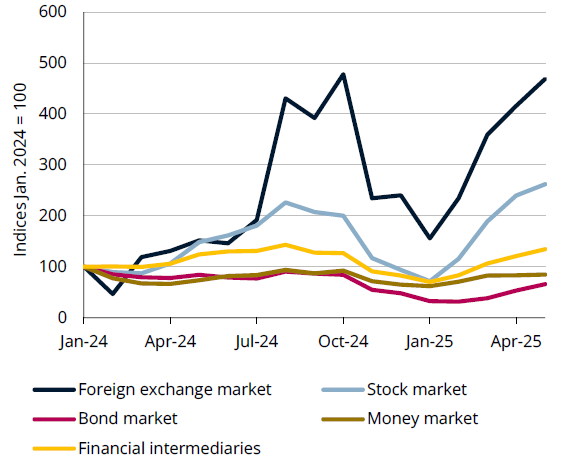

Systemic stress indicators in the eurozone

Source: BCE (moving averages over three months)

A perturbed financial environment

The ever-changing announcements on tariffs are destabilising the financial markets. They have also had a major impact on exchange rates. The dollar, which rose in the last quarter of 2024, fell over the first five months of 2025. In contrast, the euro has gained in value against the currencies of its main trading partners (it is now worth USD 1.14 compared with USD 1.04 at the end of 2024, and 8.22 yuan compared with 7.58 yuan at the end of 2024). On 22 April, the eurozone's nominal effective exchange rate reached its highest level since the creation of monetary union.

The stock market indices of the main financial centres fell in March and April, against a backdrop of high volatility. In the eurozone, the benchmark equity index (Stoxx 50) recovered, but declined slightly in June due to heightened tensions in the Middle East, which caused oil-related stocks to rise, while all other sectors fell. Demand for sovereign bonds increased in the eurozone but decreased for US Treasuries (usually the preferred choice when risk rises) due to a certain lack of confidence in US debt and automatic selling by some hedge funds. Long-term interest rates in the eurozone thus rose by 0.3 percentage points over the first five months of 2025, while short-term rates fell by 0.7 percentage points following three key rate cuts (a fourth rate cut took place at the beginning of June).

Financial sector

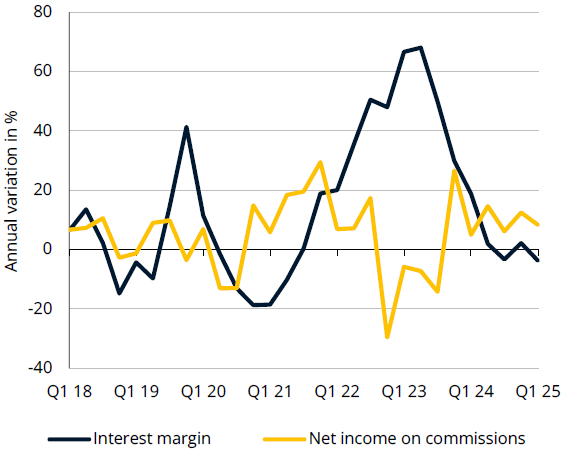

Main banking revenue items

Source: CSSF (decumulated data)

Gloomy Q1 results for the financial sector

Results in the financial sector were fairly mixed in Q1 2025, due to high levels of volatility on stock markets, the rise in long-term interest rates and the cuts in key rates in the eurozone. Compared with the last quarter of 2024, value added in the financial sector at current prices rose modestly for financial auxiliaries (notably fund management companies) and insurance companies (+2.6% and +2.1% respectively over one quarter), while it fell for banks (-2.7%). For the latter, the interest margin fell by 2.8% quarter-on-quarter (-3.8% year-on-year) due to the fall in rates, and net commissions were slightly lower than those received in Q4 2024 (‑0.7% quarter-on-quarter, +8.4% year-on-year).

Taking into account price effects linked to stock market valuations and interest rates, real value added in the financial sector fell by 3.9% in Q1 2025, after rising by 3.4% in Q4 2024, thus displaying relatively high volatility.

Inflation

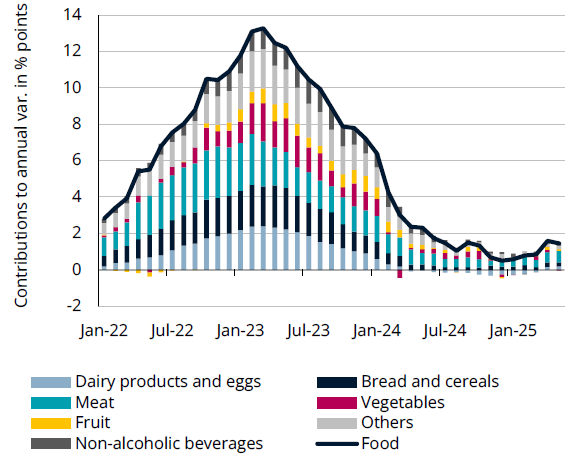

Food inflation

Source: STATEC

Slight rise in food price tensions

Since January 2025, there has been a slight rise in food inflation (+1.5% in May 2025, after a low point of +0.5% in December 2024). This trend is mainly attributable to dairy products (where prices have risen slightly after falling over the previous twelve months), fruit, meat, coffee and cocoa. In May, prices for cocoa (+13.6% year-on-year), sheep and goat meat (+11.7%) and coffee (+10.3%) rose the most year-on-year, followed by beef (+8.4%), root vegetables other than potatoes (+8.2%) and butter (+6.9%).

Compared with the eurozone, food inflation remains relatively low in Luxembourg (+1.5% in May, compared with +2.9% in the eurozone). Over the first five months of 2025, this difference is due mainly to chocolate (+4.2% in Luxembourg, versus +15.7% in the eurozone), cheese (-0.3% versus +2.9%), fresh or chilled fruit (+1.5% compared with +3.9%), coffee (+6.5%, compared with +13.3%), mineral or spring waters (-2.1% compared with +2.6%) and fresh or chilled vegetables (+1.1% compared with +3.1%). By contrast, price pressures are more marked in Luxembourg for olive oil (+8.4%, compared with -18.6% in the eurozone).

Wages

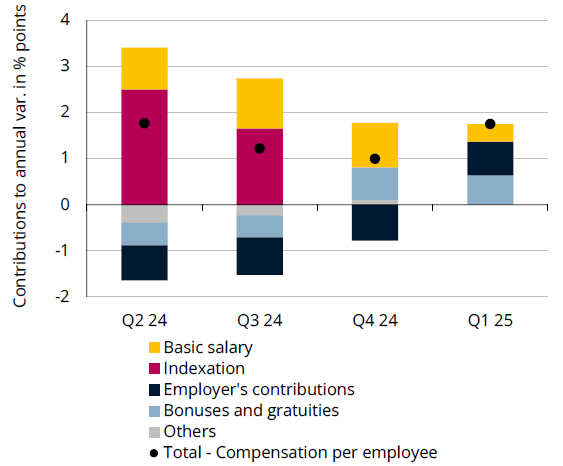

Compensation per employee

Sources: IGSS, STATEC

Wage costs boosted by rebound in contributions in Q1

In Q1 2025, compensation per employee (CPE) rose by 1.8% year-on-year, after experiencing a slowdown in 2024. This slight increase at the start of the year was mainly due to the upturn in employers' contributions. They were lowered in 2024, making a negative contribution to CPE growth, and returned to their normal level in 2025, having an upward effect on the CPE (these changes do not influence the wages received by employees). In recent quarters, the gradual disappearance of the impact of indexation has contributed to the slowdown in CPE. Indexation did not have any effect anymore at the turn of 2024-25, but it will again support CPE growth from Q2 owing to the indexation of May 2025. In addition, over the last two quarters, bonuses and gratuities, which rose in Q4 mainly due to professional, scientific and technical activities and in Q1 due to financial activities, had a positive influence on CPE growth.

For 2025 as a whole, a 3.3% rise in CPE is forecast, followed by 2.3% in 2026. While the non-market sector will benefit from the wage agreement in the civil service (+2% in 2025 and a further +0.5% in 2026), wages excluding indexation in the market sector will display little dynamism over this period, in line with activity and employment.

Labour market

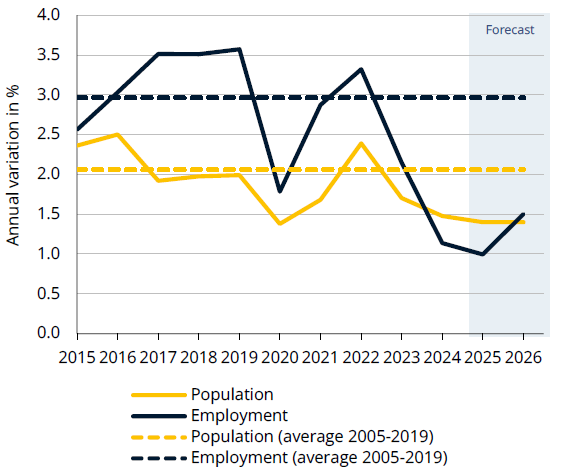

Employment and population forecasts

Source: STATEC (2025-2026: June 2025 forecasts)

Joint slowdown in employment and population

Employment growth has slowed considerably since the post-Covid recovery, and is likely to remain very moderate this year according to STATEC's June forecasts. With 1% growth in 2025, employment growth would remain historically low, comparable to the levels in a crisis year such as 2009, and a far cry from the average annual growth recorded in pre-Covid years, which was close to 3%. A recovery in employment, which usually lags activity by three to four quarters, is not expected until 2026 (+1.5% year-on-year), driven by slightly more dynamic private non-financial employment (+1.2% following on from +0.6% in 2024 and 2025).

The unemployment rate is expected to remain high over the forecast horizon, reaching 6.0% of the labour force in 2025, before falling very slightly to 5.9% in 2026. The population is expected to continue to grow, but at a much slower rate than in the last two decades, mainly due to low immigration: +1.4% in both 2025 and 2026 (i.e. the rate seen at the height of the Covid crisis in 2020, compared with +2.1% on average between 2005 and 2019).

Energy

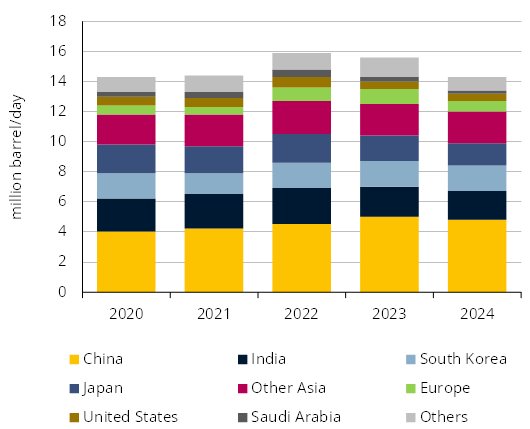

Destination of crude oil transported through the Strait of Hormuz

Source: U.S. Energy information administration

Energy markets turn their attention to the Strait of Hormuz

Following the hostilities between Israel and Iran, the Strait of Hormuz is attracting increasing attention, as about one-fifth of the world's total oil consumption passes through this strategic route. Any disruption in this region would have a significant impact on the global oil market, particularly for Asian countries, which account for almost 80% of the destinations for this oil. There are, however, alternatives to mitigate the impact of such disruptions, in particular through pipelines in Saudi Arabia and the United Arab Emirates, but their capacity is still insufficient to replace the volumes currently transported by this sea route.

Furthermore, although Iran has repeatedly threatened to close the Strait, it is unlikely that it has the capacity to do so. In addition, this would not be in its economic interests as its own oil exports (around 2 million barrels a day, mostly destined for China) also use this route. As well as for oil, the Strait of Hormuz is also a strategic crossing point for around 20 % of the world's trade in liquefied natural gas, mainly from Qatar. Again, around 80% of this LNG is currently destined for Asian markets.

Dashboard

Indicators

Dernière modification le