Conjoncture Flash November 2025: Activity in the eurozone held up well in the 3rd quarter

Economic activity continued to grow over the summer in the eurozone, with results from France surprising on the upside. While there are still marked differences between Member States, overall performance suggests that 2025 will be better than previously expected.

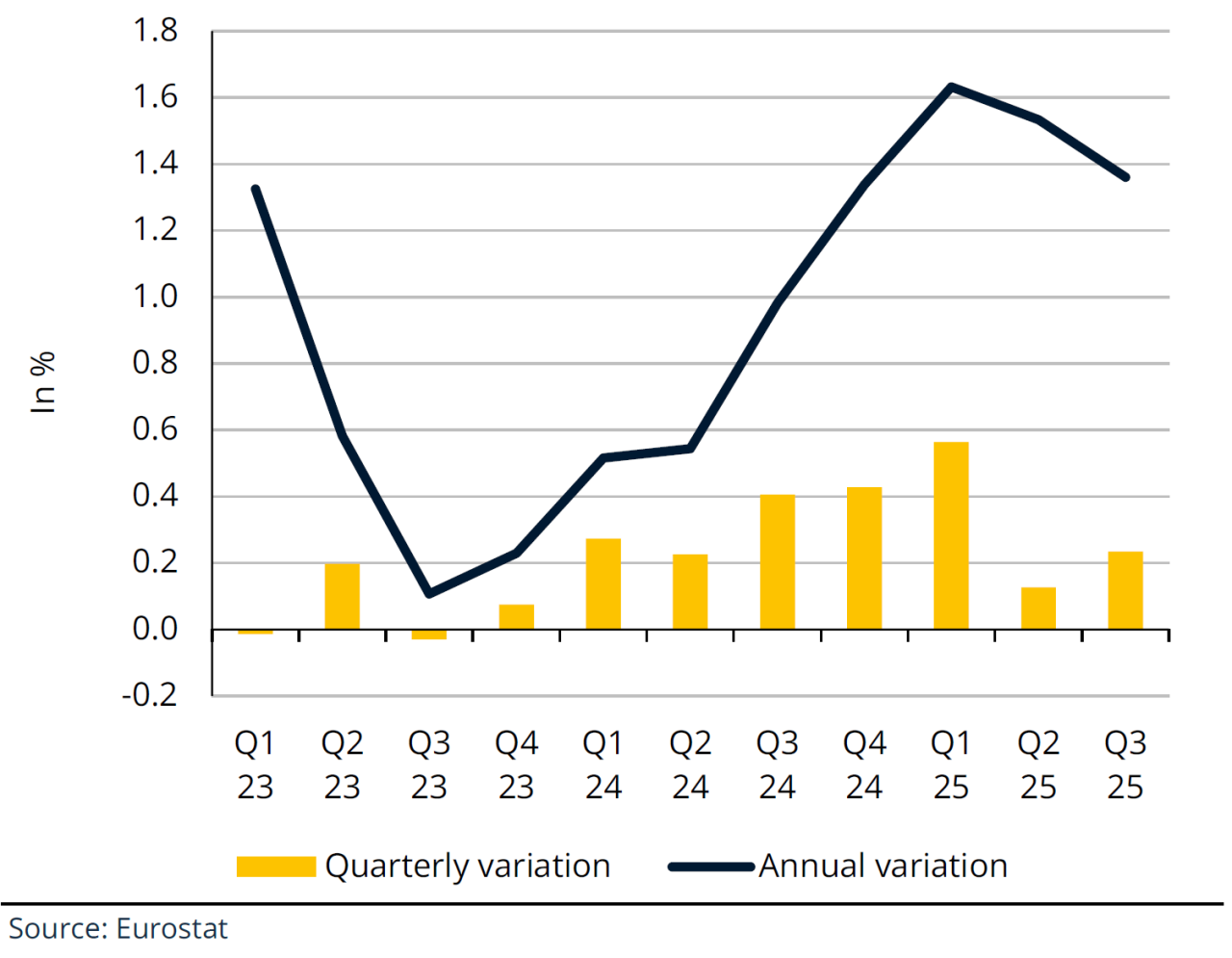

In the 3rd quarter of 2025, Eurozone GDP rose by 0.2% over one quarter (+1.3% over one year). This increase was slightly higher than expected,[1] due in no small part to results from France. French GDP rose by 0.5% over the quarter, well above the 0.2% increase expected by both INSEE and the Banque de France. This positive surprise is likely to have come mainly from exports of transport equipment (especially aeronautical equipment) and business investment in manufactured goods and services (within the information and communications sector in particular).

As in previous quarters, the Member States of the Iberian Peninsula remain on a solid growth trajectory (+0.6% in Spain, +0.8% in Portugal), largely due to the strength of domestic demand.

For their part, Germany and Italy narrowly escaped a technical recession (two consecutive quarters of falling GDP), showing stagnation in Q3 (following declines of -0.1% and -0.2% respectively in Q2). Despite a rebound in investment in machinery and equipment, German GDP suffered from a negative contribution from foreign trade. In contrast, foreign trade sustained Italy's growth, however, a drop in inventories had a negative effect.

3rd quarter GDP data for Luxembourg will be published on 5 December.

Towards a more solid expansion than expected this year

This result, combined with those for the first two quarters, suggests that growth in economic activity in the eurozone will be stronger than expected just a few months ago, for the year as a whole. In its latest forecasts, [2] the European Commission is now expecting growth of 1.3% in the eurozone this year, compared with the figure of 0.9% in its spring forecasts. [3] A similar upward revision is also evident in the new forecasts performed by the IMF (+1.2% in its October 2025 forecasts, compared with just 0.8% in those announced last April) and Oxford Economics (+1.4% currently compared with +0.8% in April).

[1] The consensus of analysts at FactSet and Bloomberg expected a rise of 0.1%.

[2] https://economy-finance.ec.europa.eu/economic-forecast-and-surveys/econ omic-forecasts/autumn-2025-economic-forecast-shows-continued-growth-despite-challenging-environment_en

REAL GDP in the eurozone

For the 4th quarter, consumer surveys are providing rather reassuring signals. The PMI composite activity index for the eurozone rose for the 4th month in a row in October, reaching its highest level in two and a half years (and fell only slightly in November according to the preliminary estimate). The economic sentiment indicator compiled by the European Commission has also been trending upwards in recent months.

The international context continues to be marked by trade tensions, particularly with the United States following the sharp increase in its tariffs, although the agreement reached with the European Commission has removed some uncertainties. While the effect of these tensions does not appear to have been too damaging for the eurozone for the time being, it is likely to be more marked next year: the forecasts for 2026 from the sources cited above have been revised downwards slightly (once again compared with the forecasts announced last spring), towards growth of close to 1%.[4]

[3] In these forecasts, published on 19 May, the quarterly growth observed in the 1st quarter and expected for the 2nd and 3rd quarters was roughly half the current figures.

[4] +1.2% for the European Commission, +1.1% for the IMF, +0.9% for Oxford Economics.

International 1/2

Unemployment rate

Source: Eurostat

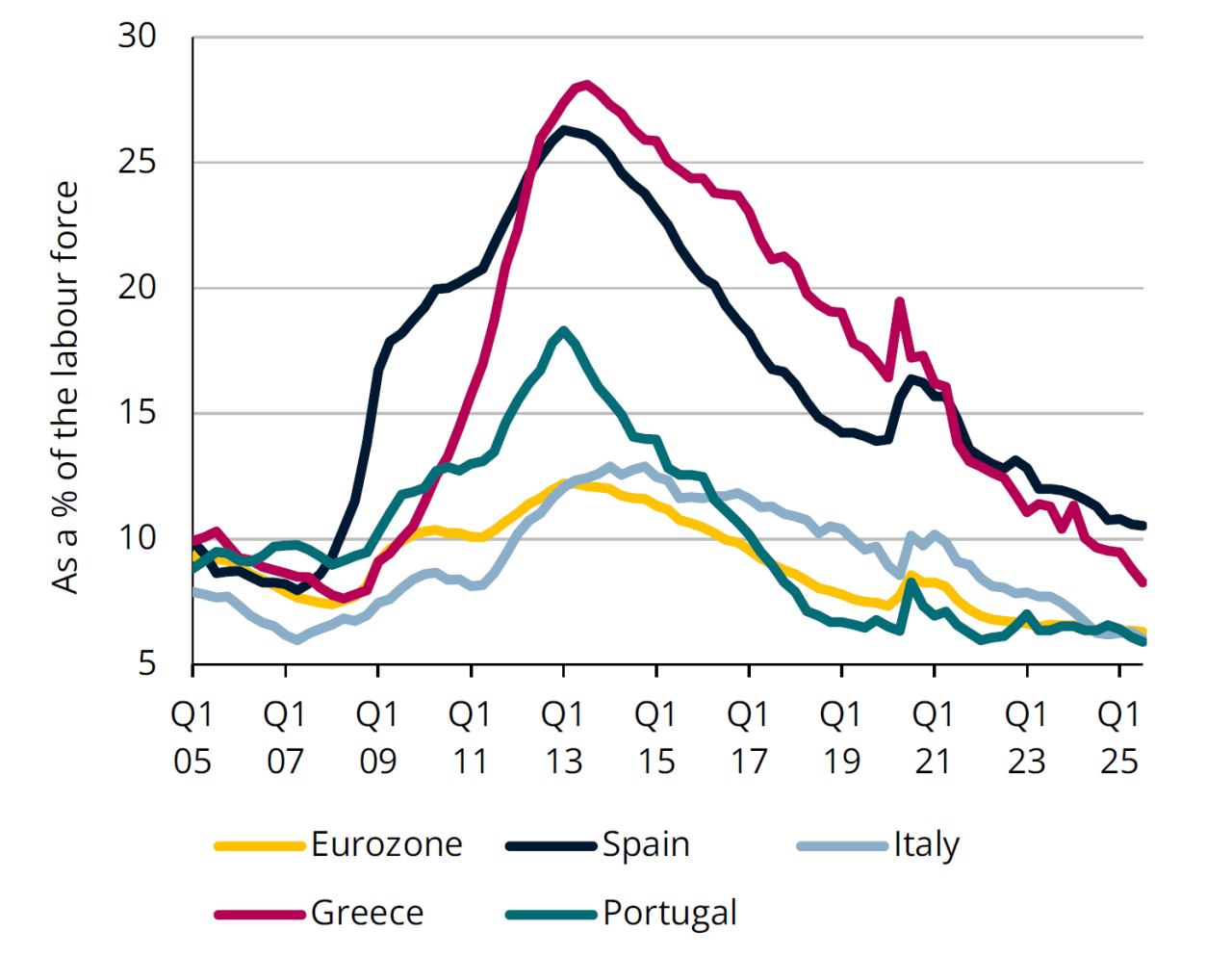

Unemployment no longer falling in the eurozone

With the subprime and sovereign debt crises, unemployment rose sharply in the eurozone (from 7.7% of the labour force in 2008 to 12.1% in 2013) and even exploded in the southern countries. Despite a steady decline since 2014, with a brief interruption in 2020 during the COVID-19 pandemic, Spain and Greece still have some of the highest unemployment rates (at 10.5% and 8.3% respectively in Q3 2025). Finland has also seen a sharp rise in jobseekers since the Russian invasion of Ukraine (the rate having risen from 6.4% in Q2 2022 to 9.9% in Q3 2025).

Since the beginning of 2025, the fall in unemployment in the eurozone appears no longer to be continuing, with the unemployment rate having stabilised at around 6.3%. Spain, Italy and Greece continue, however, to record a drop in the number of jobseekers. Conversely, Germany and France have been experiencing a rise in unemployment since 2023, and this trend has intensified in 2025. In Luxembourg, unemployment had resumed an upward trend as of 2022 but has tended to stabilise in recent months (at around 6.0%).

International 2/2

Sovereign ratings in the eurozone

Source: S&P Global Ratings

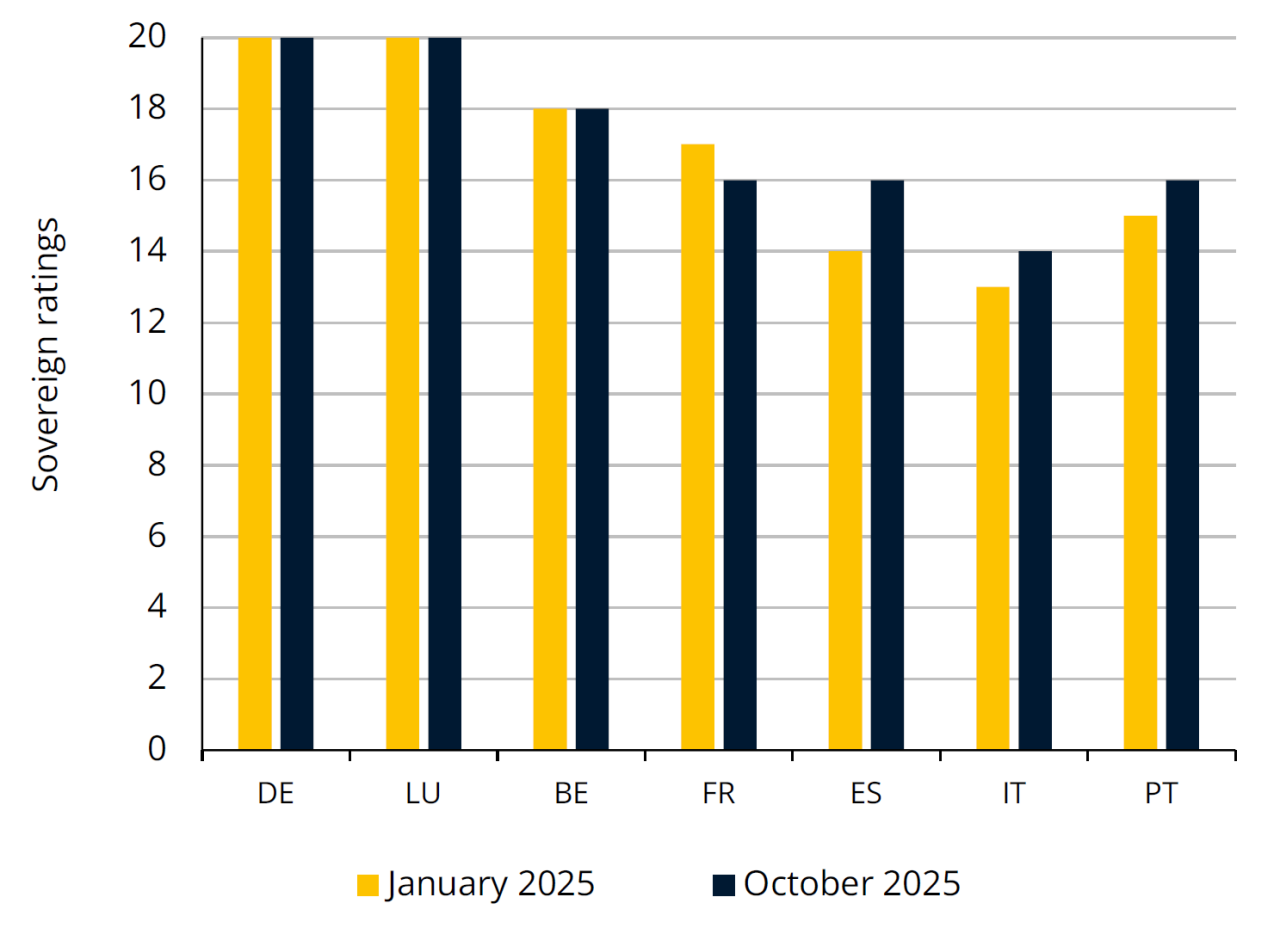

S&P Global Ratings' letter grades have been converted into ratings out of 20 (20 corresponding to the best AAA, 0 corresponding to CCC).

Better ratings for southern countries, but a downgrade for France

In autumn 2025, France saw its sovereign rating downgraded by Fitch and S&P Global Ratings, against a backdrop of political crisis combined with an excessive budget deficit and growing public debt. This reduction in France's rating should increase its borrowing costs and make future sovereign bond issues less attractive. Belgium's sovereign rating - two notches higher than France's - has been given a negative outlook due to increased risks associated with the implementation of fiscal consolidation and high economic vulnerability. Germany and Luxembourg have kept their maximum rating (triple A), with a stable outlook, thanks in particular to the efficiency and transparency of their institutional and budgetary frameworks.

Southern European countries have seen their ratings improve significantly, by one notch for Italy and Portugal and two notches for Spain. This favourable dynamic can be explained by several common factors: a significant improvement in their net external positions, an acceleration in the roll-out of the NextGenerationEU plan and resilient economies accompanied by robust labour markets. This improvement in sovereign ratings is also reflected in spreads with Germany, which have narrowed significantly since the start of 2025 for the economies of southern Europe.

Property

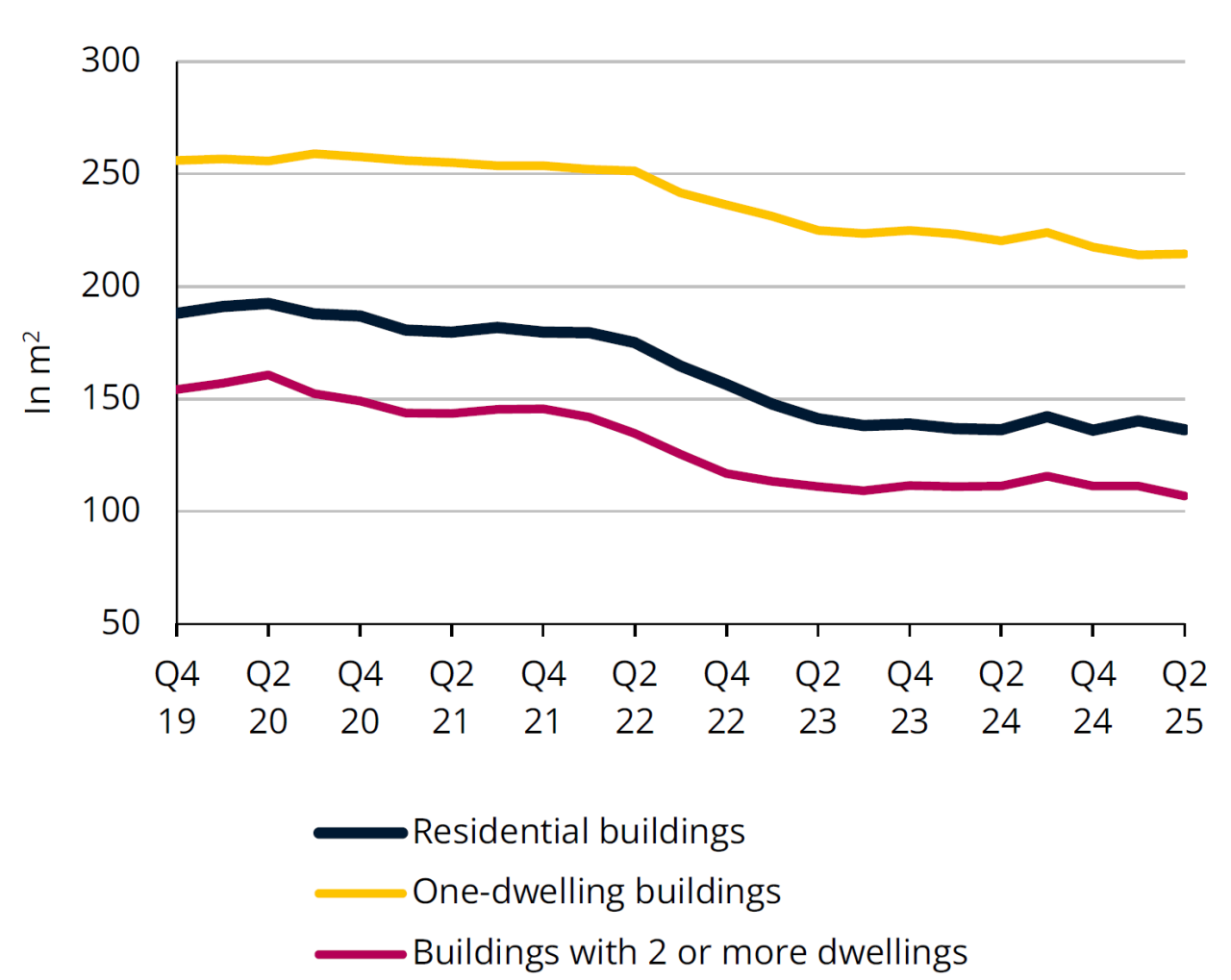

Building permits - Average floor area per dwelling

Source: STATEC (data smoothed over 4 quarters)

New homes are becoming smaller

Building permits show a clear decline in the average size of homes planned since 2022, for both houses and apartments. It is worth noting that the "Buildings with 2 or more dwellings" category includes all predominantly residential buildings, and therefore also includes some mixed-use buildings, which explains the apparently high average surface area within this category. The fall in the size of new dwellings is probably the result of the sharp rise in mortgage rates, which considerably increased the cost of purchasing housing. This shows that a downward adjustment in the new housing market has occurred, not only in terms of sales prices (around -3.5% in both 2023 and 2024), but also in terms of housing size.

This trend can also be observed for new apartments in the statistics of notarial acts of sale (which directly contain the surface area of the sold apartments). The average surface area of apartments sold under construction has only been around 77 m2 since 2023, compared with around 82 m2 over the previous ten years. In the 1st half of 2025, it even fell to 71 m2, the lowest level on record to date.

Financial sector 1/2

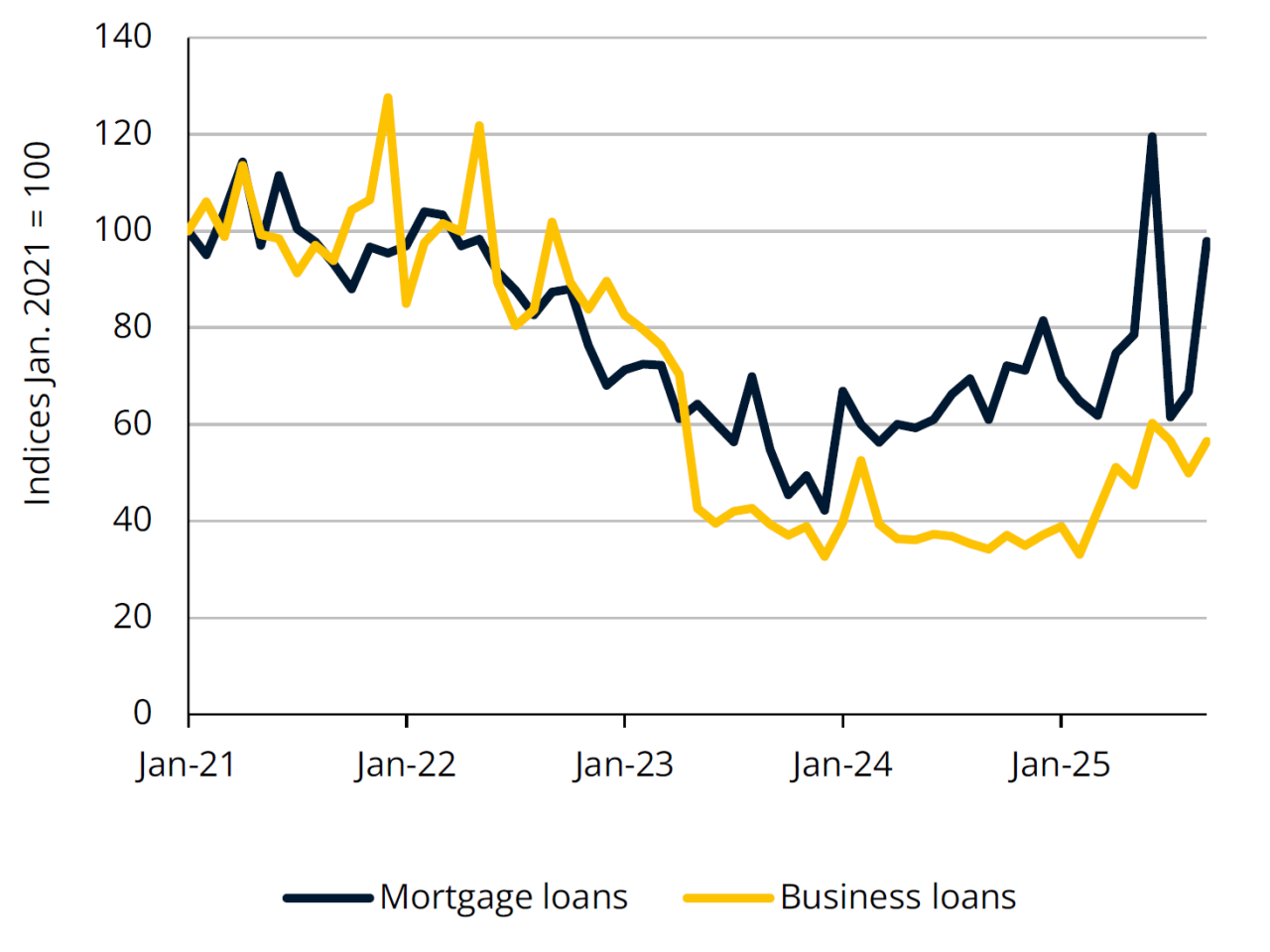

New loans granted by Luxembourg banks

Source: BCL

Demand for mortgage loans back on an upward trajectory

New mortgages granted by banks in Luxembourg surged in June, as households took advantage of the tax breaks linked to the housing package before they expired at the end of the month. Demand was weaker during the summer, then increased again in September. Over the first three quarters as a whole, new mortgages rose sharply (+25% year-on-year), while consumer credit declined by 4%.

Lending to non-financial companies between January and September was up by almost 30% year-on-year, but current levels are still 25% lower than they were at the start of 2022, before the rise in key interest rates. According to the Bank Lending Survey, the upturn in new business loans is mainly due to requests for refinancing and debt restructuring. The banks also indicated that they had tightened their lending criteria for small and medium-sized enterprises, mainly due to the capital requirements under the CRR (Capital Requirements Regulation) III directives.

For the 4th quarter of 2025, the banks expect demand for loans from households and businesses to stabilise.

Financial sector 2/2

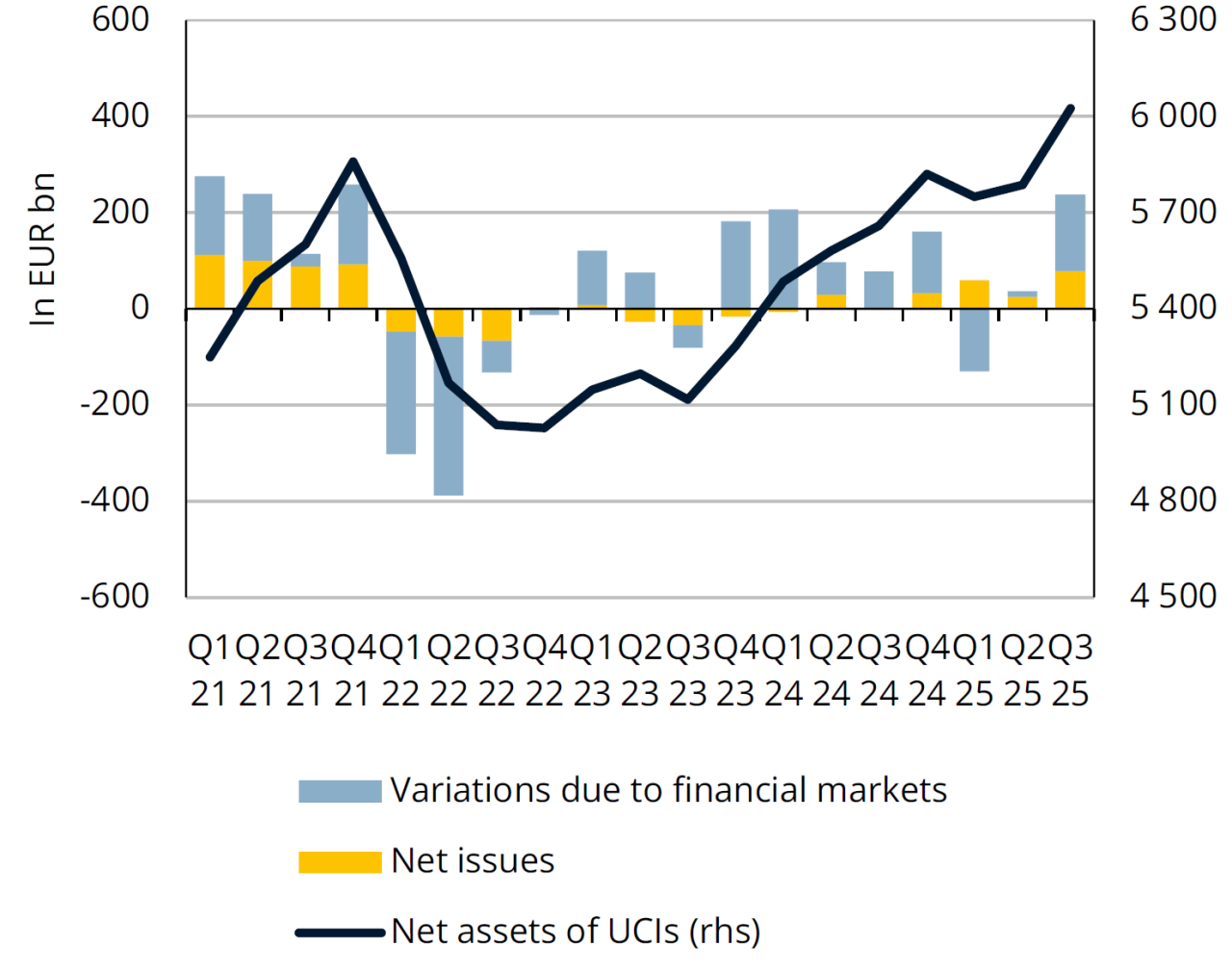

Undertakings for Collective Investment

Source: CSSF

Growth in investment funds valuations and issues

In the 3rd quarter, Luxembourg’s undertakings for collective investment (UCI) saw their net assets increase by 6.5% year-on-year. This increase was largely due to an upturn in equity valuations (+EUR 159 bn over the quarter), driven by investors' improved outlook for US trade and monetary policy, global growth and investment in artificial intelligence (despite growing concerns regarding high valuations and market concentration). According to the CSSF, Latin American and Asian equities were the best performers, while European equities delivered more modest gains due to the mixed economic outlook in Germany and political instability in France.

Net issuance displayed strong growth (+EUR 79 bn over the quarter), reaching its highest level since 2021 in August. This increase in capital investment, which concerns both equity and fixed-income mutual fund categories, should support real value added within the financial sector in Q3.

Labour market

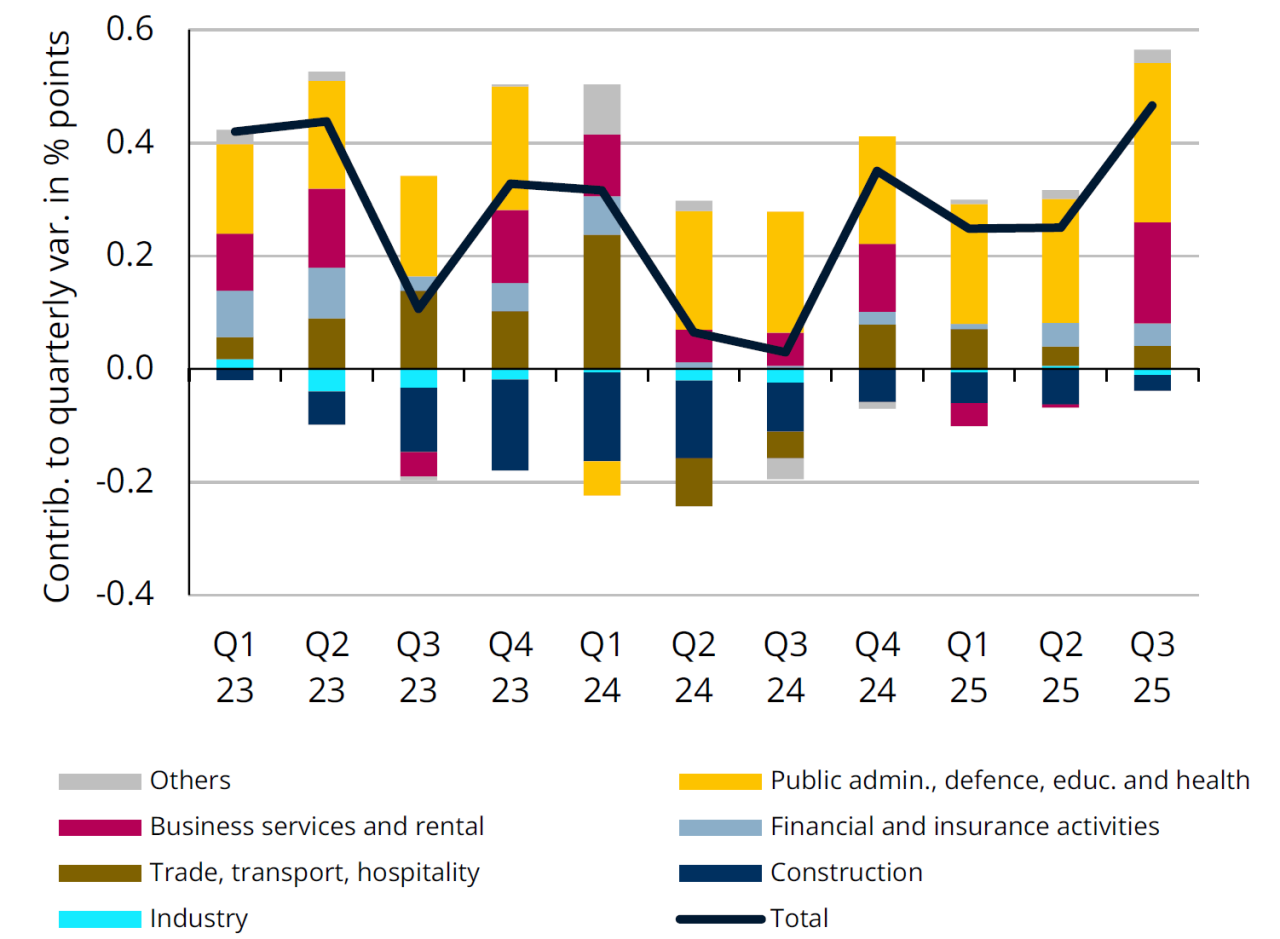

Domestic employment

Sources: IGSS, STATEC - national accounts (seasonally adjusted figures)

A good third quarter for the job market

Employment growth is gaining momentum in Luxembourg. After quarter-on-quarter growth of +0.3% in the 1st and 2nd quarters, the 3rd quarter came as a positive surprise with +0.5%. This acceleration came from both residents (+0.4% in Q3 after +0.3% in Q1 and Q2) and cross-border commuters (+0.5% in Q3 after +0.2% in Q1 and Q2).

At branch level, it is first and foremost business services that are contributing to this improvement (in particular temporary work, which had fallen sharply in Q1 and Q2, and services relating to buildings and landscaping), but also the public sector (which remains the main creator of jobs in Q3 2025). The construction sector still recorded a drop over the 3rd quarter as a whole, but this was much less pronounced than in previous quarters (the number of employees even increased slightly in the monthly figures for August, September and October).

In addition, job vacancies resumed their upward trend in September and October, particularly in business services, the financial sector and construction.

Energy

Energy prices

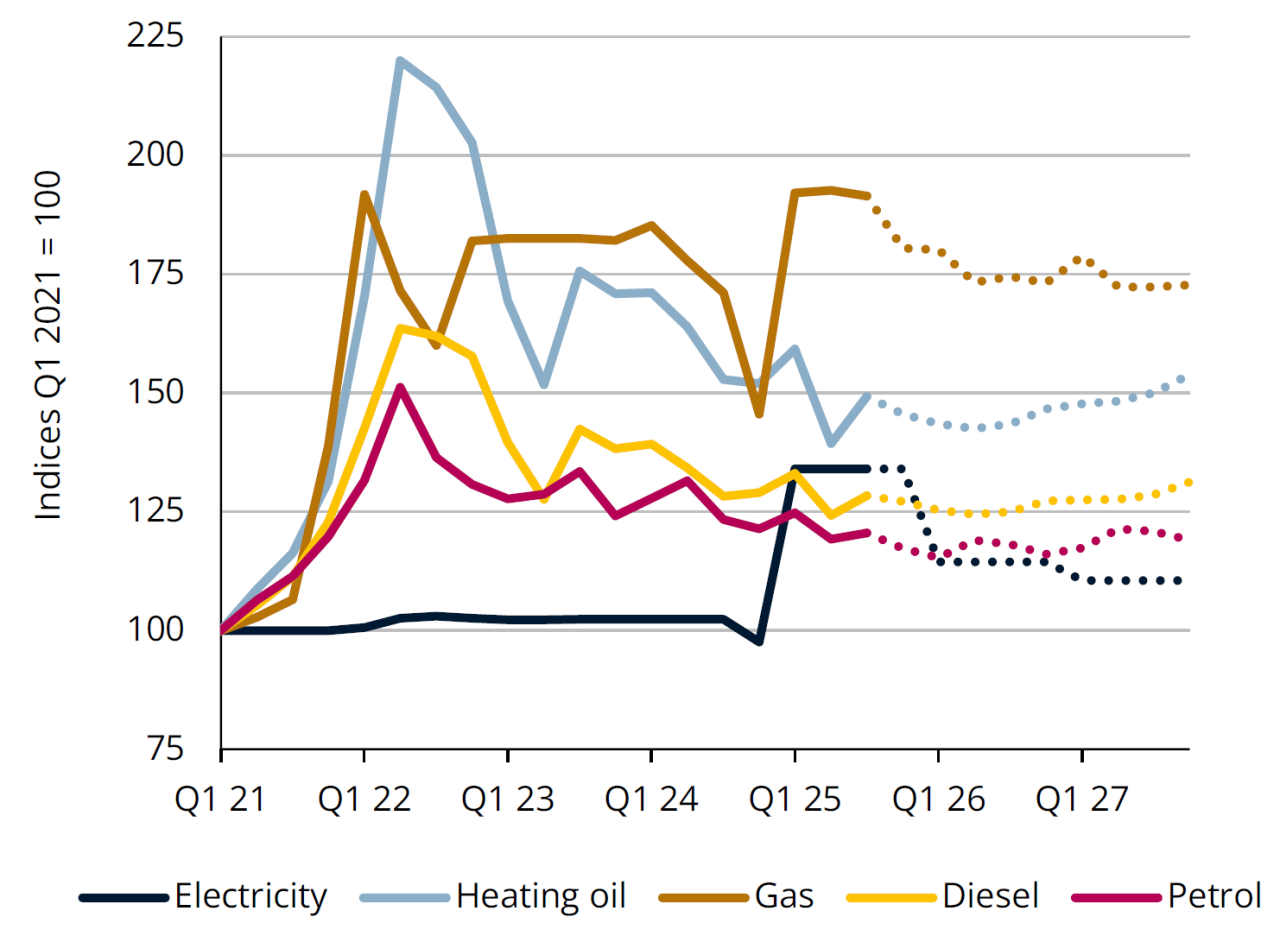

Source: STATEC (Q4 2025 - Q4 2027: forecasts)

A move towards lower energy prices in 2026

Following the partial lifting of government measures to stabilise electricity and gas prices, households saw their bills rise by around 30% for electricity and 10% for gas in 2025 compared with 2024. However, the electricity supply tariff for households is set to fall by around 15% early next year. The State will fund part of the cost of the electricity network (around a third for both households and businesses), with an overall budget of EUR 150 million. This measure, combined with lower supply costs for suppliers, will more than compensate for the removal of the subsidies introduced during the energy crisis and still in force today.

Fossil fuel prices are also expected to fall in 2026, despite a further increase in the CO₂ tax by EUR 5/t as of 1 January 2026, taking it to EUR 45/t. The forecast price drops (-7% for gas; -3% for heating oil and petrol; -2% for diesel) would be mainly due to the expected decline in gas and crude oil prices on the international markets.

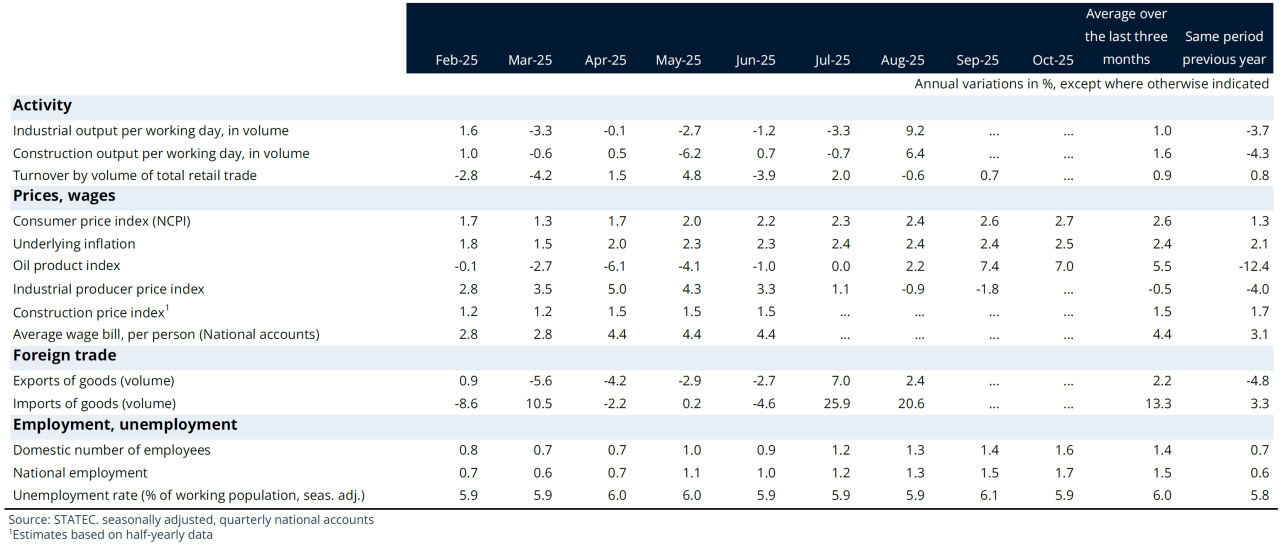

Dashboard

Indicators

Last update