Conjoncture Flash December 2024: Growth set to rise in 2025

In 2024, economic growth in Luxembourg will be moderate but should pick up in 2025 and 2026 owing to lower interest rates, which favour residential investment and the export of financial services, against a backdrop of stronger external demand[1]. Household consumption should also improve with a slight fall in savings.

The global economy is set to grow by 3% per year between 2024 and 2026, despite an expected slowdown in the United States and China. In the eurozone, the economic recovery is ongoing, but remains uneven between Member States. Moreover, it is showing signs of running out of steam as we approach 2025.

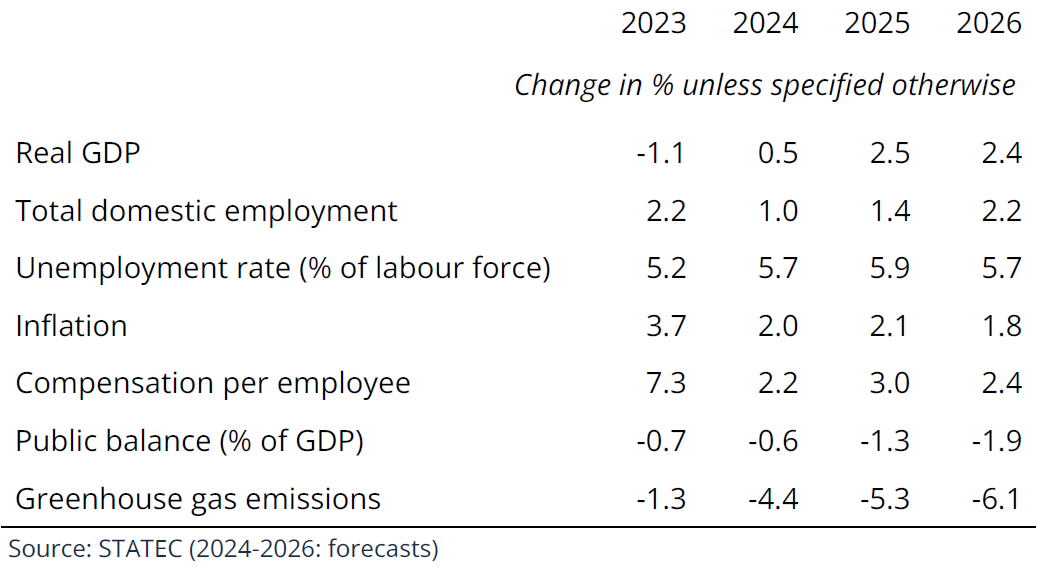

The Luxembourg economy returned to growth in 2024 after a contraction in real GDP in 2023. However, the recovery lacks vigour and remains unevenly distributed across the different sectors. For 2024, a modest expansion of +0.5% is expected, with more robust growth forecast for 2025 (+2.5%) and 2026 (+2.4%), underpinned by stronger domestic and external demand.

Eurozone inflation will hit the 2% target by the end of 2024 and it will fall below 1% in Luxembourg. However, it is expected to rise again in the Grand Duchy in 2025. Following the easing of energy price caps, inflation is likely to increase to 2.1% in 2025 and then fall back to 1.8% in 2026. The next wage indexation is scheduled for Q2 2025.

Compensation per employee has also slowed considerably since 2023, rising by just 1.2% year-on-year in Q3 2024. The reduced impact of indexation, linked to the fall in inflation and the temporary reduction in employers' contributions, had the most significant impact on this slowdown. After forecasting +2.2% for 2024, growth in compensation per employees will recover in 2025 (+3.0%) with the expiry of the contributions measure. Subsequently, it will settle at 2.4% in 2026. Inflation continues to fall and real wages continue to rise but household consumption remains held back by a high level of savings (despite a downward trend).

Employment growth in Luxembourg continues to slow in 2024, reaching its lowest level since 2009. Employment in the construction industry remains on a downward trend, but has become less pronounced in recent quarters. The anticipated recovery in economic activity should also help to boost employment. STATEC forecasts growth of +1.4% for 2025 and +2.2% for 2026, which is still well below the average for the last twenty years (close to 3%). The unemployment rate is expected to rise slightly to 5.9% in 2025 before falling back to 5.7% in 2026, reflecting stronger employment growth.

Between 2024 and 2026, public revenues are projected to slow due to the adjustment of tax scales, the fall in fuel sales and the normalisation of corporate tax balances.

MACROECONOMIC TRENDS AND FORECASTS IN LUXEMBOURG

Public spending should follow a similar trajectory with growth constrained by the end of the crisis measures. The public deficit is set to widen from -0.6% of GDP in 2024 to -1.9% in 2026.

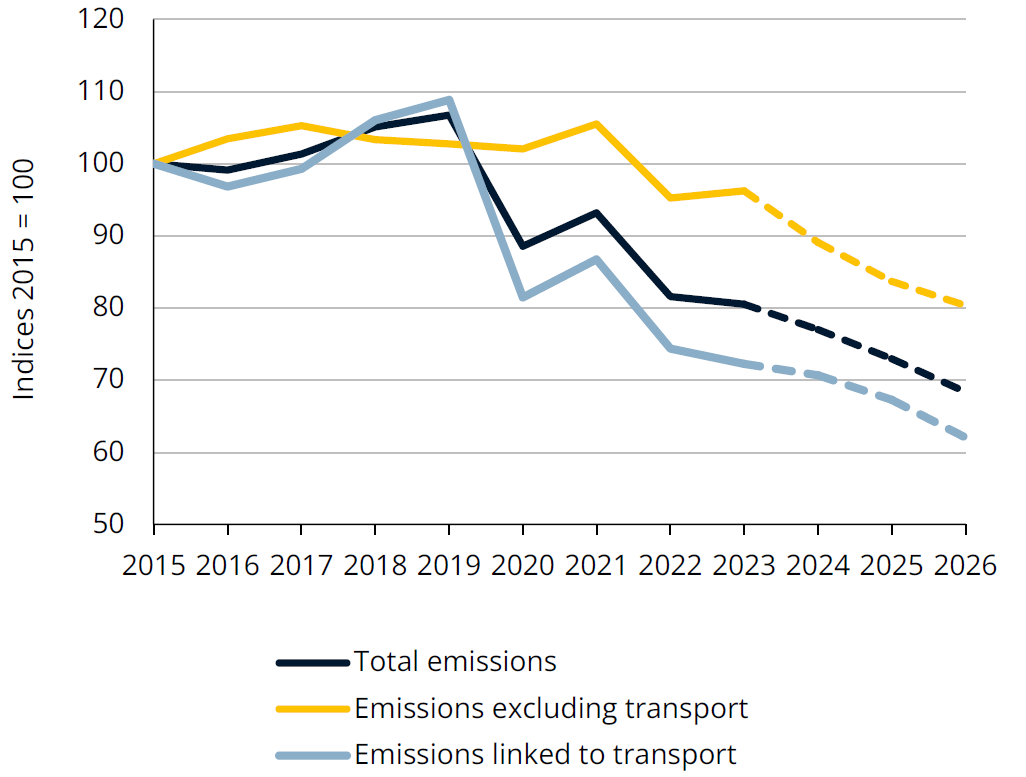

Greenhouse gas emissions in Luxembourg are expected to fall significantly, by 4.5% in 2024 and 5% in 2025 (see below). This reduction is due to lower consumption of petroleum products and increased use of electricity. Gas and electricity prices are set to rise from 2025 with the gradual phase out of tariff shields.

Projected economic upturn clouded by risks

The growth forecasts are shrouded by uncertainties, such as inflation trends and the subsequent reactions of monetary policy. These risks ultimately affect growth expectations in the eurozone and Luxembourg. On the negative side, higher-than-expected key interest rates in the eurozone could undermine the recovery which is expected to occur in 2025. On the positive side, a faster-than-expected fall in interest rates would add around 1 percentage point to the growth forecast for next year.

The expected improvement in employment is also overshadowed by ambiguity. The current slowdown in cross-border employment could well be both cyclical and structural in nature.

[1] These forecasts are taken from STATEC Note de conjoncture 2-24.

Activity

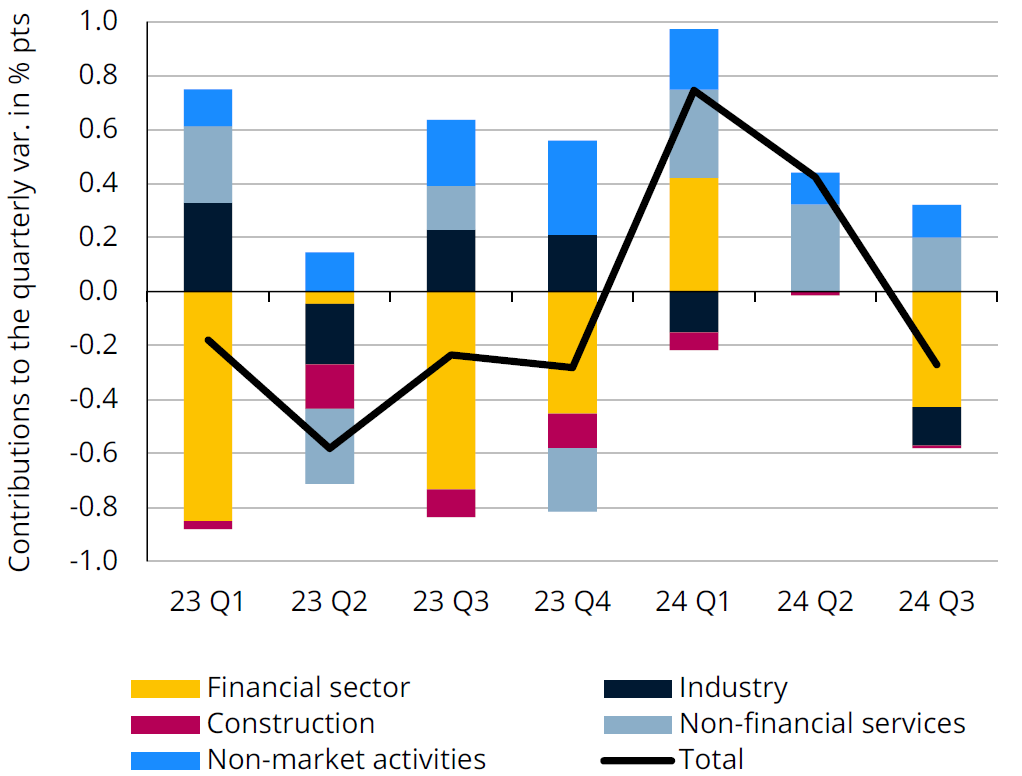

Change in real value added by sector

Source: STATEC

Recovery on thin ice

With GDP growth of 0.2% over one quarter in Q3 2024, the Luxembourg economy has recorded a fourth consecutive quarter of growth, something that has not happened since 2021 (during the post-Covid recovery). In spite of this, recent trends in activity remain marked by weak momentum. In Q3, the rise in GDP was mainly driven by taxes on production, but value added - which better reflects the underlying economic trend - fell by 0.3%. This decline was mainly due to the fall in financial activities (decline in interest margins, slowdown in investment fund issues) and - to a lesser extent - industry. Construction continues to make a negative contribution to value added, albeit to a lesser extent.

Non-financial services have performed best over recent quarters (alongside non-market activities). However, there was a downturn in Q3, reflecting the deterioration in business surveys over this period. The October and November surveys display more positive signals for non-financial services, retail trade and industry (but not for construction, where business confidence continues to fall).

Real estate

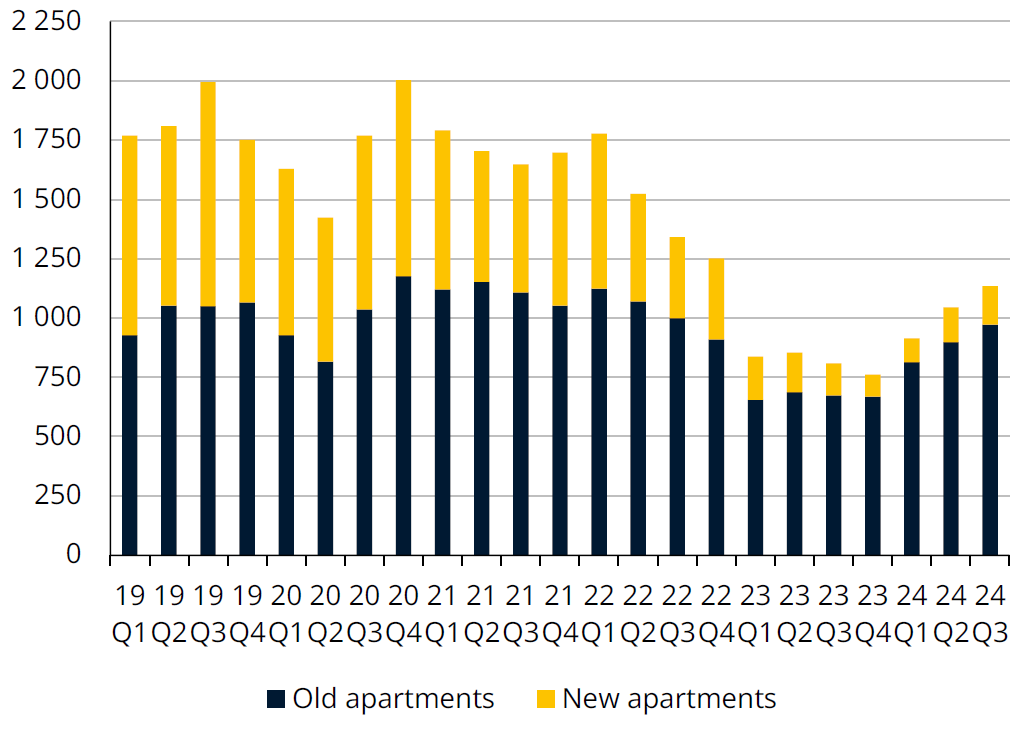

Number of transactions of apartments

Source: STATEC (seasonally adjusted data)

Real estate market is slowly getting back on track

Sales of houses and flats have been rising since the start of 2024. Sales of existing flats (seasonally adjusted data) rose by 8.3% quarter-on-quarter (+44% year-on-year) in Q3, while sales of new flats, which have been particularly weak since the start of 2023, rose by 11% quarter-on-quarter (+20% year-on-year). However, sales of new flats remain very weak (-76% in Q3 compared with the average for 2015 to 2021).

The fall in mortgage rates and property prices (-1.7% year-on-year, +0.2% quarter-on-quarter) is probably aiding the recovery. According to the bank lending survey, household demand for loans continued to pick up in Q3 in Luxembourg thanks to the improved outlook for the property market and the fall in interest rates. Demand for fixed-rate mortgages has been sustained by the decline in corresponding rates since the beginning of 2024. Variable rates started to fall later, with the key rate cuts that began in June. All in all, the average fixed and variable rates on new loans showed a similar fall of 0.5 percentage points over one year in October, with the variable rate remaining higher (at 4.3%, compared with 3.5% for the fixed rate).

Financial sector

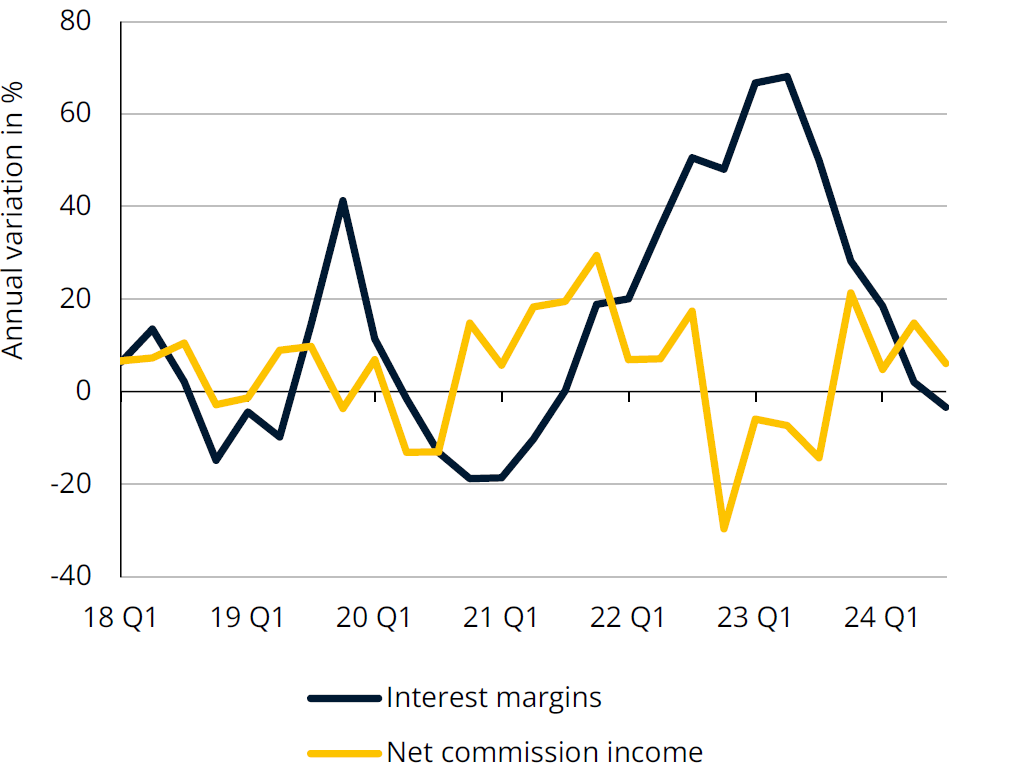

Main banking revenue items

Source: CSSF (decumulated data)

Decline in value added in the financial sector

In Q3, real value added in the financial sector fell by 1.7% over the quarter (-1.9% over the year), mainly as a result of the fall in banks' interest margins. Interest margins in Q3 fell by 0.7% quarter-on-quarter (-3.3% year-on-year) with the cuts in key rates and the fall in outstanding loans (-5% year-on-year in loans from non-financial companies, -3% in loans from households). Nevertheless, banks' earnings were buoyed by higher commissions on wealth and investment fund management, and by stagnating general expenses.

Growth in the net assets of undertakings for collective investment slowed to +1.4% quarter-on-quarter in Q3. This increase came mainly from valuations linked to the financial markets, while net asset issuance fell in September (see November's Conjoncture flash). Life insurance premiums continued their meteoric rise (up 65% year-on-year in Q3, after two years of sharp falls), mainly thanks to unit-linked products. But the value added of insurance companies contributes very little to the total of the financial sector.

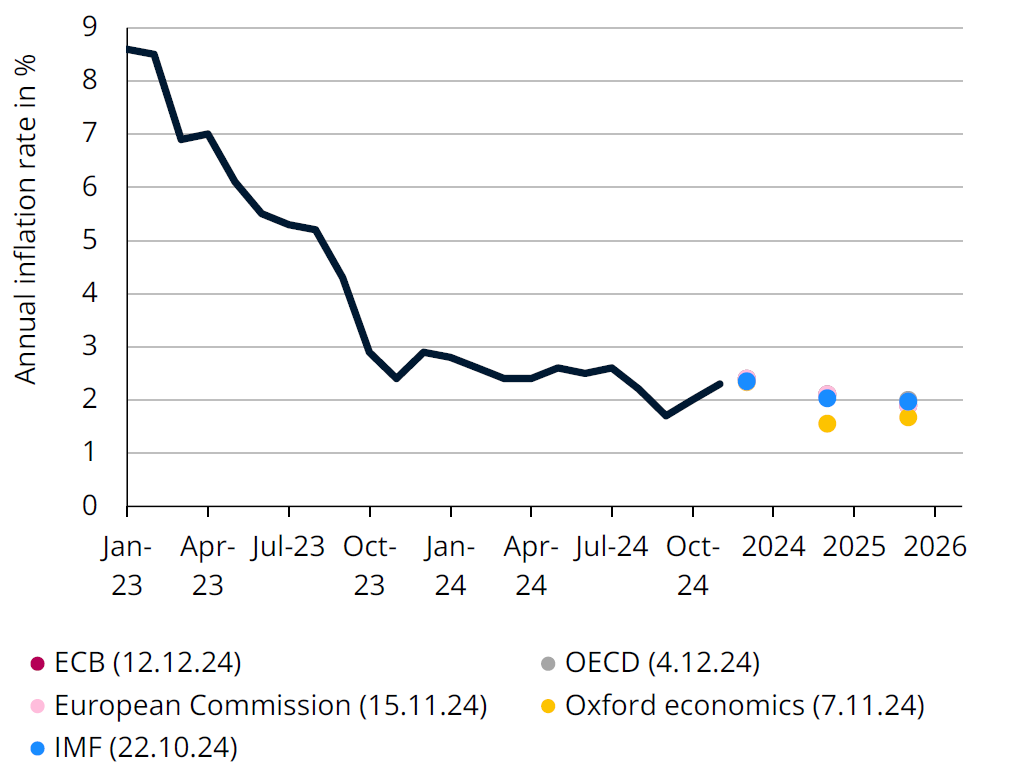

Inflation

Inflation and inflation forecasts in the eurozone

Source: Eurostat (Nov-24: flash estimate), forecasts: as indicated

Inflation fell faster than expected

In recent months, inflation has fallen faster than expected, mainly due to a sharper fall in petroleum products. The latest forecasts from the main international institutions predict that inflation in the eurozone will still average over 2% in 2024, with figures ranging from 2.3% (Oxford Economics) to 2.4% (ECB, OECD, European Commission, IMF). For 2025 and 2026, the forecasts converge around the 2% target, with a range of 1.6% to 2.1% in 2025 and 1.7% to 2.0% in 2026.

In Luxembourg, inflation currently stands at 0.8% in November, well below the eurozone rate (2.3%), under the significant effect of low inflation in services. By 2025, however, it is likely to be higher, mainly as a result of the easing of energy price caps. The latest STATEC forecasts (Note de conjoncture 2-24) predict inflation will be 2.0% in 2024, 2.1% in 2025 and 1.8% in 2026, with indexation scheduled for Q2 2025 and 2026.

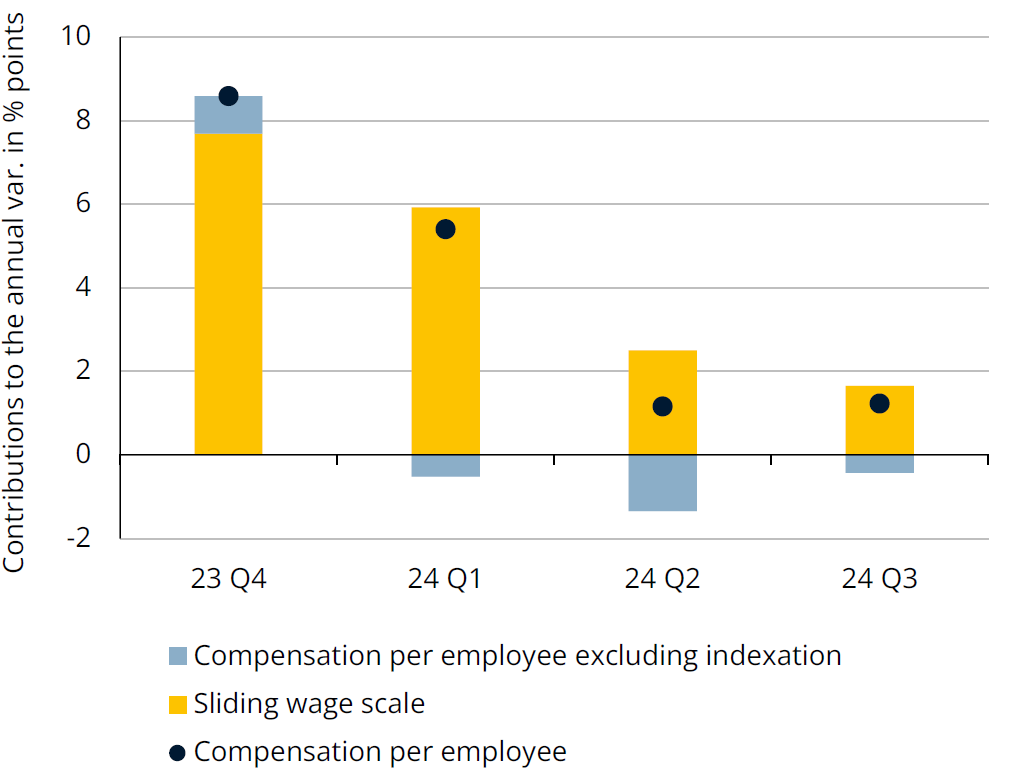

Wages

Compensation per employee

Source: STATEC

Continued slowdown in compensation per employee

Compensation per employee (CPE) rose by 1.2% over one year in Luxembourg in Q3. This represents a considerable slowdown compared to last year, mainly due to a sharp reduction in the impact of indexation (the contribution of mobile scale was 1.7 percentage points in Q3). In fact, the successive index brackets had largely contributed to the strong growth in CPE in 2023, but no longer in 2024 (unlike in the eurozone, where the increases were lower but more spread out). In Q4, the impact of indexation will fall to zero, since the last index bracket dates from September 2023 and the next one is not due until 2025, suggesting a further slowdown in CPE. The reduction in employer contributions in 2024, which is largely responsible for the negative contribution from components excluding indexation, has also restricted growth in CPE over the last three quarters. This was compounded by an exceptional base effect in Q2 (see September Flash).

In the eurozone, the trend is also leaning towards a slowdown, with CPE up by 4.3% year-on-year in Q3, compared with 4.9% in Q1. Belgium is an exception among our neighbouring countries, displaying stronger CPE growth in Q3 than at the start of the year. This is linked to an upturn in inflation in Belgium, unlike in the eurozone, where the slowdown in inflation is helping to reduce CPE growth.

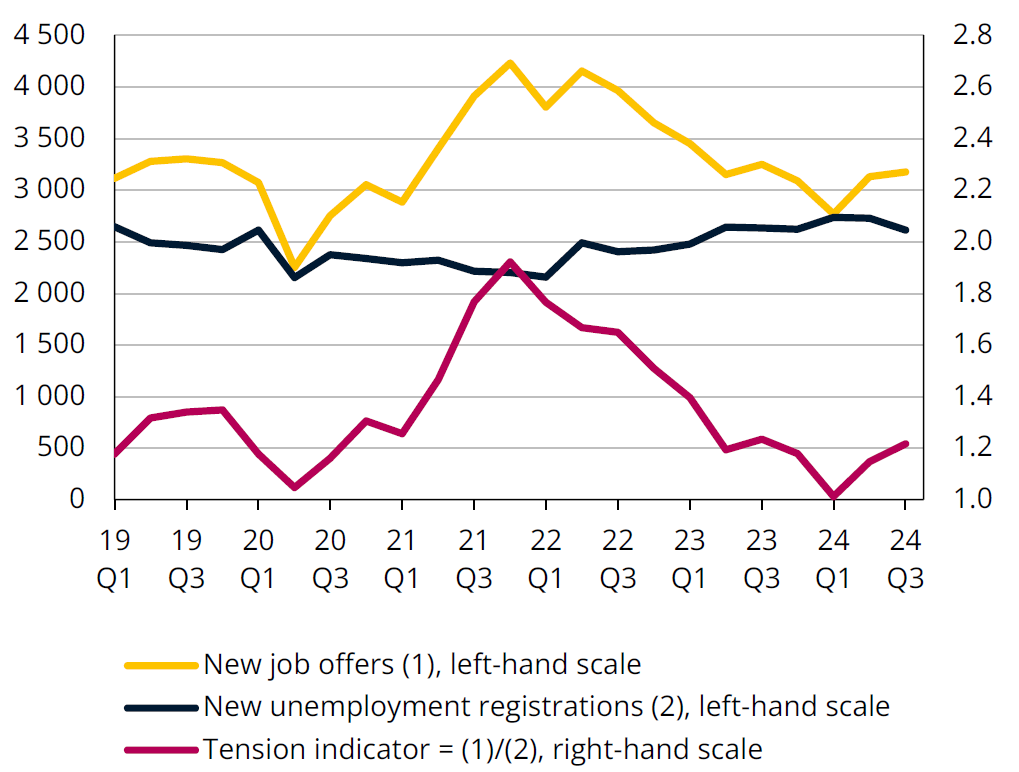

Labour market

Tension indicator on the labour market

Sources: ADEM, STATEC (seasonally adjusted data)

Slight rise in tension

The rise in the tension indicator since the start of the year raises hopes of a slight improvement in the labour market in the short term. Historically, this indicator is strongly correlated to trends in unemployment and employment, with a lead of two to three quarters. This rise in tension stems from both components of the indicator: a slight fall in new jobless registrations (-4% between Q1 and Q3) and a recovery in the flow of job offers (+15%). This contrasts with the continuing fall in the number of vacancies (-10% between Q1 and Q3). According to the ADEM (Press release of November 2024), this disconnection can be explained by a "reduction in the average length of time job offers have been open since September 2023", the month in which the law facilitating access to the labour market for third-country nationals came into force.

In autumn 2024, the unemployment rate remained on an upward trend (albeit more moderate than in 2023), reaching 5.9% in November. Employment accelerated slightly compared with the start of the year, rising from +0.16% over one quarter in Q1 to +0.21% in Q2 and then +0.24% in Q3, but this increase remains extremely weak (+0.7% on average over the last decade).

Energy

Greenhouse gas emissions in Luxembourg

Sources: Inventory of GHG emissions, STATEC (2023-2026: forecasts)

Greenhouse gas emissions set to fall further by 2026

STATEC expects fossil fuel prices to rise in 2025, mainly as a result of the expiry of State subsidies for gas and heating oil, as well as the increase in the carbon tax from EUR 35 to EUR 40 per tonne of CO2. This rise in fossil fuel prices, combined with the continued electrification of heating and transport, has led STATEC to forecast a fall in greenhouse gas emissions of 5% in 2025 and 6% in 2026.

On the one hand, this reduction is due to the transport sector, where STATEC forecasts a further fall in fuel sales, estimated at -4.5% in 2025 and -7% in 2026. This trend is the result of more attractive prices for professionals in Belgium and France than those currently available in Luxembourg, but also due to the expected expansion in the electrification of vehicles, which should accelerate in the near future. In terms of non-transport emissions, the fall would be driven essentially by a reduction in the consumption of gas and heating oil.

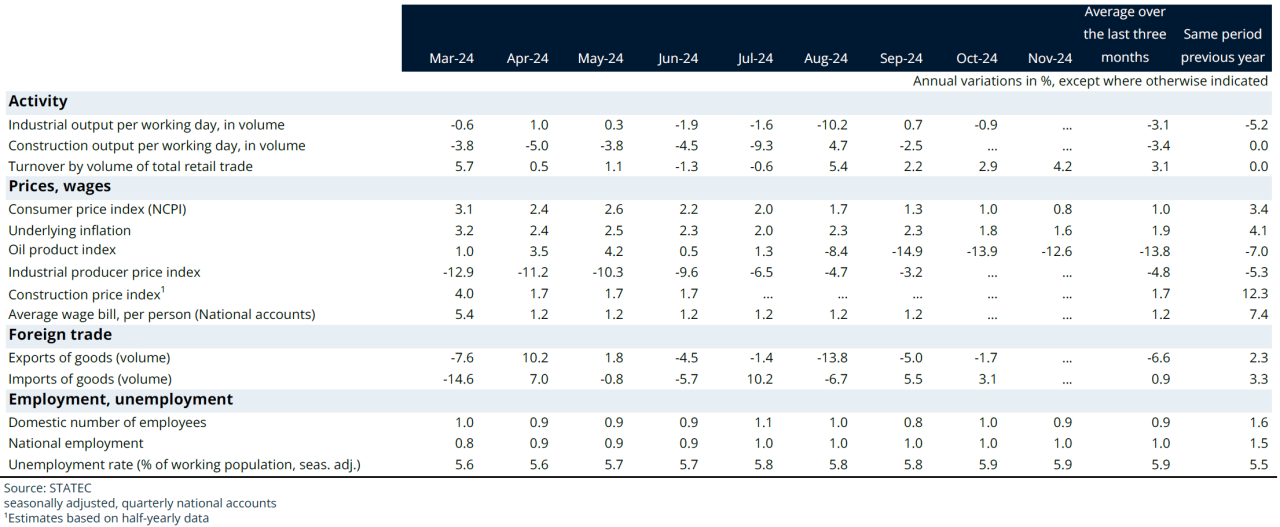

Dashboard

Indicators

Last update