Note de conjoncture 2-25

Recovery under pressureAlthough global activity has shown some resilience this year, it remains under threat from the negative effects of rising trade tensions. A moderate recovery is taking hold in Luxembourg, which should strengthen in 2026 and 2027.

International environment still marked by uncertainties linked to US policy

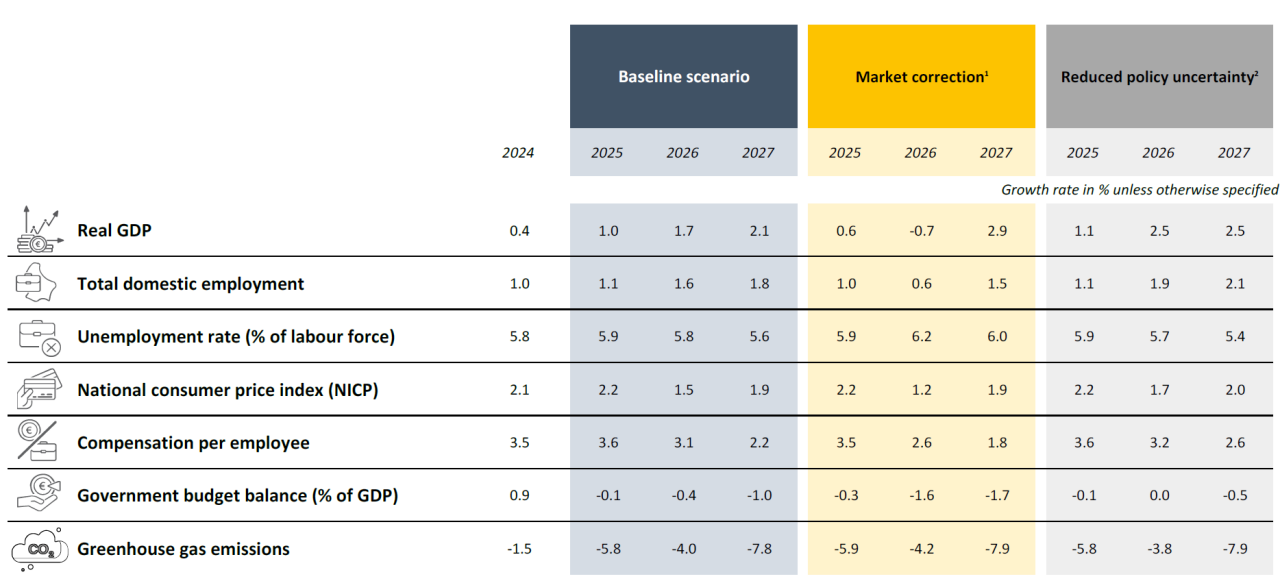

Despite rising trade tensions, the economy and international trade in goods showed notable resilience in 2025. A slowdown in global activity is expected next year, but it will be less pronounced than expected. Investment in artificial intelligence has been a factor supporting the economy and stock markets. Some of the uncertainty surrounding trade policy has been removed in recent months, but uncertainty remains high regarding the impact of US tariff hikes. Activity in the eurozone also held up well over the first three quarters of the year, despite contrasting performances from one Member State to another. Growth is expected to be around 1.3% in 2025 and to fall back below 1% in 2026.

More positive signs for recent activity pointing to a moderate acceleration in growth up to 2027

In Luxembourg, activity picked up again in the first half of 2025, after three years of near stagnation. Growth in the second quarter was driven by information and communication services, non-market activities, industry and real estate. More positive signs were seen in the third quarter for financial and non-financial services, as well as for construction, although the latter is still experiencing a number of difficulties. Lower interest rates should stimulate investment and activity in the property and construction sectors over the coming quarters. The financial sector, meanwhile, should benefit from buoyant stock markets. Under these assumptions, GDP growth would be modest in 2025 (1.0%), rising to 1.7% in 2026 and 2.1% in 2027.

Inflation below 2% in 2026 and 2027

Inflation was close to 2% in the eurozone in Q3 2025, but higher in Luxembourg (2.5%). Pressure on commodity prices is increasing with a surge in precious metals, while the easing off in fruit and vegetable prices contrasts with an ongoing sharp rise in meat prices. STATEC is forecasting inflation of 2.2% in 2025, slowing to 1.5% in 2026, with energy prices expected to fall, particularly for electricity. A gradual return to an inflation rate close to the ECB target is expected in 2027, with inflation estimated at 1.9%. The next wage indexation is foreseen for the third quarter of 2026, followed by another one a year later.

After slowing sharply in 2024, compensation per employee accelerated in the first half of this year, as a result of the rebound in employer contributions and, above all, the index bracket in May. Over the year as a whole, compensation per employee should rise by 3.6%, before slowing to 3.1% in 2026 and 2.2% in 2027. Next year, the increase in contributions resulting from the pension reform will have an upward impact, but it is above all the pace of indexations that will continue to be the major determinant of compensation per employee growth over the next few years.

Job creation strengthens – a trend set to continue

The labour market, which has deteriorated significantly since 2023, has recently been showing more positive signs. Job creation strengthened in the third quarter, particularly in market services, and unemployment no longer appears to be rising. Evolutions have been favourable (or less unfavourable) in construction, where employment has stopped falling, but also in the public sector. After an increase in total employment limited to around 1% in 2025, economic momentum is set to strengthen in 2026 and net job creation should accelerate accordingly, rising up to 1.6%. The labour force is expected to increase by 1.2% per year over the period, while the total population is expected to grow by 1.3% in 2025, 1.4% in 2026 and 1.5% in 2027. Unemployment is expected to fall slightly, from 5.9% of the labour force in 2025 to 5.8% in 2026 and 5.6% in 2027.

Public finances: spending growth outstrips revenue growth up to 2027

After four years of strong growth, public revenues will slow down in 2025 and should continue to show moderate growth over the next two years. The "Entlaaschtungs-Pak" measures in favour of households and businesses and the package of housing measures, combined with base effects on corporation tax and VAT, are contributing to the fall in taxes collected by the State. The pension reforms will boost revenues by directly increasing social security contributions. Growth in public spending is set to remain strong, with employment and wages in the civil service showing little sign of slowing. Social benefits linked to pensions and investments (including the launch of a military satellite and CFL projects) are other areas of expenditure that are rising sharply. STATEC expects public spending to rise by around 6% per year between 2025 and 2027. The public balance would fall to -0.1% of GDP in 2025, -0.4% in 2026 and -1.0% in 2027.

Emissions fall mainly due to lower fuel sales

Global oil output reached new heights in 2025, contributing to a gradual easing in oil prices. In Europe, gas storage levels remain lower than in previous years, but a 20% decline in consumption since 2021 and growing use of liquefied natural gas are limiting the risks weighing on supply. In Luxembourg, the boom in renewable electricity production continues, driven mainly by photovoltaics, where over 70% of new capacity now concerns self-consumption. Following the increases in gas and electricity prices in 2025, STATEC expects price cuts of 7% and 15% respectively in 2026. STATEC forecasts a further contraction in the volumes of oil products sold in Luxembourg in 2025 and 2026 (-3% and then -7% for heating oil and -7% and then -4% for fuel sales). Falling fuel sales should also account for most of the reduction in greenhouse gas emissions expected in Luxembourg, estimated by STATEC at -6% in 2025, -4% in 2026 and -8% in 2027.

Thematic studies in this Note

Macroeconomic forecasts

- Source: STATEC (2025-2027: forecasts)

- In this adverse scenario, increased uncertainty about inflation prospects and US debt weakens financial markets, raises borrowing rates, and slows global growth.

- In this favorable scenario, reduced uncertainty about US trade policy encourages businesses to invest and hire, which supports stock markets and stimulates global demand..

Press Office | Tél 247-84219 | Fax +352 26 20 19 0 | info@statec.etat.lu

La reproduction totale ou partielle du présent bulletin d’information est autorisée à condition d’en citer la source.

Last update